|

Themes for a new decade - How Internet of Things (IoT) will change our world By JPMorgan Asset Management 11 May 2021

Source: Shutterstock, J.P. Morgan Asset Management.

Authors Jasslyn Yeo, Ph.D., CFA, CAIA, CFTe, Global Market Strategist, Market Insights Strategy Alexander Treves, CFA, Head of Investment Specialists – Asia, Emerging Markets and Asia Pacific Equities Elvina Lee, CFA, Head of Investment Specialists – Asia, International Equity Group Christian Mariani, CFA, Investment Specialist – U.S. Equity Jacky Cheung, CFA, CAIA, Product Strategist, APAC Product Strategy

(Article written as of 26 Feb 2021)

In Brief

Introduction In the new decade, we see a growing need for investors to focus increasingly on themes for equity investing. The reality is that there are some growing challenges for top-down allocators to make regional and sectoral equity decisions. Changes in technology, consumption patterns, regulation, market structure and competitive dynamics are driving increased stock return dispersion, both at a within-country and within-sector level. Looking through a long-run theme lens can help investors to unravel the underlying growth drivers behind an industry’s evolution, reinforcing an active bottom-up stock selection process.

As highlighted in our 2021 Long-Term Capital Market Assumptions, we see trend growth projections remaining subdued and public market expected returns over the next 10-15 years generally lackluster, necessitating A new portfolio for a new decade1. In a similar vein, we are launching this new publication, Themes for a new decade, with the objective of exploring key structural trends that we believe can fundamentally drive the future industry landscape. Investors with the ability to identify companies that can increase revenues, adapt and innovate their business models to these industry trends and capture structural growth potential can potentially enhance their public market equity returns.

In this inaugural publication, we shine the spotlight on How Internet of Things (IoT) will change our world. We recognize that the world we live in today is undergoing rapid digital transformation, and the world we will live in tomorrow will become increasingly connected with widespread technology adoption. Technological developments have connected human to device, and we are advancing toward connecting human-device–human. Here, we take a closer look at two of the most widely used applications of IoT, namely manufacturing (industrial automation) and transportation/mobility (autonomous vehicles).

Industrial automation The adoption of industrial automation (IA) is still in a nascent stage, and there remains huge secular growth potential across the robotic, vision and laser industries.

For example, according to the International Federation of Robotics (IFR), the global average robot density in the manufacturing industry has now reached 113 units per 10,000 employees. However, this is still significantly below that in Japan (364) and Germany (346), and a small fraction of that in Singapore (918) and South Korea (855), thereby suggesting that there is much room for other markets to catch up (see Exhibit 1).

China’s robot density (187) ranks 15th worldwide, but it has been the most aggressive in capacity expansion, accounting for greater than 40% of the annual industrial robot installations in 2019. Back in 2015, automation was a means for China to upgrade its manufacturing sector (“Made in China 2025”) and address its shortage of labor. Today, automation has become increasingly important in helping China to achieve self-sufficiency in high-tech manufacturing and promote productivity growth under its dual circulation strategy (the latter spurred by the U.S.-China trade tension), as manufacturing wage inflation rises.

Across the Pacific, President Biden has recently signed an executive order to “Buy American,” aimed at revitalizing the U.S. manufacturing sector and localizing supply chains.2 Since re-shoring suggests higher costs (e.g. labor costs), some U.S. manufacturers may increase automation, in order to enhance productivity and retain their profit margins.

Apart from capacity expansion, demand for automation is expected to come from capacity upgrades associated with new technologies. Industry 4.0 (Industrial Internet of Things (IIoT)) – the fourth revolution in manufacturing - follows close on the heels of Industry 3.0.

The adoption of industrial automation has enormous room for growth EXHIBIT 1: ROBOT DENSITY IN THE MANUFACTURING INDUSTRY, 2019 ROBOTS INSTALLED PER 10,000 EMPLOYEES

Source: International Federation of Robotics, J.P. Morgan Asset Management. Data reflect most recently available as of 31/1/21

Under Industry 3.0 (Digitization), most factory equipment (e.g. robots, machine tools and laser equipment) and enterprise processes have already been automated and digitalized.

However, automation technologies continue to run in silos and data flows primarily in one direction. As a result, changes in one part of the system require manual carry-over to other parts of the system.

Under Industry 4.0, IIoT will break these automation silos by integrating all parts of the system in a data loop, allowing a two-way data flow, i.e. IIoT will connect the physical system (things) with the virtual system (internet connection, digital twins). And together with artificial intelligence (AI) and 5G adoption, IIoT can significantly improve both the flexibility and productivity of automation systems, particularly in predictive maintenance, quality inspection and assurance, and manufacturing process optimization.

Investment implications Industrial automation/IIoT is on a structural growth trend, as global manufacturers try to reduce labor costs and improve operational efficiency, amid the incremental reshoring of production. While broader adoption of IIoT platforms in the manufacturing industry is expected to be gradual, there is a huge potential market size for increased automation content in robotics (e.g. robot density, robots and cobots with enhanced flexibility), vision (e.g. vision penetration, 3D vision) and laser processing (e.g. laser penetration, ultra-high power lasers). This in turn can help to generate strong revenue streams and improve margins and earnings growth, as well as the return on invested capital (ROIC) for the IA/IIoT system solution providers. Among the IA/IIoT names, we prefer those with domain expertise, as we believe the IA/IIoT leaders of today will likely remain the IA/IIoT leaders of tomorrow, given the relatively high entry barriers.

Industry 4.0 – the fourth revolution of manufacturing

Source: Shutterstock, J.P. Morgan Asset Management.

Autonomous vehicles Autonomous driving will transform the future of mobility.3 Mass market adoption of autonomous vehicles will markedly improve road safety and reduce traffic congestion and carbon dioxide emissions, enhancing the quality of lives of many.

The hard reality is that fully automated vehicles are still in the distant future.4 The technology – algorithms and software – required to provide automotive grade safety in all driving conditions is still lacking. Cybersecurity also remains a concern.

However, we do not need to reach full automation to benefit from this structural trend. Continuing advancements of automotive driving technology are making good progress in improving the safety of semi-autonomous vehicles, which are attracting a wider consumer base .

Sensor technologies/ advanced driver assistance systems (ADAS) (e.g. ultrasonic sensors, cameras, radar, LIDAR) enable the digitalization of information for control and communication, and allow the automation of certain functions. Among them, adoptive cruise control, parking assist and fatigue recognition are becoming more common fixtures in motor vehicles.

Vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I) and vehicle-to-everything (V2X) technologies are also starting to gain some traction. We are moving closer toward a connected vehicle eco-system, where via the Internet of Things (IoT) or wireless-network connectivity technology, vehicles can communicate and share vehicle safety data with each other (V2V), with infrastructure including traffic lights/ signs and roads (V2I) and with their surrounding environments in general (V2X). Such technologies play a critical role in warning drivers of potential collisions, thereby helping to prevent road accidents. They also help in traffic management and in reducing road pollution.

Here, China is expected to lead the V2X deployment. While the U.S. and Europe continue to debate over preferred V2X technologies and data protection and privacy issues, the Chinese government has moved ahead to incorporate LTE-V2X/5G-V2X as part of its Intelligent and Connected Vehicles (ICV) strategy.5 According to the “Strategy on Developing Smart Vehicles” blueprint published in February 2020, China will roll out LTE-V2X regionally and 5G-V2X in some cities and expressways by 2025. Many V2X pilot zones have already been established.

Elsewhere, progress has been slower, but in the right direction. Importantly, global policymakers are recognizing the social and environmental benefits of autonomous vehicles. The 3rd Global Ministerial Conference on Road Safety held in Sweden, February 2020, culminated in 140 countries signing the “Stockholm Declaration,” which targets a global reduction in road traffic deaths and injuries by 50% in 2030, and calls for all vehicles sold by 2030 to include safety performance technology.

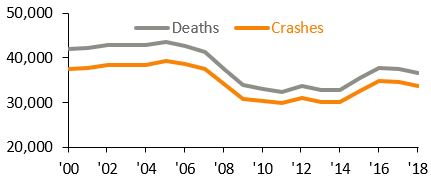

“The number of deaths on the world’s roads remains unacceptably high with 1.35 million people dying each year.” Source: WHO, 2018

Autonomous vehicles can help improve safety on the road EXHIBIT 2: NUMBER OF MOTOR VEHICLE DEATHS AND FATAL CRASHES IN THE U.S. NUMBER OF DEATHS AND FATAL CRASHES

Source: Insurance Institute for Highway Safety, J.P. Morgan Asset Management. Data reflect most recently available as of 31/1/21.

Investment implications En route toward fully automated vehicles, we are seeing exciting developments in automotive technology, with heavy investments from major automaker companies and technology giants. We expect rising consumer demand with a wider adoption of autonomous vehicles, in part spurred by policymakers. The global autonomous car market, valued at USD 19.46 billion in 2020, is projected to grow at an 18.06% compound annual growth rate (CAGR) from 2021 to 20266, and offers potentially attractive growth opportunities for automotive suppliers of sensors, controls and telematics.

The car that drives itself

Source: Shutterstock, J.P. Morgan Asset Management.

YOU MAY ALSO LIKE THIS

Sources 1J.P.Morgan Asset Management 2021 25th Annual Edition Long-Term Capital Market Assumptions. Provided for information only to illustrate market trends, not to be construed as research or investment advice. Investments involve risks, not all investments are suitable for all investors. 2In light of the rising U.S.-China tensions and recent COVID-19 experience, many regions (e.g. the European Union) and countries are now focusing on building self-sufficiency and localization, in order to prevent supply chain disruptions and protect national security. Provided for information only to illustrate market trends, not to be construed as research or investment advice. Investments involve risks, not all investments are suitable for all investors. 3Ultimately, the goal for the future is for self-driving electric cars. Autonomous driving technologies and electric vehicles are complementary, with autonomy to bring about safer, more efficient driving and battery use, while electric cars can help to significantly reduce carbon emissions (green), fuel costs and maintenance. 4Fully automated vehicles are vehicles that can perform all driving functions in all road conditions for an entire trip with no human intervention required. 55G-V2X will likely be one of the most widespread applications of 5G in China. 6Source: Mordor Intelligence.

JPMorgan Asset Management's Disclaimer

FOR EXCLUSIVE USE BY NAVIGATOR ONLY – NOT FOR FURTHER DISTRIBUTION

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy.

This communication is issued by the following entities:

In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be. In Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For all other markets in APAC, to intended recipients only.

For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2021 JPMorgan Chase & Co. All rights reserved. |

To continue to serve you better, our system will be undergoing maintenance between 10 PM to 11:59 PM on 25 Apr 2024. During this period, you will not be able to access your dollarDEX account. We apologise for any inconvenience caused.