Quality, resilient Singapore stocks to shine despite a challenging milieu

20 Aug 2019

Summary

In our view, the macro backdrop for Singapore is likely to be challenging in the near term with possible economic downgrades and slower corporate earnings growth. Yet, our bottom–up view on stock selection remains constructive. We continue to be positive on innovative 'New Singapore' stocks, selected industrial counters and quality dividend stocks, all of which should offer resilience in an environment of slower economic growth

Weighing the Positives and Negatives

Being finicky has its merits especially when it comes to stock selection in Singapore, which is facing a challenging macroeconomic backdrop. Without doubts, fears of a steep slowdown in the global economy and the possibility of a flare–up in the unresolved US–China trade feud will likely dominate as key investor concerns in the coming quarters. And we expect these uncertainties to translate into slower economic and corporate earnings growth in Singapore for the rest of 2019.

While we are cautious on the rising macro headwinds, our bottom–up views on stock selection continue to be constructive. We see good opportunities in stocks with quality value, sustainable growth and strong structural ideas, especially those that are reinventing their business models. We are also positive on Singapore dividend stocks, whose dividends are supported by healthy and structural earnings growth. In short, our focus will be on delivering stock selection returns by picking quality companies, which are resilient amid an increasingly volatile but slower growth environment.

On a more positive note, after a fleeting market downturn in May 2019, global risk appetite has started to improve of late after the Fed signalled its intention to cut rates to prevent the US–China trade war from stalling economic growth. The increasingly dovish tilt of major central banks as well as the resumption of US–China trade talks in late June had also lifted market sentiment at the end of 2Q 2019.

Moreover, equity markets have already begun to price in growth concerns and earnings risks. At the same time, valuations of Singapore equities are looking inexpensive relative to their historical averages, with price–to–book multiples still nearing the trough levels that were last seen in 2011 and 2015. All things considered, we believe these positive and negative factors are setting up an interesting backdrop for Singapore equities, which will continue to be a good hunting ground for the discerning, active and bottom–up stock pickers.

Bleak Economic Outlook for Singapore

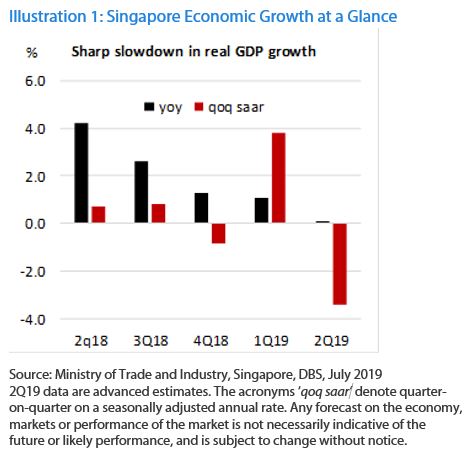

The Singapore economy saw 1.2% growth year–on–year (YoY) in 1Q 2019, the lowest growth rate in close to 10 years. And recent flash estimates by the Singapore Ministry of Trade and Industry (MTI) pinpointed to an even slower YoY growth of 0.1% (or –3.4% on a quarter–on–quarter basis) in 2Q 2019. A technical recession—defined as two consecutive quarters of negative economic growth—occurring in Singapore in 2H 2019 is now a real possibility, especially with the worsening of global trade of late.

Notably, contraction in manufacturing sector growth is the main driver of the slowdown. But other segments of the Singapore economy, such as wholesale and retail sales, are also not performing well. It is likely that MTI will again lower its full-year economic growth forecast for Singapore. In May 2019, it downgraded Singapore's 2019 GDP growth to 1.5–2.5% from an earlier range of 1.5–3.5%.

To be sure, the macro risks are beginning to bite for the open and trade–dependent economy of Singapore and we now think that Singapore's GDP growth for 2019 will come in at around 1%. Nonetheless, we continue to see no serious excesses in the global economy, where growth remains supported by the dovish stance of the Fed and other major central banks, as well as targeted support measures by the Chinese government.

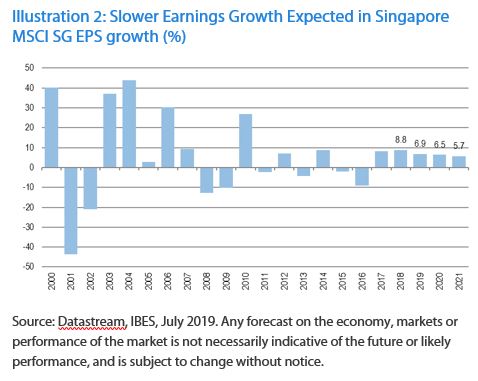

In Singapore, weak economic growth often translate into deteriorating earnings for companies, and earnings downgrades in the city–state could be on the rise. Against this backdrop, it is likely that earnings expectations will continue to be cut, with downside risk to our current expectation of 3–5% growth. Still, earnings growth trajectory in Singapore is increasingly bifurcated and dispersed. In 2019, we have witnessed much wider sector and company dispersion in terms of earnings growth. This tends to bode well for us as bottom–up stock selectors.

Sanguine on 'New Singapore' Stocks and Industrials

Beyond the economic doom and gloom, Singapore stocks that offer sustainable earnings growth and decent dividends, which are backed by strong free cash flows, will continue to shine in our view. In an environment where economic growth and corporate earnings are deteriorating, resilient stocks with structural growth drivers will remain highly sought–after by investors.

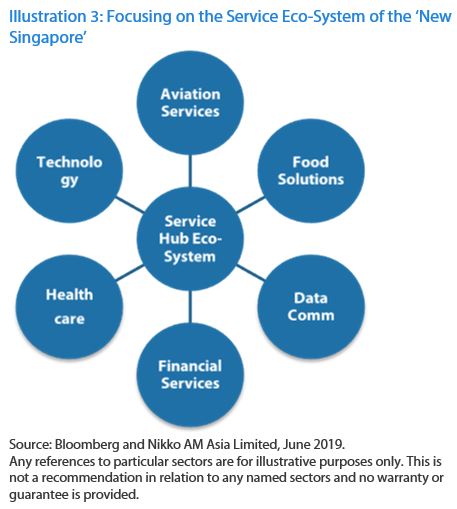

One group of equities that we are positive on are the “New Singapore” stocks, which represent the future economy of Singapore, embodying innovation, integration and sustainability. These are companies that are reinventing or reorganising their business models to succeed and be more relevant in the future economic landscape. In particular, we like corporate restructuring candidates. In our view, corporate restructuring will continue to be one of the key drivers of Singapore equity returns as locally–listed companies look to exploit inorganic growth opportunities. 'New Singapore' companies tend to be in sectors such as technology, data centres, healthcare, logistics, tourism and consumer services, most of which focus on the service eco–system (see Illustration 3 for examples).

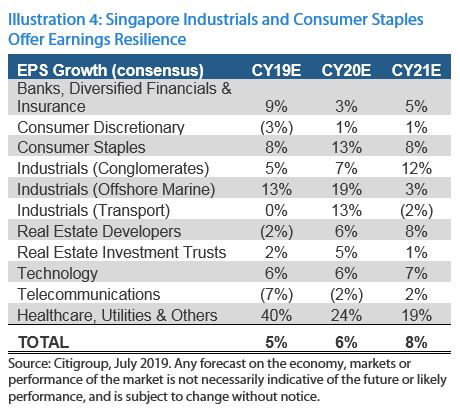

Elsewhere, we continue to favour industrials and consumer staples sectors. Industrials are offering a combination of good value, earnings resilience (see Illustration 4) and decent growth, all of which should provide some upside as US–China trade tensions ease. In addition, industrials are typically beneficiaries in the latter part of the economic cycle where capital expenditure begins to accelerate. Likewise, defensive consumer staples, whose revenues are linked to basic needs and are less economically sensitive, tend to offer resilience in an environment of slower economic growth.

The Dividend Advantage

Lastly, we remain convinced about the long–term merits of investing in Singapore dividend stocks, especially those with dividends that are supported by healthy and structural earnings growth. In the current low interest–rate environment, where decent yields are hard to come by, stocks that pay an attractive and predictable dividend yield will continue to be in strong demand with yield–hungry investors.

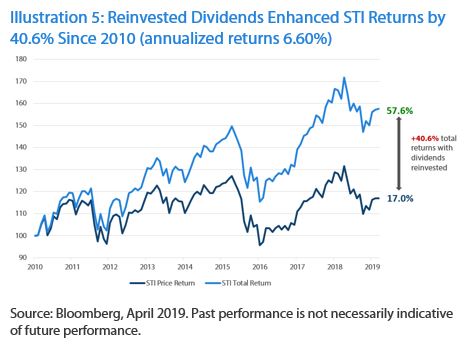

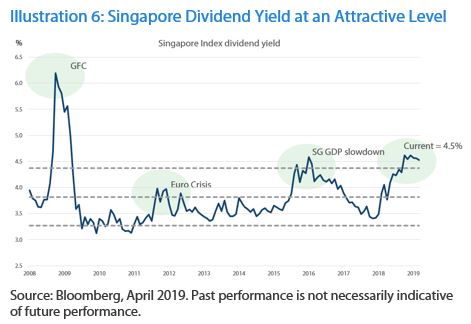

Dividend expectations for Singapore corporates continue to remain much more resilient than earnings estimates. That's a testament to the quality of their underlying earnings, cash flows and balance sheets. Forward dividend yields of Singapore stocks also remain one of the most attractive in the Asian region, highlighting the importance of dividends as part of the total return equation for investing in locally–listed stocks. Since 2010, reinvested dividends had offered additional alpha and enhanced the returns for the STI by more than 40% as shown in Illustration 5 (annualised returns of the STI over 10 years up to April 2019 is 6.60%).

In general, we invest in two groups of dividend stocks, namely dividend anchors and dividend growers. In short, dividend anchors are companies with low gearing, strong cashflow streams, consistent profitability and a strong track record of dividend payouts. Whereas dividend growers are those with decent earnings growth, free cash flow growth and exhibit an increasing payout ratio.

To conclude, despite the challenging macro backdrop for Singapore, exacerbated by a slowing global economy and the yet–to–be–resolved US–China trade feud, we continue to find ample opportunities in Singapore to deliver decent gains and generate alpha with judicious stock selections.

Important Information

This document is for information only with no consideration given to the specific investment objective, financial situation and particular needs of any specific person. Any securities mentioned herein are for illustration purposes only and should not be construed as a recommendation for investment. You should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you. Investments in unit trusts or ETFs are not deposits in, obligations of, or guaranteed or insured by Nikko Asset Management Asia Limited (“Nikko AM Asia”). Past performance or any prediction, projection or forecast is not indicative of future performance.

The information contained herein may not be copied, reproduced or redistributed without the express consent of Nikko AM Asia. While reasonable care has been taken to ensure the accuracy of the information as at the date of publication, Nikko AM Asia does not give any warranty or representation, either express or implied, and expressly disclaims liability for any errors or omissions. Information may be subject to change without notice. Nikko AM Asia accepts no liability for any loss, indirect or consequential damages, arising from any use of or reliance on this document. This publication has not been reviewed by the Monetary Authority of Singapore.

Nikko Asset Management Asia Limited. Registration Number 198202562H

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 20/08/2019.