2019 investment outlook: Opportunities amidst Challenges

In stark contrast to the stellar performance of equity markets back in 2017, 2018 proved to be the year where volatility is back. On one hand, Central Banks globally are reversing years of monetary easing after peak liquidity in 2016-2017. While on the other, geopolitical tensions ranging from Brexit to Sino-US trade disputes rocked financial markets.

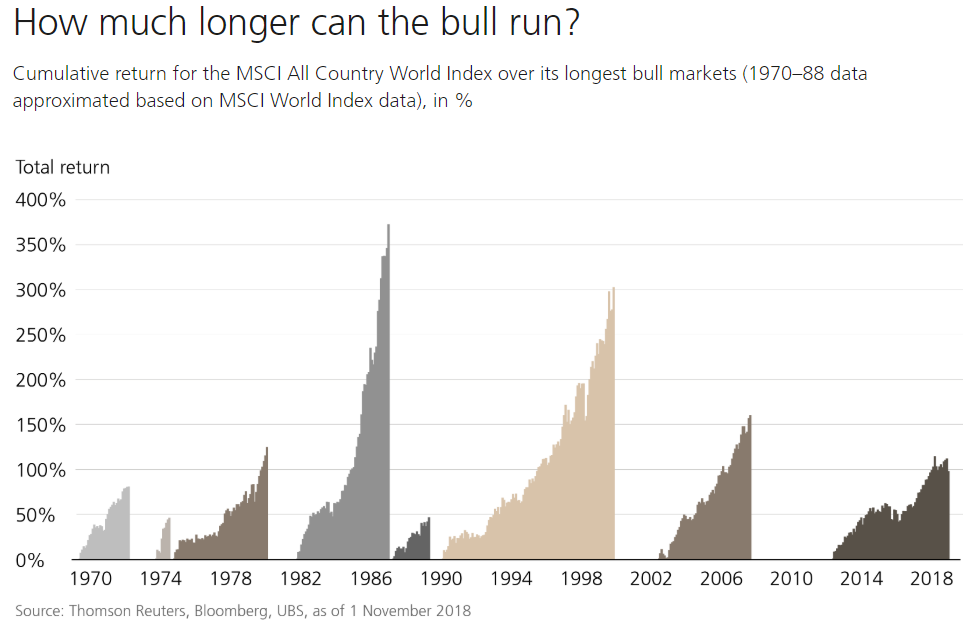

With the current bull market at its 10th year, how much longer can it run?

Figure 1

We expect 2019 to be very much similar to 2018 with spikes in volatility as we approach closer to the end of the cycle. Unresolved issues between US and China as they compete for global supremacy and the anxiety over the Brexit deadline in March will continue to dominate headlines at least in the first half of 2019. The pace and extent of the tightening by Central Banks across the world including US Federal Reserve, European Central Bank, Bank of England, Bank of Canada and the Reserve Bank of Australia will also continue to weigh on markets.2

In the US, economic strength as well as earnings momentum may provide short-term outperformance despite the prospects of 2-3 rate hikes from the Federal Reserve (Although the Fed did hint of a potential pause in the rate hike3). In addition, while President Donald Trump’s Republican Party lost control of the House in the recent US midterm elections, he still has discretion over tariffs and his ambitions for re-election in 2020 may result in accelerated deals with EU and China.

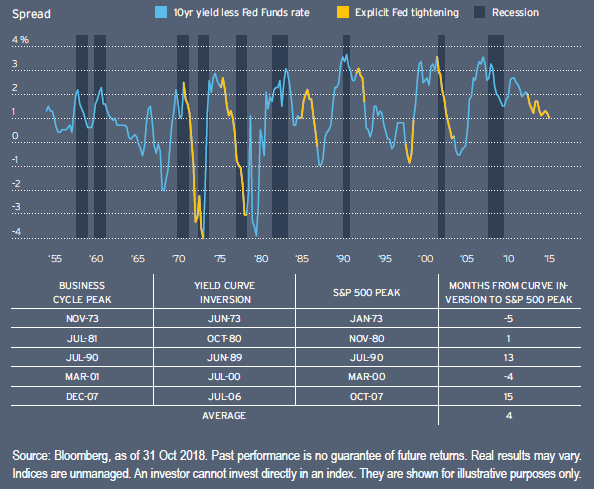

Yield curve inversion = Recession

There have been much attention and concern about the relationship between the inversion of the US yield curve and a US recession, with the inversion of the US Yield Curve as a leading indicator of a recession.

As figure 2 shows4, an inverted US yield curve has preceded every US downturn for the past half century. While there have been a couple of false or early warnings, no contraction cycle have occurred without this signal being triggered. On average, US contractions typically begin twelve months after long yields have fallen below the Fed’s policy rate. US equities, another leading indicator with a shorter lead-time, have peaked at about four months after yield curve inversions.4

Figure 2

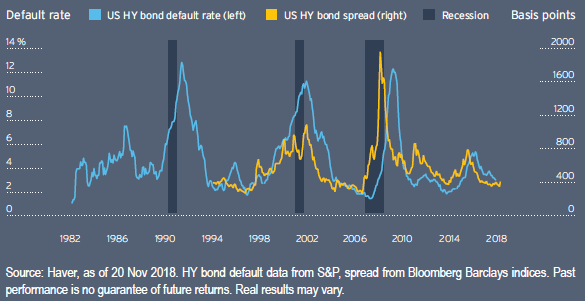

However, we noticed that the past tendency of credit markets and equities have been much more coincident indicators of economic downturns than the yield curve. (as shown4 in Figure 3)

Figure 3

Despite widespread attention and concern, the US yield curve has yet to invert, hence there are reasons to believe that while we are at the late stage of the bull market, the probability for a recession in 2019 will not be likely.

Opportunities to consider in 2019 amidst the challenges

-

1. Tighter Monetary Policy

Given the expectation of interest rates hike across major central banks in 2019, investors could consider investing in floating rate instruments where the yield increases as interest rates rise. If you are interested in such an approach, it is worth considering Floating Rate Funds. Fixed Income investors could also consider Short Duration Bond Funds where correlation to interest rate risks are lower than longer duration bond funds.

-

2. Slower Growth

While global growth is expected to be slow in 2019, there lies opportunities within US Financials and Global Energy stocks. The rising rate environment provides tailwind for US Financials due to the increase in net interest margins, and with oil prices on a steady recovery from its 2016 lows, it is definitely a sector worth a second look.

-

3. Geopolitical Risk

Geopolitical uncertainty could come in many shapes and forms, and sometimes in the most unexpected places. One way for investors to navigate the uncertain climate is to consider rebalancing your asset allocation and diversify with Multi-Asset Income funds with a focus on defensive sectors.

-

4. Emerging Market or Emerging Value?

Following the sell-off in China and Emerging Market (EM) in 2018, equity valuations have become much more attractive. While the earnings-per-share estimates continue to trend downwards for 2019 and will need to stabilize before investors are likely to re-enter emerging markets, specific EM opportunities could emerge in the later part of the year. Investors could consider increasing their long-term EM allocation by buying the dips. In particular, if US and China can reach an agreement, the uncertainty over global equity markets would lift and Chinese equities might be one of the biggest winners.

Start searching for these funds using our intuitive filters on Fund Finder to see which funds suit you.

So there you have it, these are the highlights for what to expect in the New Year. In your quest for higher returns, remember that now is not the time for market timing. Often times, the most “boring” move could be the smartest move. Get started, stay invested, and top up your portfolio over time.

Footnotes

Sources:

1UBS: https://www.ubs.com/global/en/wealth-management/chief-investment-office/our-research/year-ahead.html?campID=SEM-CIOYEAH2019-SG-ENG-GOOGLE-YEARAHEAD2019-ANY-ANY-ANY-ANY

2State Street Global Advisors: https://www.ssga.com/publications/global-market-outlook/2019/gmo-2019-full-magazine.pdf

3Bloomberg: https://www.bloomberg.com/news/articles/2018-11-21/fed-seen-primed-for-2019-pause-as-growth-market-headwinds-swirl

4Citibank: https://www.privatebank.citibank.com/ivc/docs/Outlook_2019.pdf

YOU MAY ALSO LIKE

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 15/01/2019.