Singapore bonds offer steady returns

12 May 2020

Although the COVID–19 induced market volatility has impacted almost every asset class, there are some that have held up better. Singapore dollar (SGD) bonds have managed to offer relatively stable returns in the current environment due to its defensive characteristics.

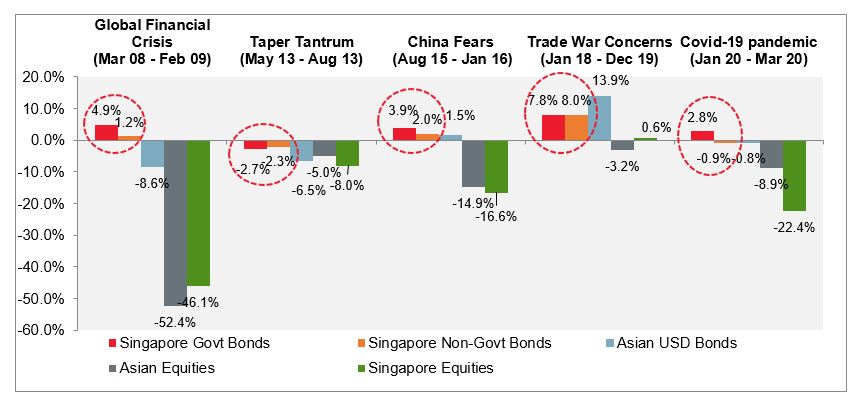

Historically Singapore bonds have delivered relatively stable returns even during periods of market volatility. This is evident again in the current global health crisis; Singapore's local currency government and non–government bonds generated resilient returns while most other asset classes in Fig 1 struggled. This resilience can be attributed to a number of factors.

First, Singapore is among a handful of countries in the world to boast the best (AAA) ranking from all three major ratings agencies. Even as some of these countries have recently come under rating pressure given the increased fiscal burden arising from COVID–19, Singapore's rating remains steady thus far underpinned by robust governance, strong economic fundamentals and a stable political environment.

Second, Singapore government bonds deliver attractive yields. Typically, in a risk averse environment, investors seek safety in US Treasuries. At the time of writing, 10–year US Treasuries offer 0.6% yield versus 0.9% from a 10–year Singapore government bond.2 Given that the US has a lower sovereign rating of AA+ by Standards & Poor, the yield offered by Singapore government bonds stand out as good value. This value is further enhanced when compared against the negative yields of some government bonds in the Eurozone and Japan.

The onset of COVID–19 has also seen central banks globally slashing rates to support their economies. As it is still too early to see how effective this will be in supporting growth, it is likely that interest rates will remain lower for longer. With the savings rate and 1–year fixed deposit rates in Singapore below 1%, the yields offered by Singapore government bonds look attractive.

Third, the SGD bond market is one of the most developed markets in Asia and is becoming a natural choice for international issuers looking to raise funding outside of their home countries. The Monetary Authority of Singapore launched the Asian Bond Grant Scheme in January 2017, which aims to broaden the issuer base in the Singapore debt market by co–funding expenses related to bond issuance for first–time issuers. The local bond market has grown significantly in size and corporate bonds issued by companies in various sectors provide diversification opportunities (see Fig 2).

By diversifying across government, quasi government and corporate bonds, investors can benefit from higher yields. The yield pickup can amount to over 2% and this is particularly pertinent in the current low interest rate environment. All these make the SGD bond market not only a reliable fundraising platform for issuers, but also a viable asset class for income–seeking investors.

An effective portfolio diversifier

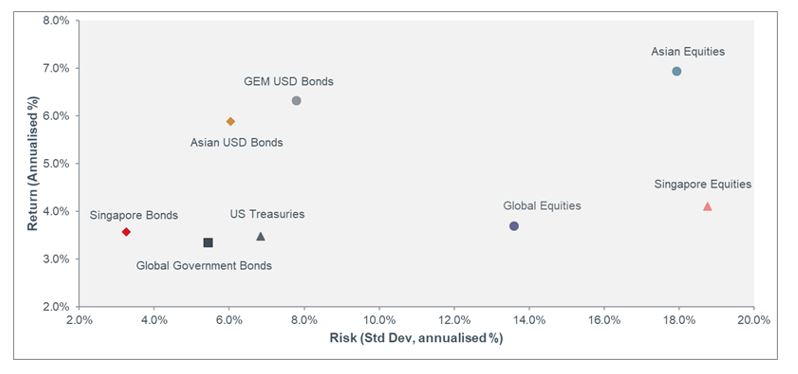

The Singapore dollar bond market, as measured by the Markit iBoxx ALBI Singapore index, has delivered a cumulative return of 19.7% in the last five years4. The index has returned 3.7% on an annualised basis over five years and has one of the lowest risk profiles as seen in Fig 3. Due to the favourable risk/return profile, Singapore bonds play a significant role in protecting the downside risk of a portfolio.

Furthermore, the negative correlation between the Singapore dollar bond and the Singapore equity markets implies that Singapore dollar bonds can play an important role in stabilising investors' portfolios over the medium to long–term.

Accessing SGD bonds

The increasing maturity of the SGD bond market has also sparked interest from individual investors to hold bonds directly. While direct investment in bonds, and holding them to maturity, appears to be a straightforward and easy–to–understand way of obtaining regular income, this may not necessarily be the best way to optimise returns over time.

Direct investments in SGD corporate bonds typically require large capital outlays as the minimum investment requirement is high, at SGD 200,000 or SGD 250,000 for each bond. To be sure, retail investors can invest directly too at a lower minimum investment amount (SGD1,000 and above) in retail corporate bonds, but there are limited investment choices. Diversification across more bond issues helps to lower an investment portfolio's concentration/issuer risks and mitigate any adverse portfolio impact arising from price fluctuation of a single corporate bond or the occurrence of a credit event/default.

Investing in a bond fund can therefore offer benefits from diversification across a wider investment universe not to mention the professional investment expertise of an experienced fixed income team that can select credits and provide investors with enhanced returns while keeping default risks low. Institutional investors enjoy better pricing power and have an allocation advantage as they typically have larger order books which allow them to participate and potentially obtain a larger allocation in a new bond issue.

The uncertainties surrounding the extent of the impact of COVID–19 on economies are likely to weigh on financial markets and keep volatility elevated for some time. For income–seekers, SGD bonds can play a key role in stabilising portfolios while providing an attractive level of income. Given the size and technical characteristics of the SGD bond market, professional knowledge and access via a bond fund is often key to maximising returns in this market.

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 12/05/2020.

-

1 Bloomberg, Eastspring Investments, 31 March 2020, based on monthly data. Singapore Govt Bonds represented by Markit iBoxx ALBI Singapore Government Index (SGD), Singapore Non-Govt Bonds represented by Markit iBoxx ALBI Singapore Non-Govt Index (SGD), {Prior to 1 May 2016, HSBC Singapore Local Currency Bond index (SGD)}, Asian USD Bonds represented by the JP Morgan Asia Credit Index (USD), Singapore Equities represented by MSCI Singapore index (SGD), Asian Equities represented by MSCI AC Asia ex Japan (USD)

-

2 30 April 2020

-

3 Asian Development Bank, Eastspring Investments, as at 31 December 2019

-

4 Bloomberg as at 23 April 2020. Total return for 5-year period (31/3/2015 – 31/3/2020)

-

5 Bloomberg, Eastspring Investments, from 31 December 2000 to 31 March 2020 based on monthly returns, in Singapore dollars, using Bloomberg conversion rates