Wrap up of Q1 Market Outlook 2019

The S&P 500 Index has staged a steady rally of close to 20% from its Christmas Eve low of 2351.10 to 2792 (as of 22/02/2019) while the Shanghai Composite Index also gained close to 16% for the first two months of 2019. This is in stark contrast to the sentiments in Q4 last year where investors are taking risks off the table in droves.

Is the positivity we had so far in the Year of the Pig sustainable? Or is this merely a Dead Cat Bounce?

We recently concluded our Q1 Market Outlook Seminar where we had Allianz Global Investors, BlackRock, JPMorgan Asset Management, LionGlobal Investors, and NikkoAM share their views on the key issues at the top of investors’ minds as well as how investors should position their portfolio for the rest of the year.

Here are the highlights:

-

1. US-China Trade War

Probably one of the biggest contributor to the slump last year, markets cheered after Trump extends China tariff deadline scheduled initially on 1st March, citing substantial progress in trade talks with China on important structural issues including intellectual property protection, technology transfer, agriculture, services, currency amongst many other issues.1

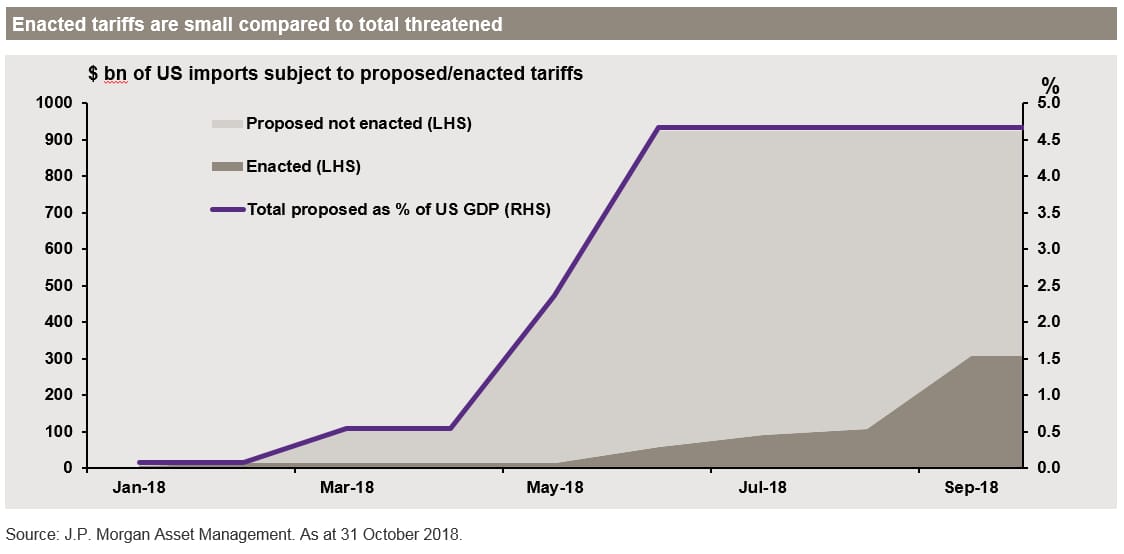

Although we are not out of the woods yet, it seems that both Chinese President Xi and US President Trump are motivated to work out their differences to ensure stability in their respective home markets. Also, while the headline news of tariffs proposed and enacted seems alarming, in reality, the total tariffs enacted compared to those proposed painted a different picture. See Fig. 1 below.

Fig. 1 (from JPMorgan Asset Management)

-

2. Central Bank Policy

With a total of four rate hikes by the US Federal Reserve in 2018 and the expectation of two to three more this year, it is no surprise that the hawkish Central Bank Policy got investors spooked last year. However, since the start of 2019, Fed Chairman Jerome Powell has adopted a more dovish stance by not raising interest rates during its last policy meeting held on Jan 29th and pledged that future moves will be done patiently. The central bank also voted unanimously to hold its policy rate in a range between 2.25-2.5% providing much needed relief for investors.2

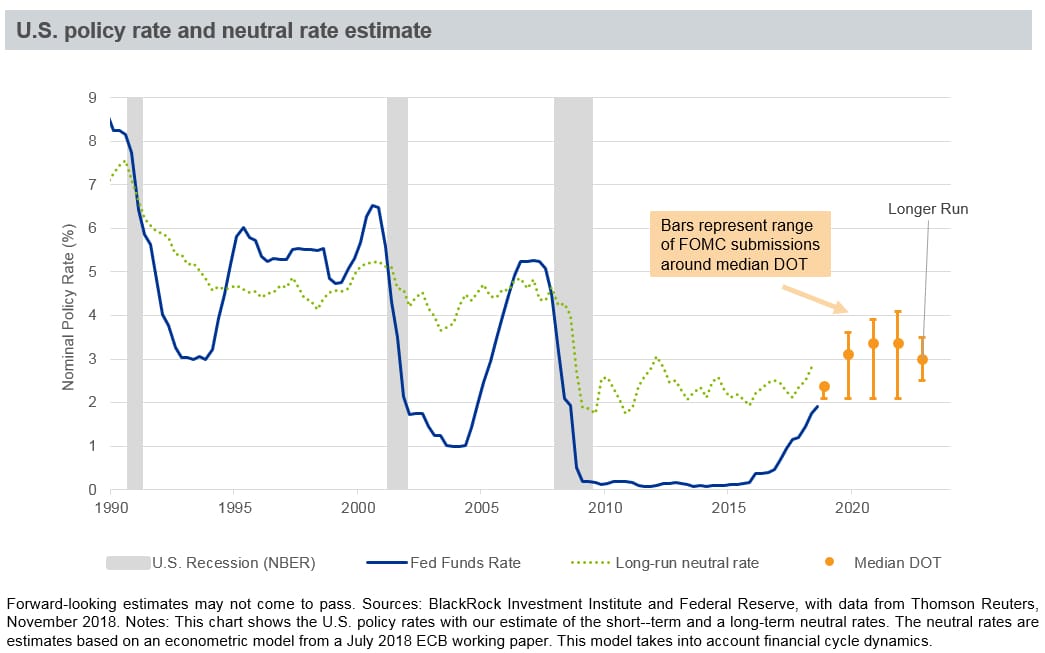

Elsewhere in Europe, the European Central Bank (ECB) continues to be more accommodative than the Fed, holding its benchmark refinancing rate at 0% on Jan 24th and reiterated that it is expecting key interest rates to remain at record low levels at least through the summer of 2019.3 See Fig. 2 below.

Fig. 2 (from BlackRock)

-

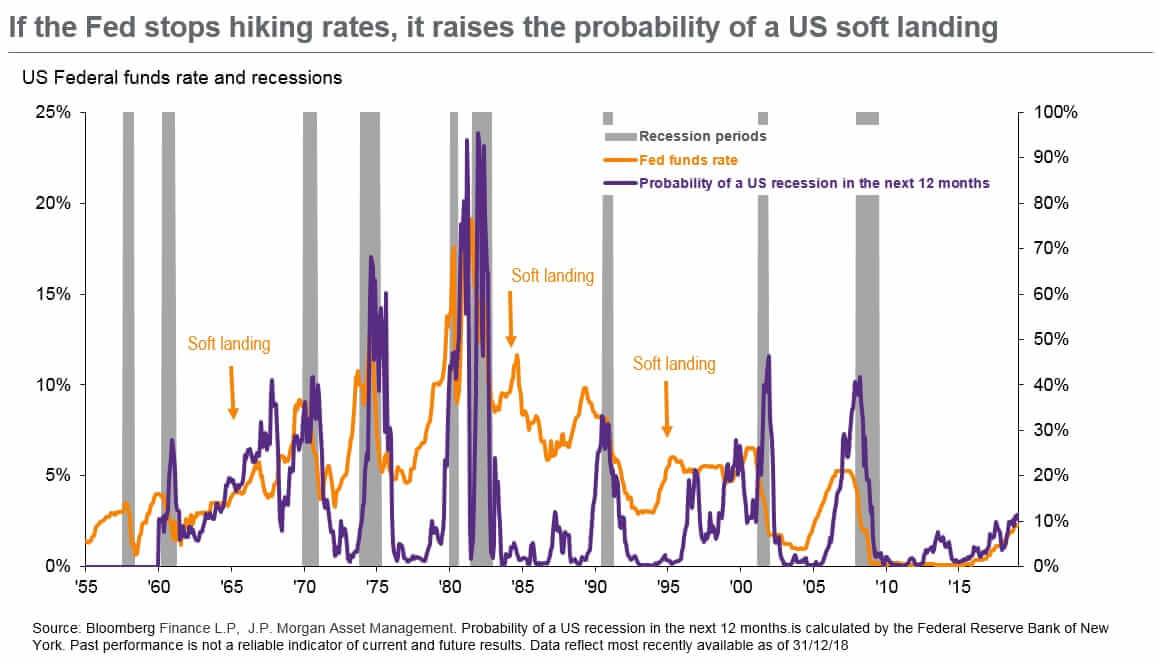

3. Late cycle in US economy but risk of recession in 2019 is low

The million-dollar question on everyone’s minds - When is the next recession?

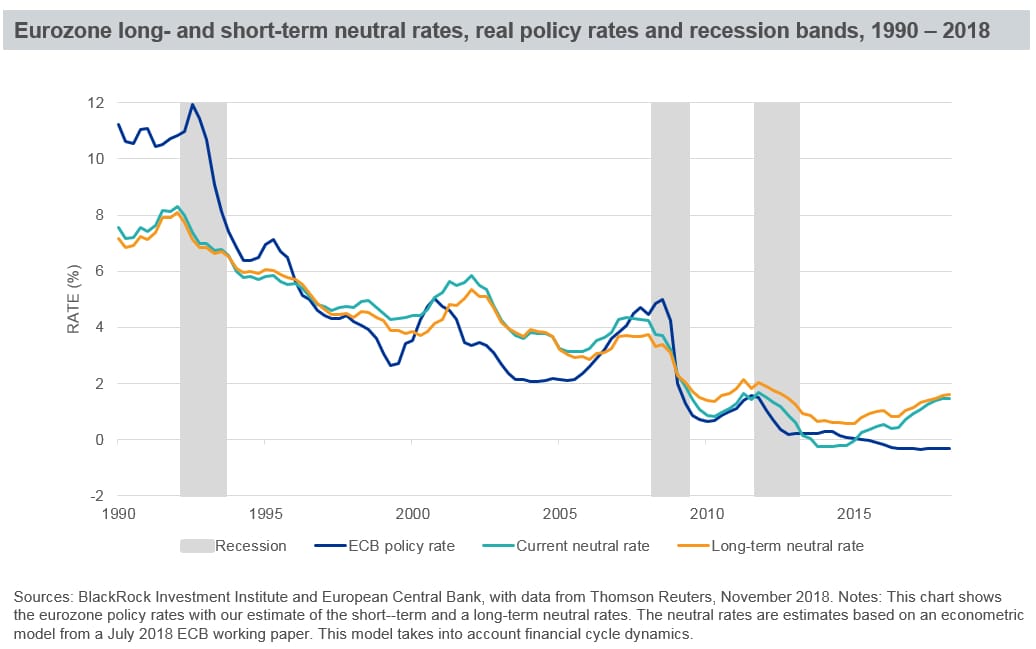

Both BlackRock and JPMorgan Asset Management estimates that the risk of a US recession in 2019 is relatively low with JPMorgan Asset Management going further to indicate that if the Fed stops hiking rates, it raises the probability of a US soft landing. See Fig. 3 and 4 below.

Fig. 3 (from BlackRock)

Fig. 4 (from JPMorgan Asset Management)

-

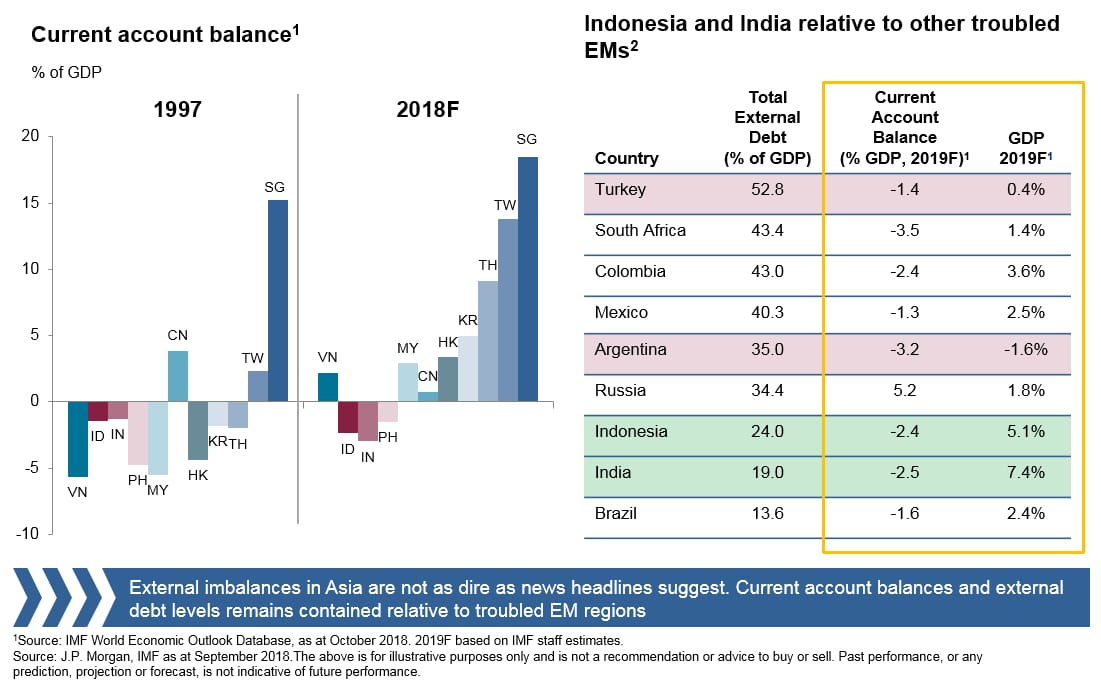

4. 2018 Emerging Market Rout

Concerns about the contagion risks of Emerging Markets after the collapse of the Turkish lira, Argentinian peso, South African rand and Brazilian real caused widespread panic for Emerging Market investors in 2018.4

However, this widespread panic may be unfounded, at least in Asia. Research by Allianz Global Investors found that Asia is in a better shape than it was during the 1997 Asian Financial Crisis. Current account balances and external debt levels remains contained relative to the troubled Emerging Market regions. See Fig. 5 below.

Fig. 5 (from Allianz Global Investors)

Now, with a clearer picture of the major concerns and improving sentiments, how should investors position their investment portfolios? Here are some quick recaps on what our fund partners shared at our Q1 Market Outlook seminar in January and February 2019.

For Allianz GIobal Investors, their high conviction themes for 2019-2021 are the “Hunt for Income” and “Rise of Asia”. To capitalize on these two themes, investors could look into Asian Bonds as they are currently offering attractive yield enhancements, especially within the Asian Hard Currency High Yields space where defaults are likely to be contained and widespread systemic risks are not expected. It also offers good long-term risk-adjusted returns for investors. US High Yields, one of the highest yielding fixed income instruments in the world, also look attractive with fundamentals supportive and defaults below their long-term historical average in addition to continued deleveraging and improving earnings and revenue. For those keen to find out more about Asian Bonds, click here to see our full suite of Asian Bonds on dollarDEX by using our Fund Finder to filter according to Asset Class and Geographical Region.

For BlackRock, rising risk calls for careful balancing of risk and reward using an active and dynamic approach to quality assets twinned with high-conviction allocations. Diversifying income sources across traditional and complementary asset classes are also key to navigate this late-cycle phase. BlackRock currently is overweight US and EM equities and underweight European sovereigns and equities. Click here to check out the US and EM equities funds by using our fund finder to filter according to Asset Class and Geographical Region.

Moving into 2019, JPMorgan Asset Management expects to see a return to more trend-like growth from 2018’s above-trend growth, portfolios should be dynamically positioned with a focus on diversification across geographies, asset classes and risks. In the late cycle, Income will also play a larger role in investor’s total return and Asia presents good opportunities for yield. In Asian equities, JPMorgan Asset Management sees value relative to developed market equities, coupled with attractive yields, supportive fundamentals and possible upside capture with a focus on value. The strategy for Asian income should be through a diversified approach of both Asian equities and fixed income, to achieve a stronger risk-reward profile. To view our extensive list of Asia funds, click here to compare them.

LionGlobal Investors (LGI) expects slower growth and higher likelihood of growth risks during this period and shared about how to navigate retirement risk in a volatile world through an Active, High-quality, Short-Duration Bond fund that combines liquidity features of Money Market Funds. If you are into the game of stability in 2019, check out LGI’s Enhanced Liquidity Fund and compare it with our Money Market Funds here.

Finally, NikkoAM sees potential in Asia, and urges investors to look beyond the market storm by focusing on economic resilience and sustainable growth sectors such as Asian Healthcare, Asian Tourism and Asian Insurance. Use our comprehensive fund finder to search for Asian funds that suits your investment appetite.

With these expert insights in mind, consider how it can fit into your overall investment strategy and always remember to do your homework before making any investment decisions. Start your no-fees investing journey with us on dollarDEX and explore close to 1,000 funds using our intuitive fund finder.

If you need any help, feel free to reach out to our customer service team by calling 6220 7890 from Mondays to Fridays, 9:00 am to 5:30 pm, or email us at cs@dollardex.com for a chat!

Sources:

1. https://www.businesstimes.com.sg/government-economy/asia-cheered-as-trump-delays-tariff-deadline

2. https://www.cnbc.com/2019/01/30/fed-leaves-rates-unchanged.html

3. https://www.cnbc.com/2019/01/24/ecb-interest-rate-decision-january-2019.html

4. https://www.reuters.com/article/us-emerging-markets-economy-analysis/analysis-emerging-market-currency-crisis-could-lead-to-broader-economic-trouble-idUSKCN1LU1V7

YOU MAY ALSO LIKE

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 14/03/2019.