Welcome to the Real China Bond Market

China's onshore bond market liberalizes further, offering more exposure to China's economic transition.

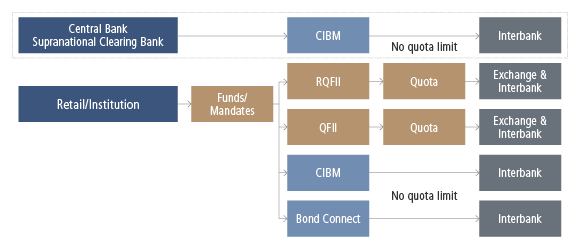

China's bond market can be split into three categories: the offshore USD and CNH (“Dim Sum”) markets; and the onshore CNY market. In 2011, China kicked off liberalization of the onshore market by including them in the Renminbi Qualified Foreign Institutional Investor program (RQFII).

Despite steadily increasing the RQFII quotas, by 2015 non-Chinese investors still owned less than 2% of this massive onshore bond market. This could be set to change after the launch of “Bond Connect” in 2017, a channel enabling international investors to trade, without quotas, on global trading platforms, with their assets held at global custodians, and with offshore cash accounts. We expect derivatives and two-way trading to follow in time.

The People's Bank of China (PBoC) estimates that 15% of the onshore bond markets could become foreign-owned: the average for major developed and emerging bond markets sits at 39%; even Japan's bond market, which is domestically-oriented and offers very low yields, is 8% foreign-owned.

The investment case is well rehearsed. China is now the second-largest economy in the world and sovereign fundamentals are strong: it has a high savings rate and sovereign debt at less than 60% of GDP, it remains a net external creditor to the world, runs a persistent current account surplus, and is increasingly powered by domestic consumption rather than investments and exports.

We argue that the onshore, CNY bond market is the better way to take exposure to this long-term China opportunity in fixed income. As well as simply being 10-times larger than the offshore markets, it includes more corporate issuers from a wider diversity of sectors, and therefore offers more exposure to the dynamics of domestic China with much lower correlations to international markets. Moreover, adjusted for credit quality, yields are somewhat higher onshore than offshore.

Private sector leverage has been rising steeply in China, but is now levelling-off. The banking and shadow-banking sectors are being de-risked and corporate sector debt-servicing capacity has been improving as productivity and profitability improves. While we expect a more laissez-faire attitude from regulators to defaults among non-systemic onshore borrowers, over the long-term this should improve the overall quality of the market and instill greater discipline.

There are now four ways into the China onshore bond market

Source: Neuberger Berman. For illustrative purposes only.

YOU MAY ALSO LIKE

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment.Past performance is no guarantee of future results.

Firm data, including employee and assets under management figures, reflect collective data for the various affiliated investment advisers that are subsidiaries of Neuberger Berman Group LLC (the “firm”). Firm history and timelines include the history and business expansions of all firm subsidiaries, including predecessor entities and acquisition entities. Investment professionals referenced include portfolio managers, research analysts/associates, traders, and product specialists and team dedicated economists/strategists.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 11/04/2019.