MAINSTREAMING ESG INVESTING IN ASIA

Eastspring Investments recently became a signatory to the United Nations endorsed Principles for Responsible Investment (UNPRI) after three years of planning and preparation. Eastspring is by no means the first organisation in Asia to become a UNPRI signatory1, nor, we hope, the last.

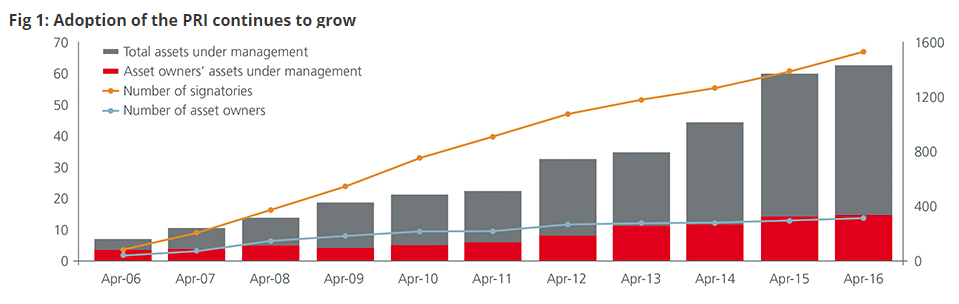

In 2016, of the asset owners, investment managers and service providers which had signed up to the UNPRI, 236 signatories were from Asia Pacific, accounting for 14% of the total. Asia ex-Japan saw a year-on-year growth of 36% in PRI signatories in 2016.2

Globally, assets managed under Socially Responsible Investment (SRI) strategies stood at USD23 trillion at the beginning of 2016, including exclusionary screening. More importantly, however, ESG-integrated (Environmental, Social and Governance) assets under management grew 38% to USD10.4 trillion globally between 2014 and 2016. Furthermore, sustainability-themed investing grew close to 140% over the same period.3 The bulk of these assets come from Europe, but there is a ramp up in other parts of the world including the US and developing markets.

Asia’s SRI assets under management were around USD500 billion in early 2016. Currently, that figure is likely closer to USD1 trillion.4,5 However, Japan alone counts for nearly 85-90% of the Asian SRI AUM (Assets Under Management).

Asian and Emerging Markets asset owners outside of Japan have been slow to adopt the UNPRI, while asset managers in the region have also lagged European, North American and Pacific counterparts in adopting ESG investing policy.

Not only was the region lagging in the absolute investment amount, the 16% pace at which such investment grew in the two years to 2016 was also moderate, compared to 33% in the US and 12% in Europe, especially considering that it was from a low base.6

WHAT IS ESG?

ESG is best seen as founded in a holistic approach which comprises tools to incorporate critical factors into the investment analysis and decisionmaking process by investors and companies across industrial sectors. Both support and complement each other for achieving the goal of a sustainable financial and economic system.7

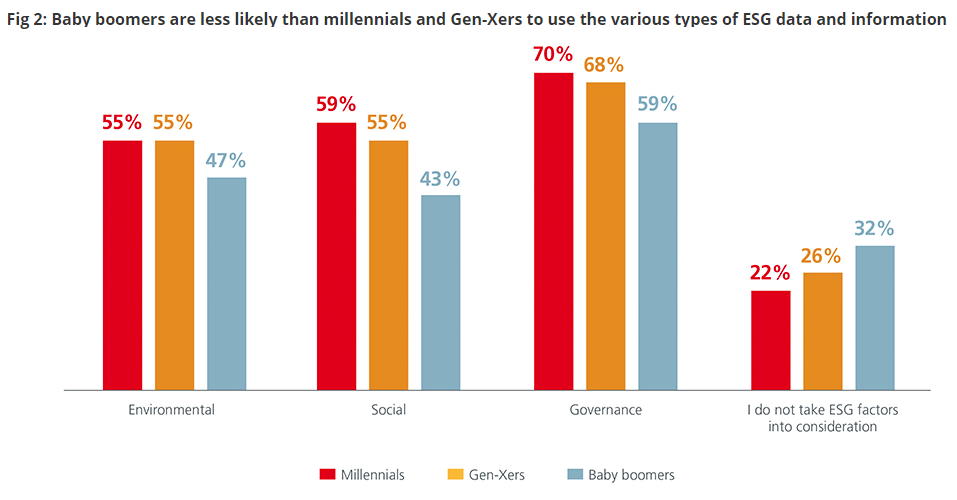

A recent meta study found overwhelming support for ESG and CSR investing after reviewing more than 100 academic studies and additional meta studies, citing benefits in the form of superior risk adjusted returns, lower cost of capital, and both market and accounting-based outperformance. The authors found that 89% of studies show that companies with high ESG scores outperform over periods ranging from 3 to 10 years.8 Employees9 and Investors10 overwhelmingly want such policies and the disclosure as well, according to other studies. Millennials as investors are twice as likely to invest in companies or funds that target specific social or environmental outcomes.11

WHY IT MATTERS?

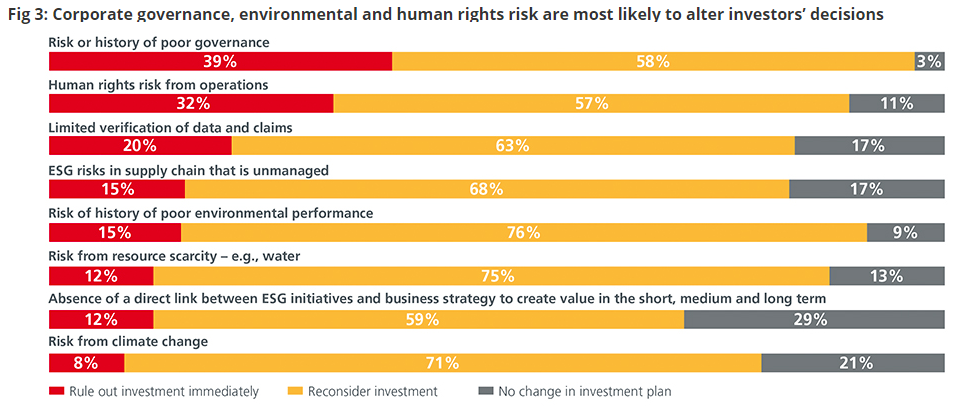

According to a survey, certain disclosures about a prospective investment will affect investors’ decisions; 39% of the investors will rule out an investment immediately if there is a history of poor governance while 32% will do the same if it is a human rights issue.

OBSTACLES TO ASIAN ESG?

There are several reasons a corporate board or management team might hesitate to embrace ESG.

The lack of a standardised and objective way to implement ESG policy and measure the results poses a daunting prospect to many.

ESG policy is still evolving12 and the focus has shifted over the years from concerns about worker and product safety to other ESG issues, such as changing societal expectations, impacts of disruptive technologies, changing demographics, scarcity of water and other resources, climate change and post financial-crisis executive pay. In addition, questions on how these get measured, calibrated and compared across a sector and geography and over time can also raise challenges.

Asian asset owners and governments display weaker leadership in enforcing governance standards and pushing corporates into ESG friendly policies versus their peers in the US and Europe.

There has been a noticeable lack of broad leadership by major asset owners in Asia outside of Japan although Singapore, Hong Kong and Taiwan have also embarked on the ESG journey through investor stewardship codes and exchange regulations. If asset owners such as government pension funds and sovereign wealth funds, major corporate pension funds, foundations and endowment funds insist on ESG-friendly investment policy, it will encourage Asian corporates to integrate ESG in their investment activities.

Asia has a more hierarchical relationship between investors and management, often preventing dialogue about ESG improvements, especially governance issues.

The Asian Society of Corporate Governance believes that the controlled and hierarchical management/shareholder communication system in Asia may be a factor impacting corporate governance and capital market development.

Japan and several other markets developing investor stewardship codes appear to agree.13 In addition, further complication stems from the fact that Asia has many listed companies which are still under family control14 where the commitment to “G” in ESG may threaten long established cultural pillars. For example, commitment to transparency may bring unwelcome scrutiny to related party transactions, cross-shareholdings, minority shareholder rights and other issues.

THE CASE FOR ESG INVESTING IN ASIA

Asia is the biggest consumer of world resources. As the world’s biggest regional economy, it is expected to grow at 5.4% in 201815. Asia is home to 60% of the world’s population, yet it has only 30% of its land area16 and 36% of its water17; it must import fuel, water, food and raw materials for production and survival. China is expected to remain the world’s largest electricity user after having become so in 2011, while India will have the next highest consumption growth rate over the next 24 years.18

While North American sourced air pollution was declining, Asian air pollution contributed as much as 65% of the western US ozone increase. Since 1992, Asia has tripled its emissions of smog-forming chemicals such as nitrogen oxides. Though China and India are the worst offenders, North and South Korea and Japan also contribute.19

On a per capita basis, China and Japan consume more seafood than India, the EU and the US combined.20 Korea ranked 15th, Vietnam 14th and China 13th in 2016’s world meat consumption per capita ranking table.21

Asia’s climate change exposure is also important and will increasingly become a factor taken into account by investors to evaluate competitiveness both at the country and the corporate level. With agriculture and fisheries exposed to droughts, and coastal populations to sea level changes and tropical cyclones, Asia’s vulnerability to climate change will also bring increased migration, potential challenges to urbanisation, supply chains disruption and potential new health threats.

Longer term, those companies which choose not to uphold ESG standards are unlikely to thrive and perhaps even cease to exist. If they don’t selfpolice, natural attrition, market forces and even international pressure may determine their fate as the world becomes increasingly global, and stewardship of resources and the environment impact larger audiences.

PROGRESS TOWARDS A LONG-TERM ORIENTATION AND SUSTAINABLE BUSINESS MODEL

More and more clients look to their asset managers to consider ESG issues when investing. According to a recent report cited by The Asset, 25.7% of the world’s ESG AUM were held by retail investors in 2016, a 96% increase compared to 2014.22 Although ESG policy and compliance may not appear directly in companies’ financial statements, investors and asset owners will increasingly ask for evidence of their risk exposure as measured by various indicators, such as carbon footprint, overlap with ESG indices and evidence of engagement beyond proxy voting with companies on key issues. If the potential risk adjusted return is not favourable, some investors might “boycott” specific stocks or sectors, like we have seen with companies engaged in fossil fuel and palm oil extraction.

In China, regulatory bodies have started to actively promote the ESG concept and its development through international exchanges, training, and developing their own policy and regulatory initiatives. The China Securities Regulatory Commission has set out a timetable which will require all listed companies to mandatorily disclose environmental information by 2020.23

In the past four years, six Asian countries— Hong Kong, India, Malaysia, Singapore, South Korea, and Taiwan—have adopted investor stewardship codes.24 South Korea’s NPS has also become a signatory to the UNPRI code and Taiwan’s Bureau of Labour Funds (BLF) has set aside USD2.4 billion for the Global ESG Quality Fix Equity Indexation mandate.25

Both the Singapore Stock Exchange (SGX) and Hong Kong Stock Exchange (HKX) have recently requested that all listed companies submit sustainability reporting or justify their reasons if they choose not to do so.26 The Hong Kong rules required all listed companies to comply or explain with ESG disclosure guidelines in 201727, extending specifically to emissions reporting in 2018. Only 21 of 635 Hong Kong-listed Chinese companies reported carbon at the beginning of 201728. Singapore Exchange rules took effect in 201829 with more than 90% of investors surveyed by Singapore Exchange reporting that they consider ESG factors, underscoring their importance.

An early adapter, Taiwan introduced its investor stewardship code in 201630, which followed 2015 sustainability reporting rules31 for large companies and certain sectors, with the goal to expand to 90% of members by market value by 201732.

In addition to policy leadership, we believe innovative technologies can help mitigate some of the ESG issue risk for investors. We see Smart Beta and AI (artificial intelligence) as helping to resolve the challenges presented by climate change, for example, through timely big data availability, better forecast of weather systems and ultimately a move to a lower carbon energy footprint.

ESG considerations are essential for long-term value creation. A safe and healthy environment, a prosperous society and flourishing communities are in everyone’s long-term interest.

Source:

1The UNPRI had more than 1,800 signatories, from over 50 countries, representing asset managers, asset owners and service providers, and approximately USD70 trillion, as at 30 April 2017.

2The Asset, page 26, as at January 2018

33Global Sustainable Investment Alliance – 2016 Global Sustainable Investment Review

4The Business Times – The rise of ESG investing in Asia, as at 28 February 2018.

5Based on SRI Review 2016 figure of USD527 billion, plus new UN PRI signatories such as ESI and China Asset Management

6South China Morning Post – Why is Asia lukewarm to sustainable investing?, as at 14 October 2017

7The Asset-ESG Forum – ESG progress faster than investors’ expectations, says PRI China country head, as at 24 January 2018

8Deutsche Bank – Sustainable Investing. Establishing Long-Term Value and Performance, as at June 2012.

9Harvard Business Review – The Comprehensive Business Case for Sustainability, as at 21 October 2016.

10Ernst & Young Global Limited – Is your nonfinancial performance revealing the true value of your business to investors?, as at 2017.

11Ernst & Young Global Limited – Sustainable investing: the millennial investor, as at 2017

12Ernst & Young Global Limited – ESG goals and preferences are evolving, as at 2017.

13CLSA – CG Watch 2016. Ecosystem matter. Asia’s path to better home-grown governance, as at September 2016.

14PRI Association – PRI looks at investor obligations and duties in six Asian markets, as at 7 September 2016.

15International Monetary Fund – Asia’s Dynamic Economies Continue to Lead Global Growth, as at 9 May 2017.

16World Population Review – Asia Population 2018, as at 13 March 2018.

17Hydropolitic Academy– Water for the people, as at 31 May 2014.

18The Institute of Energy Economics, Japan – Asia/World Energy Outlook 2016, as at October 2016.

19USA Today – Air pollution in Asia is wafting into the USA, increasing smog in West, as at 2 March 2017

20Our World in Data – Meat and Seafood Production & Consumption, as at August 2017.

21Organisation for Economic Co-operation and Development – Meat consumption, as at 2017.

22The Asset, page 26, as at January 2018.

23The Asset-ESG Forum – ESG progress faster than investors’ expectations, says PRI China country head, as at 24 January 2018.

24John Hancock Investments – ESG research: The new cornerstone of emerging-market investing, as at 3 November 2017.

25The Business Times – The rise of ESG investing in Asia, as at 28 February 2018.

26Asia Asset Management – ESG: Asia leading the way on responsible investment, as at 3 November 2017.

27HKEX – Appendix 27 Environmental, Social and Governance Reporting Guide, as at 2018.

28Bloomberg Finance – Asia looks to turn tables on lagging ESG transparency, as at 27 January 2017.

29SGX – Sustainability Reporting Guide, as at 20 June 2016.

30Taiwan Stock Exchange – Stewardship Principles for Institutional Investors.

31Taiwan Stock Exchange – Taiwan first Asian market to implement mandatory GRI G4 CSR reporting from 2015, as at 12 February 2015.

32Law Source Retrieving System of Taiwan, Republic of China – Corporate Social Responsibility Best Practice Principles for TWSE/GTSM Listed Companies, as at 7 November 2014. Fig.1. PRI Brochure, as at 2016. Fig.2. Environmental, Social and Governance (ESG) Survey, CFA Institute, as at 2017. Fig.3. Ernst & Young Global Limited – Investors see long-term financial benefits in companies with high ESG ratings, as at 2017.

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated

in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary

Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial

Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is

incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments

(Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des

Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. - UK Branch, 125 Old Broad Street, London

EC2N 1AR.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and

is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected

in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific

investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not

intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be

published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this

posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic

trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by

Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of

this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring

Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages

arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without

notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the

United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial,

Inc., a company whose principal place of business is in the United States of America.