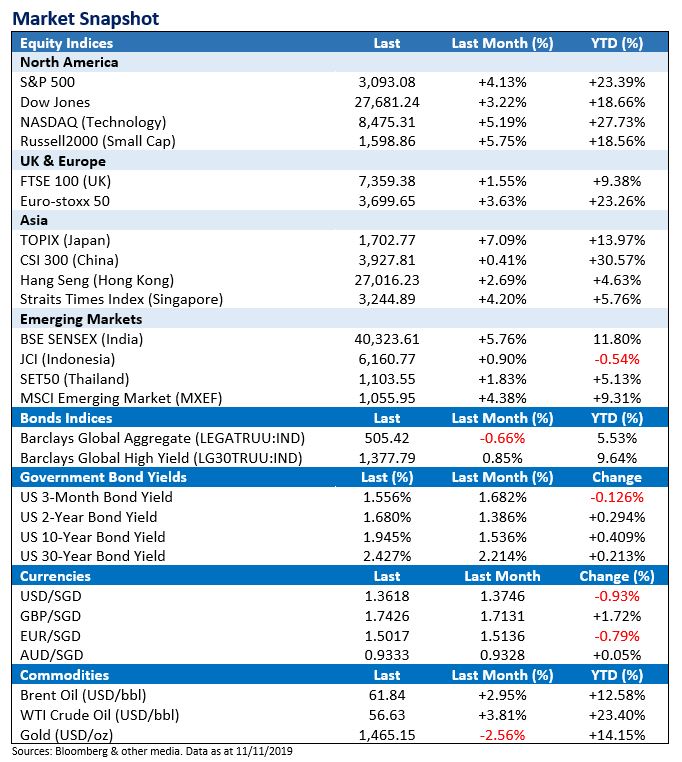

Latest Market Update

The month of October concluded with the US Federal Reserve cutting interest rates for the third time this year – lowering its benchmark funds rate by 25 basis points to a range of 1.5% to 1.75% in a widely expected move.1

With a slew of positive news and investor sentiments at an all–time–high, has the Santa Claus rally already started, and is there more room for growth in the following weeks?

Progress in trade war

As the trade war progress into its 18th–month, there seemed to be some respite from both US and China, with President Donald Trump first announcing last month that the two major powers had reached a “phase one” agreement on trade, though that pact has yet to be finalized, as well as discussions on rolling back tariffs even before a “phase one” trade deal is signed.2

Just last month, China pledged to buy as much as US$50 billion worth of US agricultural products and open up its financial markets further to foreign investors.3

U.S GDP grew faster than expected

Another positive catalyst to the world's largest economy is the latest US GDP numbers for Q3, which grew faster than expected at 1.9% but slowed slightly from the 2% pace in the second quarter. While the better–than–expected data was the result of continued consumer spending as well as government expenditures, business investment continued to decline amidst trade uncertainty and fears of a manufacturing slowdown.4

Earnings beat expectation

The recent corporate earnings announcement by companies in the S&P500 index was also much stronger than expected, with names like Netflix, Johnson & Johnson, and banking giants such as JPMorgan Chase, Bank of America and Morgan Stanley beating analysts' estimates.5

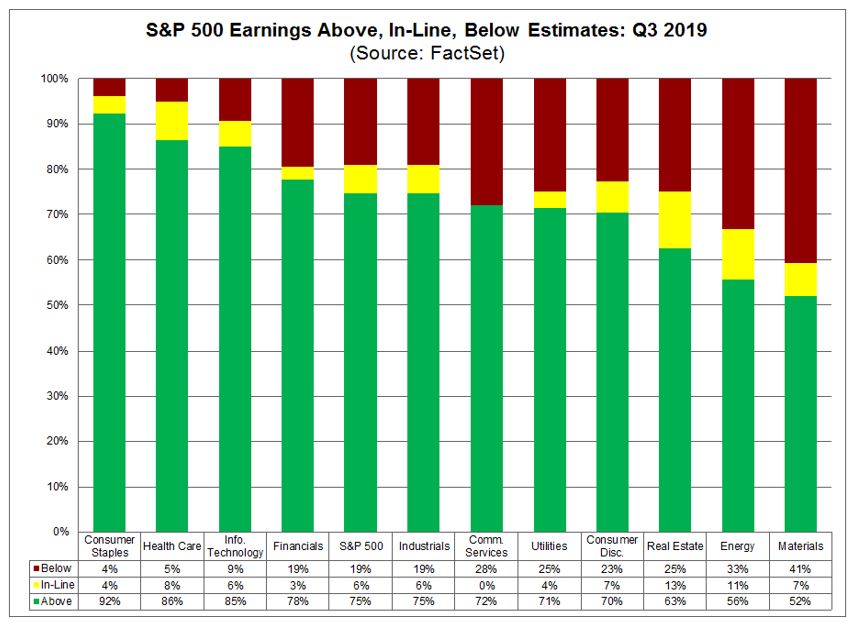

As of November 8th, 89% of the companies in the S&P500 have reported actual results for Q3 2019 and 75% of them reported actual Earnings Per Share above estimates, with Consumer Staples, Healthcare, Information Technology & Financials leading the outperformance.6

S&P 500 Earnings Above, In Line, Below Estimates: Q3 2019 (Source: FactSet)6

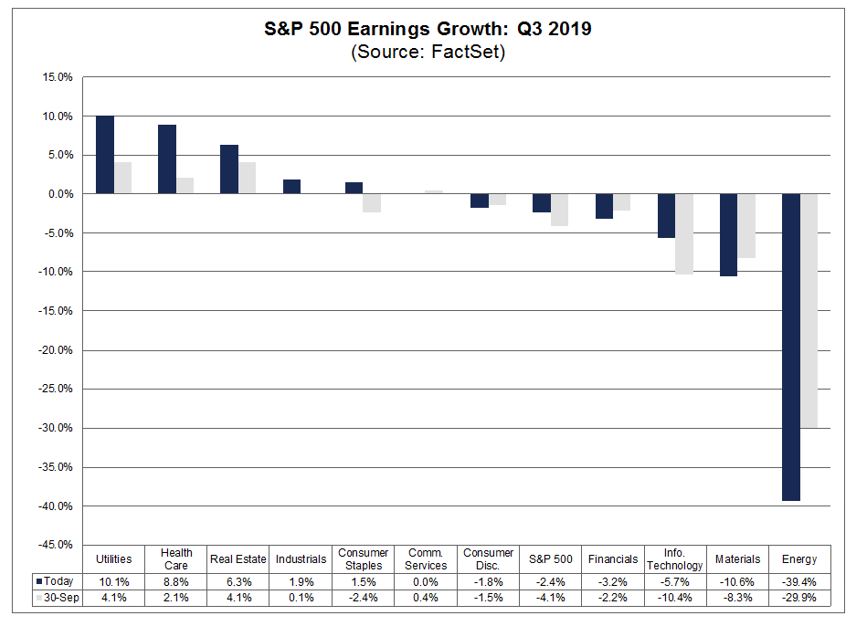

On y–o–y earnings growth, it has been led by Utilities and Healthcare followed by Real Estate, Industrials and Consumer Staples, while Materials, Energy and IT experienced the largest y–o–y decline in earnings.6

S&P 500 Earnings Growth: Q3 2019 (Source: FactSet)6

Recession alarm switches off

Just few months ago, fears of a global economic recession sounded its alarm with the inversion of the Treasury Yield Curve (where the short duration yields were higher than the rates on the long end). Today, that has changed, and the bond market is actually signaling growth after the Fed cut rates three times this year.7

Did Santa Claus rally come early?

Those of you who do not know what is a Santa Claus rally, it is a sustained increase in the stock market that occur in the last week of December through the first two trading days in January.8

Since 1998, when the S&P500 is up by more than 9.5% through the end of first week of November, the market has seen a 4% further pop on average, and this has happened 10 out of 10 times in the past 20 years, according to Fundstrat.9

With the S&P500 up more than 23% this year and 4.1% since last month, perhaps the Santa Claus rally is already here. So do you still think there will still be a recession in the near term?

Whether there is a recession or not, staying invested for the long term can help you ride the waves of volatility, so start exploring funds and grow your wealth with no fees on dollarDEX by using our intuitive fund finder now!

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 19/11/2019.

-

1 https://www.cnbc.com/2019/10/30/fed-decision-interest-rates-cut.html

2 https://edition.cnn.com/2019/11/07/investing/asian-market-latest/index.html

4 https://www.cnbc.com/2019/10/30/us-gdp-q3-2019-first-reading.html

6 https://insight.factset.com/sp-500-earnings-season-update-november-8-2019