Low volatility strategies: Back in the limelight

Volatility has made a comeback. Given still healthy market fundamentals, low volatility strategies can help investors stay invested while minimising the volatility in their portfolios.

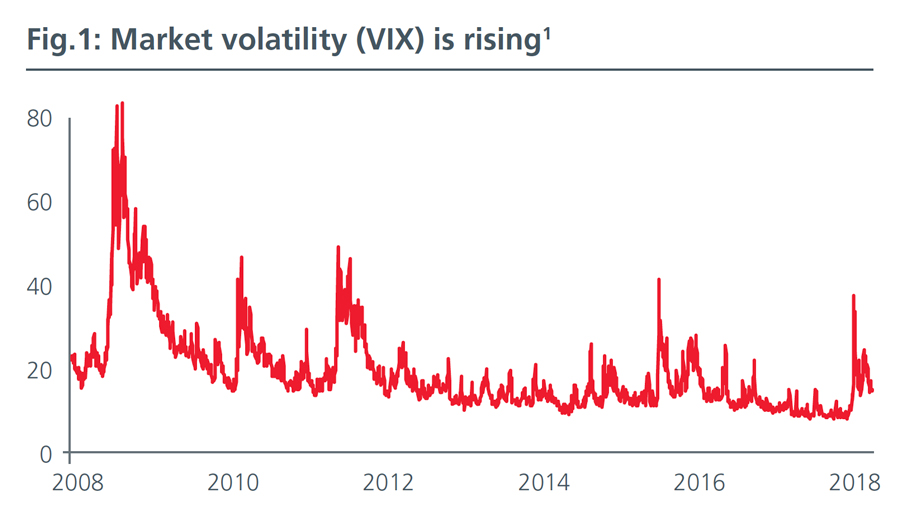

After an unusually calm period for equity markets in 2017, volatility has made a comeback. The CBOE's VIX index, a measure of implied volatility for the S&P 500, is averaging around 18% year to-date, an increase of more than 60% from last year's average level. In Asia, there have been 18 swings of at least 1% on the MSCI Asia Pacific ex Japan index in the first four months of this year, up from 14 for the full year of 2017.

High levels of liquidity have been suppressing volatility since 2010. The unwinding of the US Federal Reserve's balance sheet, trade tensions between China and the US as well as geopolitics have led to recent spikes in volatility. (See fig.1). Given these lingering concerns, investors will need to brace themselves for further volatility ahead.

At the same time, equity market fundamentals appear healthy. Asian corporate earnings are expected to grow by 13% over the next 12 months. Asia ex Japan equities are attractively valued compared to global and other regional markets. At 12.9x 12-month forward price to earnings2, the MSCI Asia Pacific ex Japan index is trading below its long term average, which has historically presented an attractive entry point for investors. With valuations suggesting that Asian equities can continue to trend higher, investors likely want to stay invested but minimise the volatility in their portfolios.

LOWER VOLATILITY, HIGHER RETURNS

Low volatility strategies contravene one of the basic theories in finance - that investors should not be rewarded with higher returns for taking on less risk.

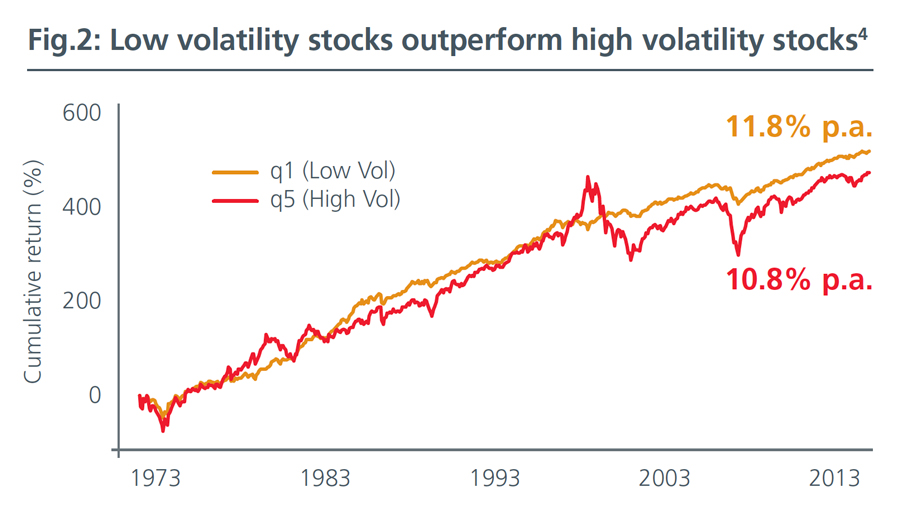

What is even more remarkable about this anomaly is that it is persistent and comprehensive. Academic research as early as 19673 supports the low volatility anomaly. Our analysis of the performance of the largest 500 US stocks from 1973 to 2016, shows that low volatility stocks outperformed higher volatility stocks. (See fig.2). Further analysis shows similar results across multiple regions and countries.

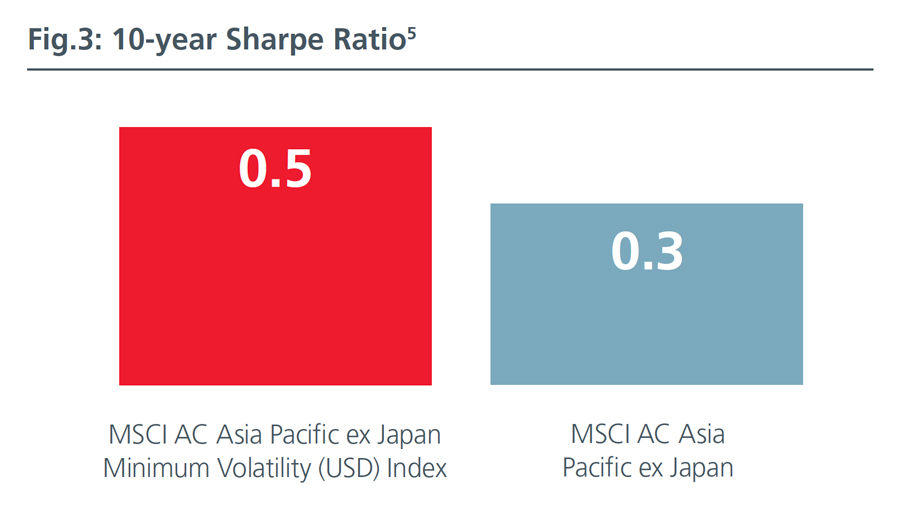

The higher return-lower volatility characteristics result in higher Sharpe ratios for low volatility stocks, of which the figures for Asia can be seen in Figure 3.

The persistence of the low volatility anomaly is an ongoing research topic for academics and practitioners alike, but there is reason to believe it is partly driven by behavioural biases. Some of these biases include the following:

Lottery effect

Investors tend to overpay for risky stocks in the hope that they yield large returns even though the probability associated with achieving those returns may be low. Conversely investors tend to ignore lower risk stocks which deliver lower returns even though the probability of achieving those returns may be higher.

Representativeness

Studies on behavioural finance suggest that the brain uses short cuts to analyse large volumes of information quickly. This results in stereotyping. This is why investors tend to overpay for high volatility stocks in glamorous sectors but ignore the speculative nature of such stocks.

Overconfidence

An exaggerated belief in one's ability and skills can lead investors to favour risky equities as those stocks will potentially offer the highest payoff if the investing hypothesis turns out to be right.

STABILITY WINS

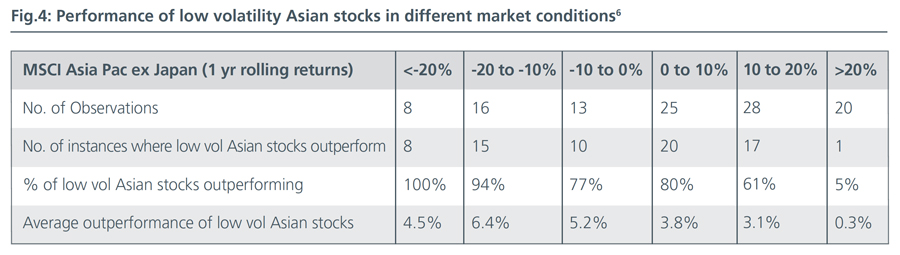

Low volatility Asian stocks have historically outperformed the broader market in most up and down market environments, except in cases where the 1-year returns from Asian equities were abnormally strong, in excess of 20%. (See fig.4).

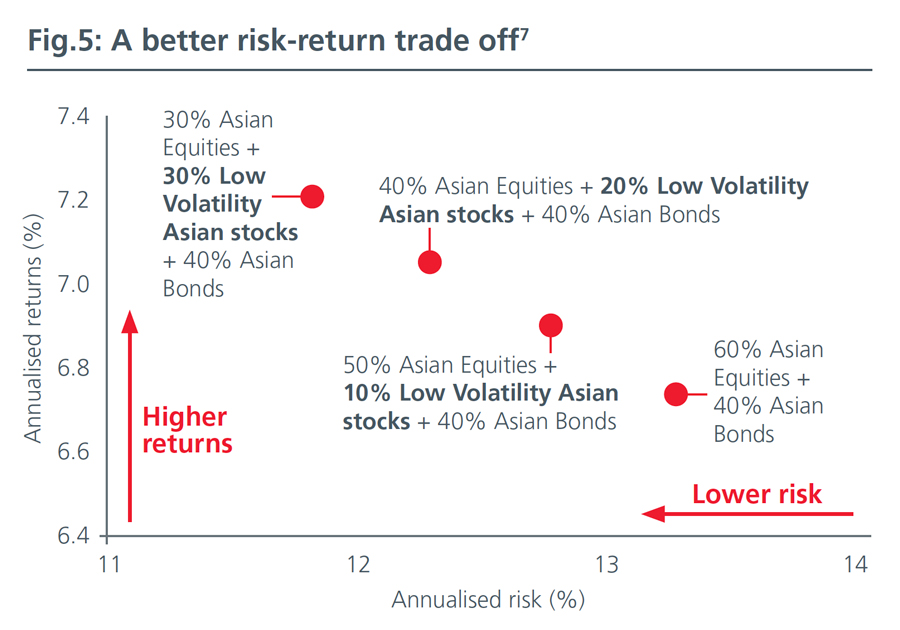

By simply replacing some exposure in Asian equities with a low volatility Asian equity strategy, the resulting portfolio can achieve higher returns but with lower volatility. (See fig.5).

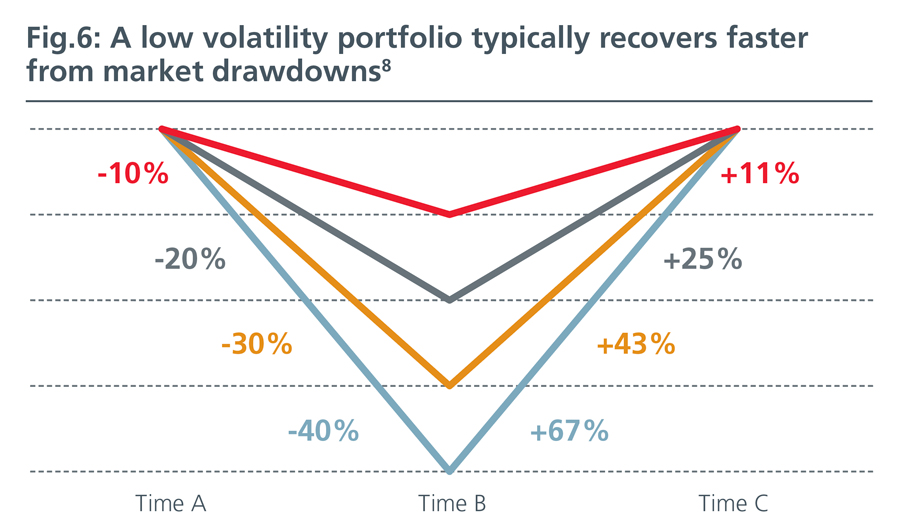

Staying true to its name and falling less during turbulent times, a low volatility portfolio needs only to rise by a smaller magnitude in order to return to the same level. Through compounding, the low volatility portfolio potentially accumulates more wealth over the long term. (See fig.6).

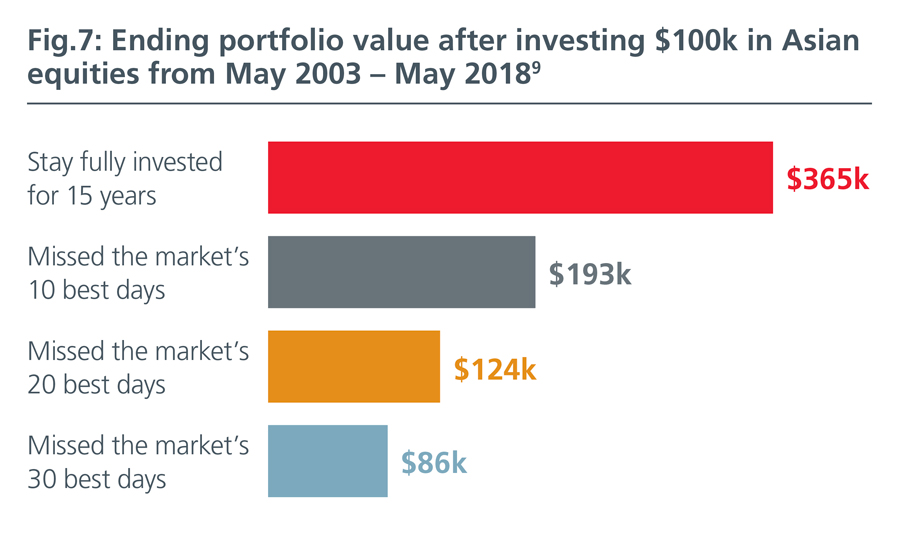

Low volatility strategies help temper the volatility in portfolios, thereby allowing investors to stay comfortably invested during turbulent times. By not trying to time the market, investors reduce the risk of missing the market's best days which can significantly lower their overall returns. An investor who started with $100k and stayed invested in Asian equities over the last 15 years, for example, would have earned $172k more than someone who missed the market's 10 best days. (See fig.7).

VALUATIONS MATTER

As with all investment strategies, valuations matter. A study10 which examined the risk and return outcomes of the lowest and highest risk quintile stocks in the US over 540 months (45 years) showed that while low volatility stocks tend to outperform high volatility stocks, they are most likely to do so when low volatility stocks are reasonably priced.

With the MSCI Asia Pacific ex Japan Minimum Volatility index trading at a 16% premium11 (12-month forward price to earnings ratio) to the broader market, valuation considerations will be especially important. Active managers who are not constrained by the benchmark universe can have a broader opportunity set of more attractively-priced stocks to choose from to generate excess returns for investors.

CONCLUSION

Market volatility is likely to rise as central banks withdraw their unconventional stimulus. This will present a buying opportunity, as long as the spike in volatility does not adversely affect the real economy. Low volatility strategies allow investors to stay invested in equities but at reduced levels of volatility. Investors will also need a long-term horizon to enjoy the effects of compounding and benefit more fully from the low volatility anomaly.

Source: 1Bloomberg. As at 2 May 2018. 2MSCI. As at 30 March 2018. 3Pratt, Shannon P. 1967 [2008]. "Relationship between Variability of Past Returns and Levels of Future Returns for Common Stocks." Business Valuation Review, Summer 2008, Vol. 27, No. 2, pp. 70-78. Written in 1967 (unpublished). 4Eastspring Investments, Thomson Reuters, S&P. Based on cumulative sum of monthly quintile returns from May 1973 to December 2016. The lowest and highest volatility quintiles are shown above. Quintiles are formed based on the prior 60-day volatility. The universe is the largest 500 stocks listed on US exchanges at each date in history. This is an approximation for the S&P500 universe. 5MSCI. As at 30 March 2018. 6Bloomberg. Monthly returns from March 2009 - March 2018 in US dollars. Past performance is not a guarantee of future returns. Low volatility Asian stocks are represented by MSCI Asia Pacific ex Japan Minimum Low Volatility. 7Datastream. Asian Equities – MSCI Asia Pac ex Japan. Asian Bonds - JPM JACI Investment Grade Corporates. Asian Low Volatility Stocks – MSCI Asia Pacific ex Japan Minimum Volatility. For a 10-year period as at 7 May 2018. 8Eastspring Investments. The above is an illustration and should not be construed as an indication of fund performance. 9Bloomberg. In USD terms. Asian Equities - MSCI Asia Pac ex Japan. Past performance is not a guarantee of future returns. As at 3 May 2018. 10Luis Garcia-Feijoo, Lawerence Kochard, Rodney N. Sullivan, Peng Wang, 2015. "Low-Volatility Cycles: The Influence of Valuation and Momentum on Low-Volatility Portfolios". 11MSCI. As at 30 March 2018..

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. - UK Branch, 125 Old Broad Street, London EC2N 1AR.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments' communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person's reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV's) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 16/08/2018.