Selling in May and going away? Think again

Following one of the swiftest and sharpest selloff in history between February and March this year, where major indices were capitulated and found an “intermediate” bottom on 23rd March, the bulls have since fought back hard and fast against the bears – causing financial markets to stage one of the fiercest rallies after a crash, eclipsing even the 1929 plunge which precedes the Great Depression, the 1987 crash and even the 2008 global financial crisis. 1

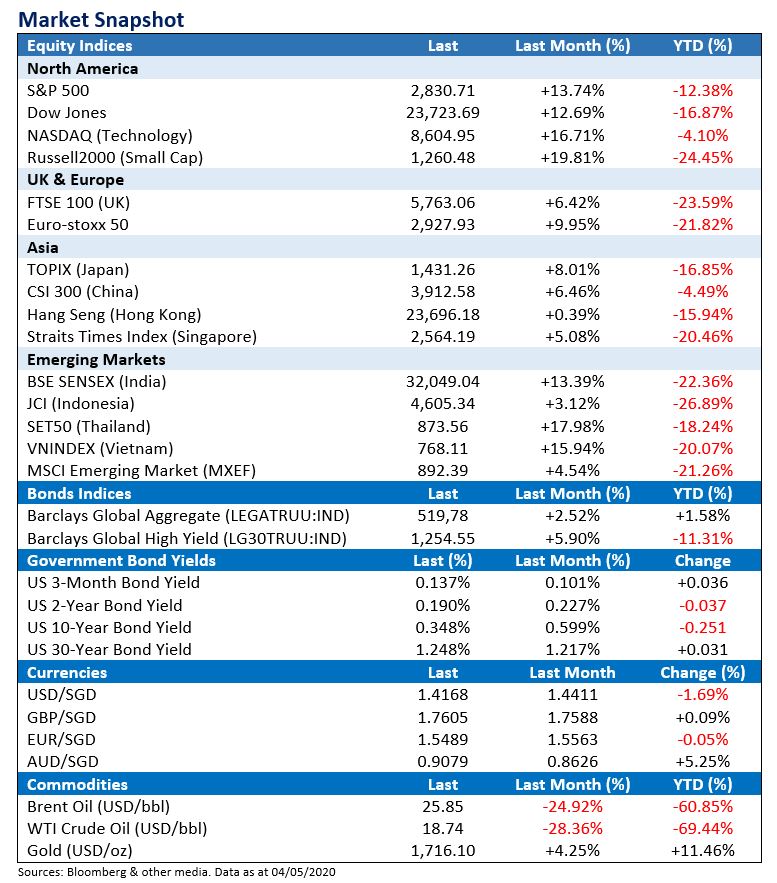

As of 30th April, the S&P 500 closed at 2,939, gaining roughly 34% from the 23rd March lows of 2,237 and equivalent to a 61.8% retracement from its 19th February highs of 3,386, a critical resistance level according to one of the most widely used technical indicator – the Fibonacci retracement level.

The DJIA and Nasdaq also painted similar picture, whereas the Russell 2000 US small companies index lags its large cap peers.

With the real economy in ruins and record unemployment in the foreseeable months ahead, yet financial markets continue to charge higher to almost pre–Covid–19 levels as if the virus pandemic did not happen at all.

Could this be an excessive case of optimism by investors after unprecedented central bank intervention and coordinated government response, one which could turn the recent rally into a typical dead–cat bounce as equity markets resume its decline? Or perhaps the financial markets truly do see beyond the economic conditions and we are in the start of a new bull market?

United States

The world's largest economy reported its deadliest day on 1st May as 2,909 people died of Covid–19 in 24 hours and with confirmed cases topping 1.18 million as of 4th May 2020.8

Meanwhile, US state governors weigh reopening parts of the economy and easing stay–at–home orders as protesters in at least 10 states such as California, Florida, New York, New Jersey & Illinois demanded that the government lift emergency measures. Dozens of states have also unveiled reopening plans and several states including Georgia, Texas, South Carolina and Tennessee have already begun to allow non–essential retailers to reopen.9

When Warren Buffett speaks, the world listens. In a four–hour live–streamed presentation at Berkshire Hathaway's 2020 annual shareholder meeting, the “Oracle of Omaha“ reassured investors that the US economy will withstand this global pandemic as it has with all of the previous battles and crises.10

While the legendary investor has sold all its airline stocks, citing a possible fundamental change due to the pandemic, Buffett has yet to make any big investments despite the recent crash and have been sitting on a massive cash pile of $137 billion by the end of March due to the uncertainty and lack of attractive opportunities.10

China

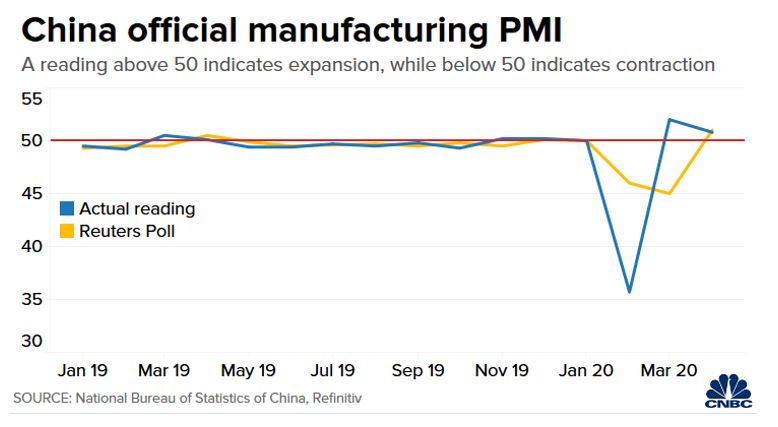

China's National Bureau of Statistics said manufacturing activity in the country expanded slightly, reporting official manufacturing PMI of 50.8 for the month of April as compared to 52.0 in March and a record low of 35.7 in February due to the large–scale lockdown implemented from late January to slow the spread of the Covid–19.11

The National Bureau of Statistics said that the recovery in demand was weaker than the recovery in production and especially true in sectors like textile, apparel manufacturing and chemical raw materials production. It also flagged heightened uncertainties in the export market with some factories reporting cancelled orders and that China's foreign trade and economic recovery is now facing greater challenges due to shrinking foreign demand despite domestic epidemic being largely contained.11

In response, the People's Bank of China (PBOC) has reduced its one–year loan prime rate (LPR) by 20 basis points to 3.85% while the above–five–year LPR fell 10 basis points to 4.65%, in line with market expectation. The reduction demonstrates China's resolve to offer targeted monetary support for the real economy, especially small, medium and micro–sized enterprises rather than real estate speculation and will step up the use of tools including reserve requirement ratio (RRR) cuts and re–loans.12

The PBOC's current approach is more moderate and measured compared to the US Federal Reserve's steep rate cuts and quantitative easing as the Chinese government refrained from introducing massive monetary and credit stimulus package in line with its deleveraging campaign since 2016. Instead, China is expected to lean on fiscal stimulus and public spending to spur infrastructure investment and consumption as stimulating domestic demand plays the main role in pumping up the economy.12

At the same time, China will step up development of 5G, artificial intelligence and other technologies at a massive scale known as “new infrastructure”, as announced by President Xi Jinping on 23rd April. Xi also announced the launch of a pilot program for China's upcoming digital yuan currency to be issued by the PBOC with the focus on making digital payments faster and easier, with speculation that it could potentially help to internationalize the yuan.13

Other central banks around the world including the UK and Japan have been assessing what their own digital currencies might look like, but China appears to be ahead of the pack.13

Europe

The euro zone economy contracted by 3.8% in 2020Q1 compared to 2019Q4 and is the lowest since records began in 1995 as the Covid–19 pandemic severely impacted business activity in the region.4

The 19–member euro area is one of the hardest–hit by Covid–19. Germany, France, Spain and Italy – the four largest euro economies – are among the top six countries worldwide with the highest number of infections. Strict lockdown measures in most of the euro area have meant that all non–essential services have been closed for several weeks.4

Germany, eurozone's largest economy, reopened some retail business in late April, but the government said that the country is on track for the worst recession since World War 2. Berlin has slashed its GDP forecast for 2020 to -6.3% from its January growth estimate of 1.1%.4

France, eurozone's second–largest economy, enters technical recession as it contracted 5.8% in 2020Q1 compared to 2019Q4, logging the sharpest decline since records began in 1949. The country is lifting some of its lockdown measures from 11th May, but analysts have raised concerns that France will face much bigger economic challenges than Germany due to its bigger services sector and a smaller fiscal response from the French government.4

Unemployment rate across the eurozone rose to 7.4% in March from 7.3% in February and data releases from Eurostat also showed that inflation could drop from 0.7% in March to 0.4% in April.4

Rest of Asia

Within Asia, the Japanese and Singaporean economies could struggle the most in the coronavirus pandemic, according to Steve Cochrane, chief Asia Pacific economist at Moody's Analytics. Both economies were already weak before the outbreak worsened over the past month and stricter lockdown measures imposed to contain the virus spread will likely exacerbate their respective economic troubles.14

Worsening economic conditions and softening export trends in North Asia will result in a tough second quarter for the whole APAC region and the International Monetary Fund also warned that for the first time in 60 years, Asia – one of the fastest–growing regions in the world – will not register any growth this year due to the coronavirus pandemic.14

Central Banks

US Federal Reserve – In the latest Federal Open Market Committee meeting on 29th April, the central banks said it would maintain its current interest rate target between 0% – 0.25% as it pledged to keep rates near zero until full employment returns and inflation gets back to around the Fed's long– stated 2% goal.2

Federal Reserve Chairman Jerome Powell also said there is a need for more stimulus for a robust economic recovery despite already launching a variety of programs that total more than $2 trillion aimed to get money to businesses and households in need.2

The Fed is also expanding its Main Street lending program, opening it to larger businesses and broadening the types of loans that will be available. Previously, the program was limited to mid–sized companies with up to 10,000 workers and $2.5 billion in revenue but have since raised to 15,000 employees and $5 billion in revenue.3

European Central Bank – The ECB said that it had kept interest rates unchanged but was ready to increase its coronavirus stimulus program if needed, as the euro zone faces a deep economic crisis that is expected to contract between 5% and 12% this year.5

The central bank also announced that it had reduced costs for commercial banks to support lending activity by further reducing lending rates to as low as -1% – effectively paying banks to borrow money, with the aim to encourage banks to lend to customers to stimulate the real economy.5

ECB President Christine Lagarde also indicated that the Pandemic Emergency Purchase Programme (PEPP) – a 750–billion–euro stimulus package announced in March to purchase government bonds – will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions.5

Other Central Banks – Elsewhere, other central banks such as Bank of Japan and Bank of England joins the Fed and ECB with “do what it takes” mantra to combat the economic turmoil.6

Medical Solutions

Treatment to lower fatalities – On 1st May, US President Donald Trump announced that the US Food and Drug Administration (FDA) granted emergency use authorization (EUA) for Gilead Sciences' remdesivir drug to treat Covid–19. New clinical trial data suggests that the drug has helped shorten the recovery time of some hospitalized Covid–19 patients. While the EUA means that remdesivir has not undergone the same level of review as an FDA–approved treatment, doctors will be allowed to use the intravenous drug for either a five–day or ten–day dose, with the ten–day treatment regimen preferred for intubated patients.7

Vaccine development – Moderna, one of the few biotech companies in the forefront of the race to develop a vaccine to combat Covid–19, has announced a 10–year partnership with Swiss drugmaker Lonza to accelerate production of the experimental vaccine, called mRNA–1273, as early as July this year. It was the first company to enter a phase 1 human trial in March and while full results have not been released, data from the phase 1 trial “looks positive” with regard to safety and Moderna has submitted an application to the FDA to move to a phase 2 trial and its phase 3 trials could be as soon as 4“th” quarter of 2020.15

However, according to Dale Fisher, chair of the WHO Global Outbreak Alert and Response Network, a vaccine for Covid–19 is unlikely to be ready until end of 2021 because of the necessary phase 2 and 3 trials to guarantee both safety and efficacy, ramp up in production and distribution, as well as administering the vaccine.17

Until a vaccine is ready, individuals must understand the role they have to play in public health instead of just relying on contact tracing. Simple efforts including social distancing and not heading out when sick is extremely important and necessary in the new normal.17

What lies ahead?

If patterns throughout history continues to repeat itself, the month of May through to October, dubbed the “summery six–month period” is also the period where stock markets posted lower returns compared to the November to April “wintery six–month period”. Hence there is a common investment adage to “Sell in May and go away, and come back on St. Leger's Day”.16

While this phenomenon has been observed from 1950 to around 2013, since 2013, statistics suggest this seasonal pattern may not be the case anymore and those who follow it may miss out on significant stock market gains.16

So, instead of selling in May and going away, one strategy is to stay invested in equities and continue to accumulate during the dips. Another strategy is to switch to defensive asset classes such as Treasuries or Investment Grade bonds such as the LionGlobal Singapore Fixed Income Investment or Eastspring US Investment Grade Bond, which have returned a year–to–date performance of 4.49% and 5.60% respectively as of 4th May 2020, outperforming the Barclays Global Aggregate's YTD gain of just 1.58%.

We hope that as you watch intently on how the impact of the coronavirus would unfold in the following weeks and months along with how your portfolio value would fluctuate with each positive and negative development, don't forget to stay calm and invested with dollarDEX. Over the long haul, the coronavirus situation will be a thing of the past and stock markets will rise again.

If you are not confident of timing the market, one good way is to invest in smaller tranches or set up a Regular Savings Plan (RSP) on dollarDEX to smooth out the volatility and take the emotions out of investing. It is also important to have a diversified portfolio to avoid concentration risk in a particular sector or region.

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 12/05/2020.

-

4 https://www.cnbc.com/2020/04/30/euro-zone-gdp-q1-2020.html

-

5 https://www.cnbc.com/2020/04/30/ecb-april-rate-decision-amid-coronavirus-crisis.html

-

6 https://www.cnbc.com/2020/04/27/bank-of-japan-expands-stimulus-again-as-pandemic-pain-deepens.html

-

7 https://www.cnbc.com/2020/05/02/who-us-just-reported-deadliest-day-for-coronavirus.html

-

8 https://www.worldometers.info/coronavirus/?utm_campaign=homeAdvegas1?

-

9 https://www.cnbc.com/2020/05/02/who-us-just-reported-deadliest-day-for-coronavirus.html

-

12 http://www.china.org.cn/business/2020-04/21/content_75956544.htm

-

16 https://www.investopedia.com/terms/s/sell-in-may-and-go-away.asp