|

Staying on top of alpha opportunities amid desynchronized recoveries and inflation fears By PineBridge Investments 8 June 2021

Halfway through the year, we see the global macroeconomic outlook to remain strong in the near term. Global manufacturing is improving, though services growth has stalled in Europe and Japan. US consumers are spending their third stimulus checks, and more re-openings over the summer should add to growth. Most of the policy stimulus and reopening benefits are likely to occur this year, with growth-rate normalization perhaps waiting until 2022. The main risk to this outlook is a more rapid and sustained increase in inflation, but that will not be ascertained until the end of the year. Therefore, the US Federal Reserve will not really know whether it can maintain its lower-for-longer forward guidance — raising chances of a more rapid and forced policy change in the fourth quarter that could trigger a more serious taper tantrum.

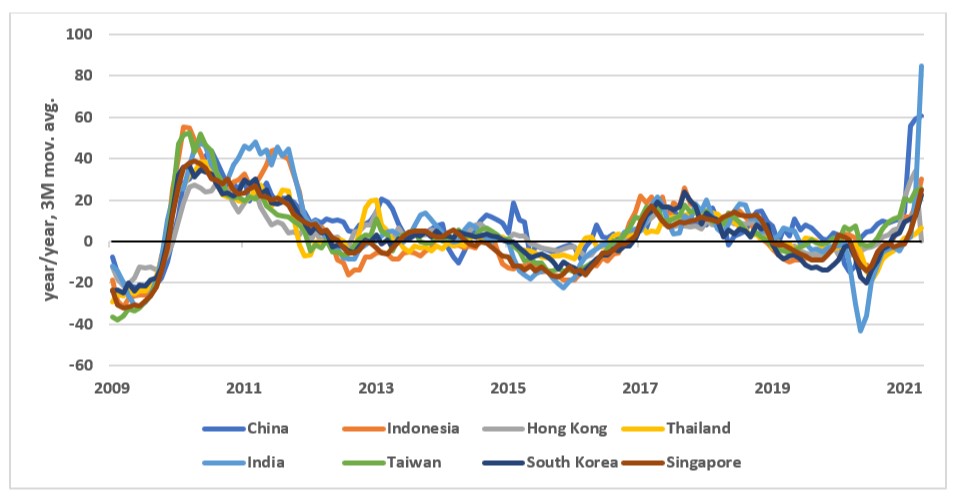

In Asia, exports are soaring. The demand for manufactured electronics has led to decade-high business optimism surveys in South Korea and Taiwan. The two export-sensitive economies have already seen a significant tech capex acceleration that has already been in place due to the US-China trade war in 2018, with a particular focus on chip production to meet the growing demand for 5G infrastructure.

Source: Macrobond, PineBridge Investments calculations as of 25 May 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

Asia weathered the Covid-19 shock in 2020 better than other major regions. China, the initial epicentre of the crisis, managed to limit the spread of the coronavirus and relied on credit growth and its industrial sector to generate a positive growth rate in 2020 – a major accomplishment while most of the world languished in recession. China also benefitted from a substantial export tailwind in the second half of 2020 as corporations and investors priced in fewer trade tensions from a Biden administration. The global work-from-home experiment coincided with a surge in electronics demand. Starting 2021, China’s economic footing has been more modest as its credit impulse has decelerated from its 2020 summer peak, and policymakers have hinted at more policy normalization. As a result, the consumer sector is expected to be a more significant contributor to economic activity, especially as China reaches two critical milestones: the 100th anniversary of the Chinese Community Party in July and the twice-a-decade Party Congress in 2022. Consumer fundamentals remain relatively strong as the labour market continues to recover and data on the household side points to income growth exceeding spending. However, households remain quite cautious, especially relative to the chart-topping retail sales numbers we’ve seen from the US. We expect China’s ambitious vaccination drive to aid that confidence recovery.

However, in emerging Asia, the spread of Covid-19 remains a significant concern, especially in India. We believe that these headwinds will be more temporary in nature rather than a structural shift. Moreover, many of these economies benefit from an overall younger demographic profile than many developed markets, so the virus may prove to be less costly and more manageable from both an economic and human perspective. Most – if not all of emerging Asia – should also benefit from the ramping up of vaccinations, so the re-opening is a matter of “when” and not “if.”

From a monetary policy perspective, we expect normalization to be a gradual process despite much more market attention paid to accelerating inflation. We believe that a Fed rate hike – a historical precursor to rate hikes from Asian central banks – is still more than a year away. While consumer prices may be accelerating in pockets of developed markets, inflation remains quite well-anchored around Asia, which may add to more caution from central banks who may choose to leave policy on the accommodative side as more evidence of a sustained recovery in Asia takes hold – a benign environment for risk assets.

Equities: Improving fundamentals

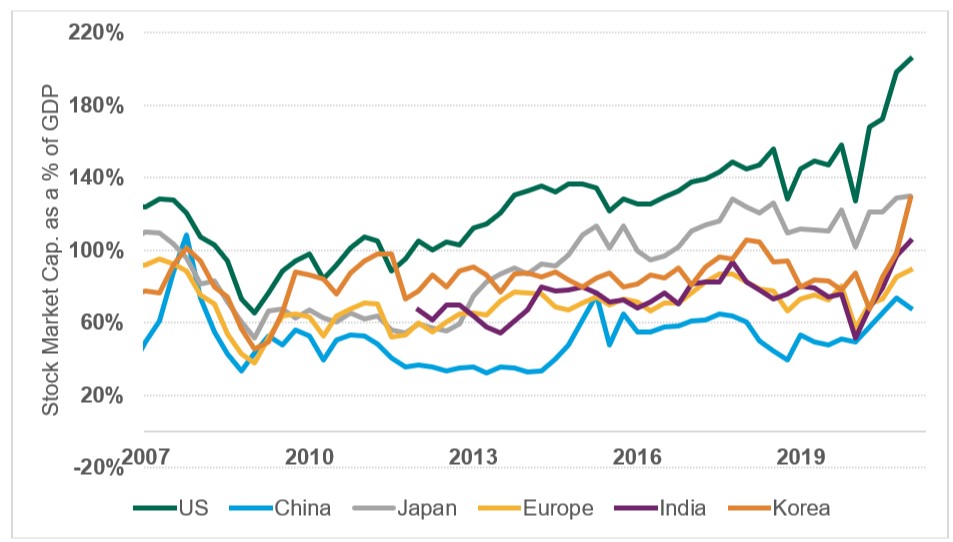

Despite much-publicized worries about inflation and premature monetary tightening, we expect unprecedented improvement in fundamentals. Across global equity markets, earnings revisions have been positive, and first-quarter results are widely expected to beat consensus. Given high expectations, near-term hiccups like Covid-related supply chain bottlenecks could drive sharp share price reactions. That said, the craziness of the past year has forced companies to get smarter and stronger, driving some to accelerate investments they believe will better position them to win. With rates near all-time lows, we believe alpha generated from finding these winners will become more important. In Asia, we expect earnings to continue to improve this year. Asian equities also appear to be far less expensive compared to the US and Japan. According to the “Buffet rule”, named after the legendary investor Warren Buffet, the stock market capitalization/GDP ratios for China, India, and Korea remain within historical norms while the same cannot be said for US equities, for example.

Valuations of Asian equities are less expensive than US and Japanese equities

Source: Macrobond, PineBridge Investments Calculations as of 7 May 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

We believe this post-Covid recovery phase will be less beta-driven and more alpha-driven as the impact of secular trends broadens out to affect more industries. This should create more opportunities for differentiated returns within sectors as the differences between relative winners and losers become more prominent.

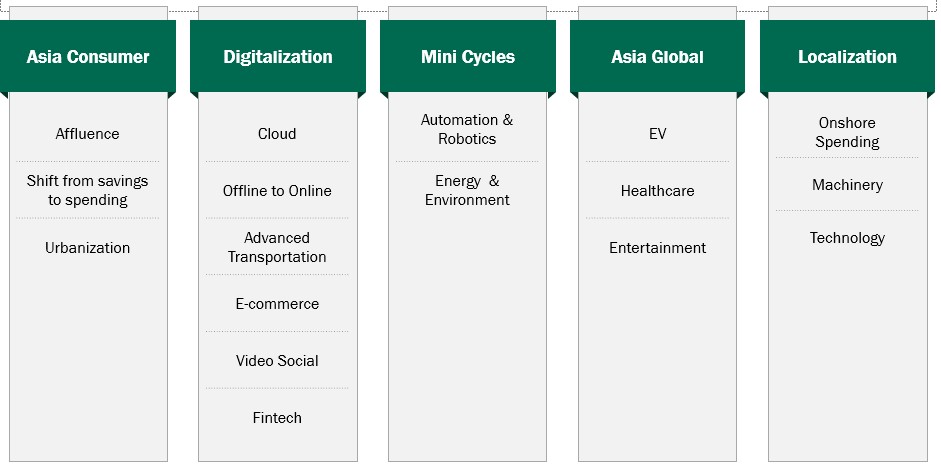

Although we can expect some headwinds in the near term, such as the continuing impact of the pandemic, Asia’s investment potential remains compelling over the long term. We believe the convergence of several powerful structural trends – including accelerating digitalization and automation, a rapid transition toward a lower-carbon economy, and an increasingly affluent and urban population – will set the stage for a seismic shift in global economic dynamics over the next 10-15 years, generating alpha opportunities.

Potential alpha drivers over the medium to long term

Source: PineBridge Investments as of 26 May 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

For example, Asia is already the world’s largest industrial robotics market: two out of three newly deployed robots in 2019 were installed in the region, with China the world’s largest market for industrial robots.1 Ageing populations and demand for complex and precision machinery are expected to shape sales of robotics systems going forward.

The opportunities around 5G technology go beyond the telecommunications industry. We believe it also offers significant opportunities for a host of other companies in the ecosystem, such as those involved in automation, media/gaming and telemedicine or tele-education, and payments infrastructure. We see global Indian IT companies benefiting from this trend, with digital becoming a significant growth component for the sector.2

Flexible approach to capturing Asian opportunities

Learn more about the Asia ex Japan Equity opportunity at https://www.pinebridge.com/en-sg/intermediary-and-individual/featured-funds/asia-ex-japan-equity.

For more investment insights, please visit http://www.pinebridge.com.sg.

YOU MAY ALSO LIKE THIS

Sources 1World Robotics Report 2020, International Federation of Robotics, PineBridge Investments as of 24 September 2020. For illustrative purposes only. We are not soliciting or recommending any action based on this material. 2Source: NASSCOM, “Future of Technology Services,” as of February 2021. 3See “The Future of Asia: Asian Flows and Networks are Defining the Next Phase of Globalization,” McKinsey, 18 September 2019. https://www.mckinsey.com/featured-insights/asia-pacific/the-future-of-asia-asian-flows-and-networks-are-defining-the-next-phase-of-globalization#:~:text=On%20consumption%2C%20in%202000%20Asia,39%20percent%20of%20global%20consumption; See “The Future of Asian and Pacific Cities,” United Nations Economic and Social Commission for Asia Pacific, 2019. https://www.unescap.org/sites/default/d8files/knowledge-products/Future%20of%20AP%20Cities%20Report%202019.pdf

PineBridge Investments' Disclaimer All investments involve risk, including the loss of principal amount invested. Past performance is not indicative of future results. The information presented herein is for illustrative purposes only and should not be considered reflective of any particular security, strategy, or investment product. It represents a general assessment of the markets at a specific time and is not a guarantee of future performance results or market movement. This material does not constitute investment, financial, legal, tax, or other advice; investment research or a product of any research department; an offer to sell, or the solicitation of an offer to purchase any security or interest in a fund; or a recommendation for any investment product or strategy. You are solely responsible for deciding whether any investment product or strategy is appropriate for you based upon your investment goals, financial situation and tolerance for risk. You should also read the prospectus of the investment product for further details, including the risk factors before investing. Any views express represent the opinion of the manager and are subject to change. Views may be based on third-party data that has not been independently verified. PineBridge Investments does not approve of or endorse any re-publication or sharing of this material. We are not soliciting or recommending any action based on this material. In Singapore, this document is issued by PineBridge Investments Singapore Limited (Company Reg. No. 199602054E), licensed and regulated by the Monetary Authority of Singapore (MAS). This advertisement or publication has not been reviewed by the MAS. Investors should note that the website www.pinebridge.com.sg and any other website (including any contents therein) referred to in this document have not been reviewed or endorsed by the MAS. |