THE WORLD'S MOMENTUM SHIFTS. AGAIN.

April proved to be a mixed month for equities as investors grappled with the lingering trade dispute between China and the US and rising political tensions in the Middle East, and by the end, Developed Markets outpaced Emerging Markets.

THE WORLD IN FIVE BULLET POINTS

• The tit-for-tat trade tariffs between the US and China that began in March continued into April with equity markets first feeling the downward pressure of the threat of escalation before compromising signals from both sides spurred a recovery. China’s President Xi also reiterated his pledge to open the Chinese market to foreign competition.

• President Moon Jae-in of South Korea and President Kim Jong Un North Korea held an historic meeting at the border between the two countries that are still technically at war with each other. Substance was light but symbolism high with President Kim being the first leader from the North to set foot in the South since hostilities stopped in 1953. The reason for the rapprochement will be debated for years however it is likely that China’s move to turn off the oil taps in March and a possible collapse of the North’s nuclear testing site provided enough of an incentive for Kim to cool his heels and head for the negotiating table.

• The US and several of its allies bombed targets in Syria in retaliation for a chemical weapons attack on Douma, a civilian neighbourhoodin Damascus. Although the strikes were limited, the diplomatic fallout with Russia is still in the balance as the US then imposed sanctions on several oligarchs connected to the Putin government in Moscow. After the strike and sanctions, oil prices tipped three-year highs while aluminium soared (see story below).

• China and Japan also met for the first time in a while. In fact, it was the first meeting between trade officials from Japan and China in eight years and the talks couldn’t have come at a more sensitive time amid an increasingly tense trade conflict between Japan’s second-largest trading partner, the US, and its largest, China.

• Later, embattled Japan prime minister Abe visited President Trump in the US in which trade was one of the topics discussed. Domestically, the prime minister was continuing to fight questions over favouritismand nepotism hanging over his head: political analysts suggested Abe was unlikely to win his party’s leadership election in Septemberso would be unable to become prime minister in subsequent general elections.

EQUITY MARKETS

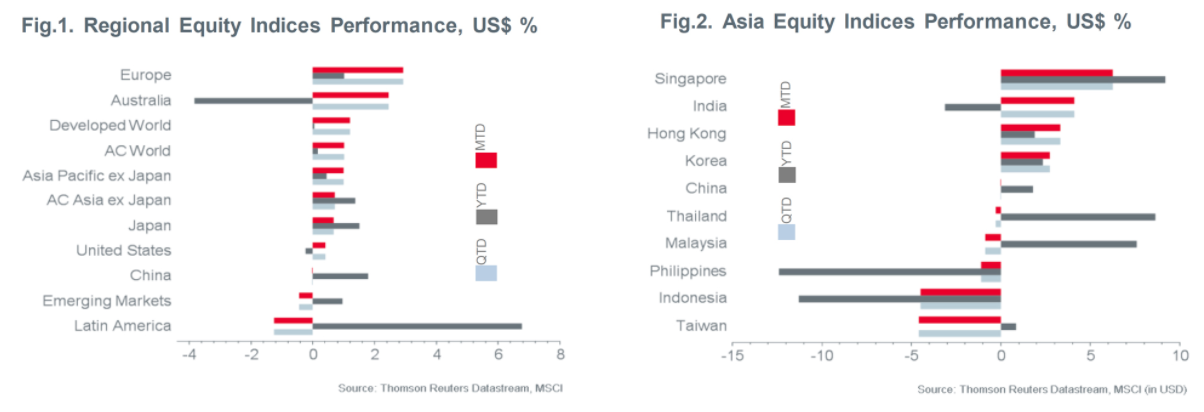

• Equity markets around the world were mixed in April with the MSCI World index up just 1.0% as investors grappled with the lingering trade dispute between China and the US, rising geopolitical tensions in the Middle East, especially in Syria as Iran and Israel eyed each other up, and a mixed set of economic and corporate data from around the world keeping the lid on gains.

• The MSCI Developed Markets index was up 1.2%, outperforming Emerging Markets by 1.6%. Within EM, Asia Pacific ex Japan was 1% higher, outperforming Latin America, down 1.2%, and EMEA, which lost 2.3% as Russia and Turkey both fell sharply. Stocks in Korea were noticeably higher on the talks between the North and South.

• Among Developed Markets, Europe outperformed the US with the UK, France and Italy notably higher than Germany, which fell on weaker-than-expected economic news. The US gained just 0.4% with traders reporting concerns on profit margins weighing on stocks. Against this, Facebook and Amazon rallied strongly in the final week as they easily beat profit forecasts.

• Underperforming Asia markets in April included China that was flat and which saw its technology stocks pulled down by the threat of US sanctions and a specific investigation into Huawei. This added to concerns that investors were already having over a trading sanction against ZTE. Taiwan was also weaker after TSMC disappointed with a weak Q2 outlook statement, dragging the Apple supply chain down with it. Singapore is now the region’s best performing regional index year to date with a 6.3% return.

• The Philippines market fell again although did rally toward the end of the month as President Dutertefiled part two of his Comprehensive Tax Reform Programmewith Congress. The bill is aimed at funding a $160bn infrastructure drive but has also hit a swathe of the country’s exporters. The MSCI Philippines index fell 1.1% and the local PSI fell 2.0%.

FIXED INCOME

• 10-year US Treasuries yields commenced a steady climb over the month, peaking at 3.03%, the highest in more than four years, before ending the month at 2.95%. The year-to-date rise in yields reflects market expectations of increased inflation driven by stronger commodity prices, the perception that wages will accelerate, and underpinned in April by better retail sales, strong housing starts data and larger Treasury auctions. Investment grade corporate bond yields also hit 3%, the fist time in eight years this has happened.

• Concurrently, the spread between the two-and 10-year Treasuries hit a multi-year low of 41 bps. This made the dreaded inverted yield curve, when short-term rates are higher than long-term yields and, historically, a recession often follows, closer to hand.

• In Asia, performance of Asian USD-denominated bonds turned negative, as accrual income and generally wider spreads failed to offset rising risk-free benchmarks. High-grade outperformed high-yield, again supported by a flattish curve and risk-averse sentiment. Overall, the representative JPMorgan Asia Credit index fell by 0.66%.

COMMODITIES

• Crude pushed through three-year highs to touch $75 per barrel, a price not seen since November 2014. Continuing production cuts by OPEC, record high levels of demand from Asia and question marks over future supply from Iran offset the high US dollar and record US shale production to send WTI up 7% over the month.

• Aluminium prices spiked to six-year highs after the US imposed sanctions on Russian companies including Rusal, the world’s second largest aluminium producer owned by Russian billionaire Oleg Depriaska. The timing coincided with an industrial dispute at a major alumina refinery in Brazil, which sent alumina prices soaring too, leading some to speculate on potential future shortages of aluminium.

• And then almost as quickly, the US reversed course and talked about watering down the sanctions…aluminium prices fell back just as quickly although they did stay at elevated levels. Year to date, aluminium futures prices are almost flat.

• Nickel prices also soared on what some analysts said was misplaced concern the metal would become ensnared in the sanctions against Russia. On one day, prices increased 7.5% to record its largest gain in more than six years but some traders speculated that some Chinese traders had misread a London Metal’s Exchange headline on Russian producer Nornickel. Palladium, another Russia-linked metal, also rose strongly.

CURRENCIES

• Rising yield differentials and the 10-year US Treasuries break above the psychological 3% barrier also prompted a turnaround in the US dollar, which, measured by the Dollar Index (DXY) gained 2.1% month on month. Strong US economic data versus weaker Eurozone data and weaker still UK data caused the spike. Almost all Emerging Market currencies fell against the greenback with the Russian ruble down 10% and the Brazilian real down 6%.

• The euro fell over the month to give up some of its first quarter gains. Against the US dollar, it fell 1.8% easing pressure on the region’s exporters and helping to deliver an outperformance in the equity markets. The UK pound also fell 1.8% against the dollar, leading to a 4.8% return in UK equities over the month as exporters gained.

• Asia currencies fell with the exception of the Philippine peso which rose around 1% on speculation of a rate hike to counterinflation and a rating agency upgrade. The Indian rupee saw a 2% drop as the oil price rose while the Taiwanese dollar fell on an exodus of fund flows after technology stocks disappointed in their outlook statements.

• The Mexican peso plunged after an opinion poll pointed to the left-wing candidate consolidating his lead ahead of Presidential elections on 1 July. The Turkish lira also fell on news that President Erdogan had called snap elections for June.

ECONOMICS

• US economic data remained robust: Q1 GDP growth was higher than expected at 2.3%, slower than previous quarters but better than the 2% forecast. Core inflation for March moved above 2% with headline inflation at 2.4%; the Personal consumption index, which the Fed uses to gauge price increases is now just shy of the Fed’s 2% target, leading some commentators to speculate whether three more rate rises were likely this year. The CPI reading also pointed to a higher inflation trend, retail sales were also higher for the first time in four months but consumer spending as a whole increased by a meagre 1.1%. Unemployment is now 4.1%, the sixth month in a row at this rate and the lowest since 2000.

• But European economic datapointsunderwhelmed. The March Manufacturing PMI reading hit the lowest point since early last year even if the reading of 56.2 pointed to continued underlying growth. Quarterly GDP growth fell to 0.4% from 0.7% in Q417. And while economists pointed to temporary factors such as poor weather in northern Europe as the reason for a blip in the poor figures, ECB President Mario Draghi did acknowledge slowing growth in his accompanying statement to the ECB’s decision to keep rates on hold. In the positive column, unemployment fell sharply in Italy, France and Spain while southern countries’ GDP growth was also stronger, implying underlying growth throughout Europe is still robust.

• Expectations of a rate increase in the UK fell after inflation fell to 2.5% and retail sales dropped by 1.2% in March. Later,GDP growth figures pointed to an expansion of just 0.1% in Q1, weighed by weakness in the construction sector. Investors had pencilled in a 25 basis point rise for May but that decision now appears more up in the air than grounded in certainty.

• The Bank of Japan kept its monetary policy measures unchanged, with short-term interest rates on hold at -0.1% and long-term rates at 0.0%. The only major surprise was the BoJpolicy-setting committee removing its timetable for achieving its 2% inflation target, leaving the door open for 10-year yields to stay at zero for longer than first thought.

• Chinese new export figures falling short while PMI figures also fell. But China’s inflation figures also came in below forecasts while its economy grew by 6.8% in Q1 -faster than expected and higher than the target of 6.5% for the full year as manufacturing data bounced and consumer demand remained robust. Both are expected to dip in the coming months after the clamp down on shadow banking and the effects of the trade disputes with the US kick in.

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only)by Eastspring Investments (Luxembourg) S.A. - UK Branch, 125 Old Broad Street, London EC2N 1AR.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments.

It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.