|

Mid-Year Review 2021: Invest with inflation on your radar 6 July 2021

As we cross the midpoint of 2021, it’s time to take stock of the markets so far this year and look at where the market forces may lead us from here.

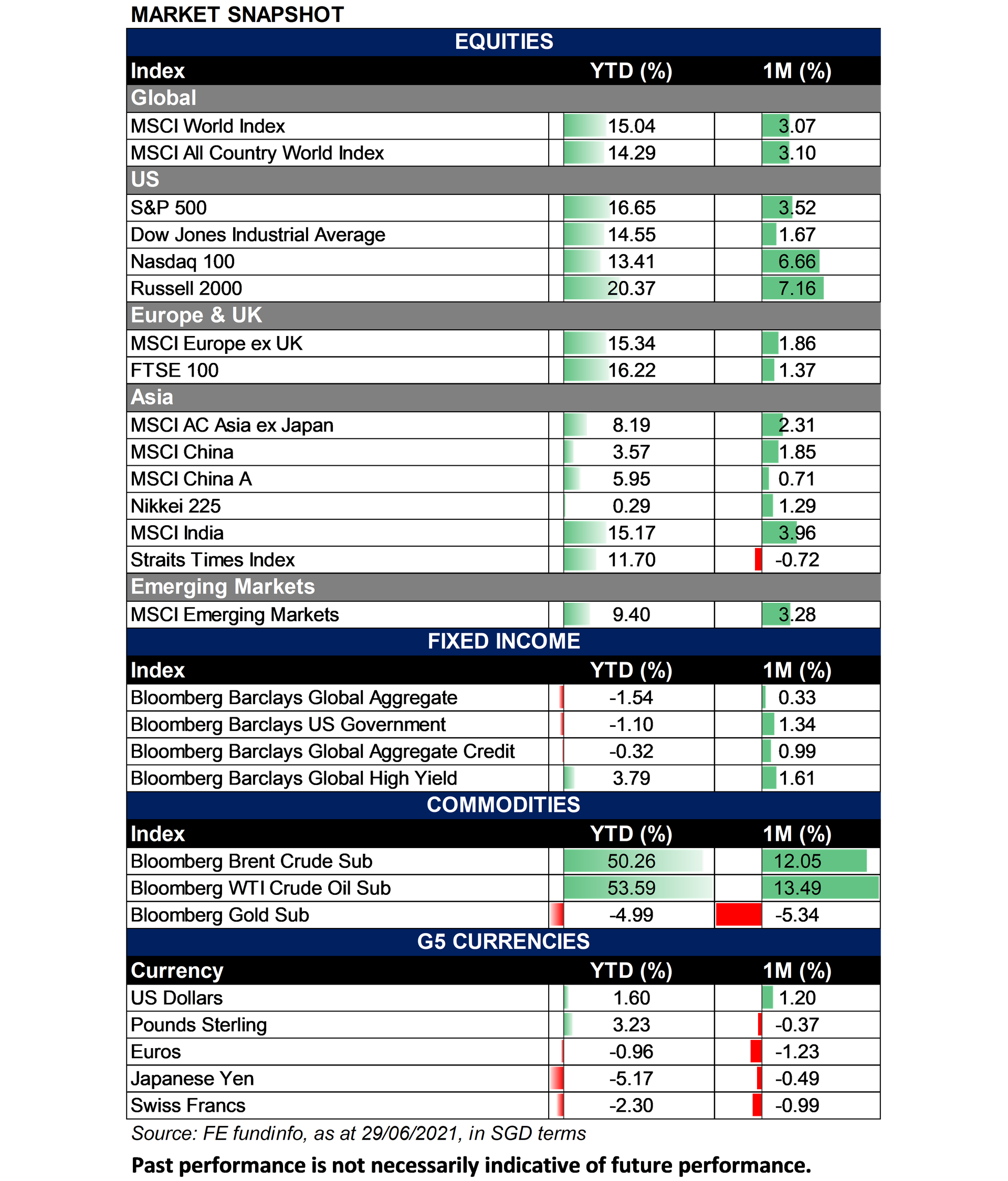

Revisiting H1 2021 Geographically, stock markets are higher in most places. 2021 saw a broad rotation from growth sectors like tech to value sectors like banks and energy plays, making the S&P 500 a better bet than the technology- and growth-heavy Nasdaq so far into the year.1 Growth stocks, however, have been doing well of late, pushing US indices S&P 500 and Nasdaq to new highs.2

Within bond markets, bond investors have been buying US government bonds in recent weeks, driving down yields and pushing the widely-watched 10Y US Treasury yield below 1.5%.3

On alternative investments, real estate and commodities have charged higher as investors seek protection from rising inflation. Fears are rising over the property market running too hot, as US home prices notched their biggest jump since December 2005 in March.4

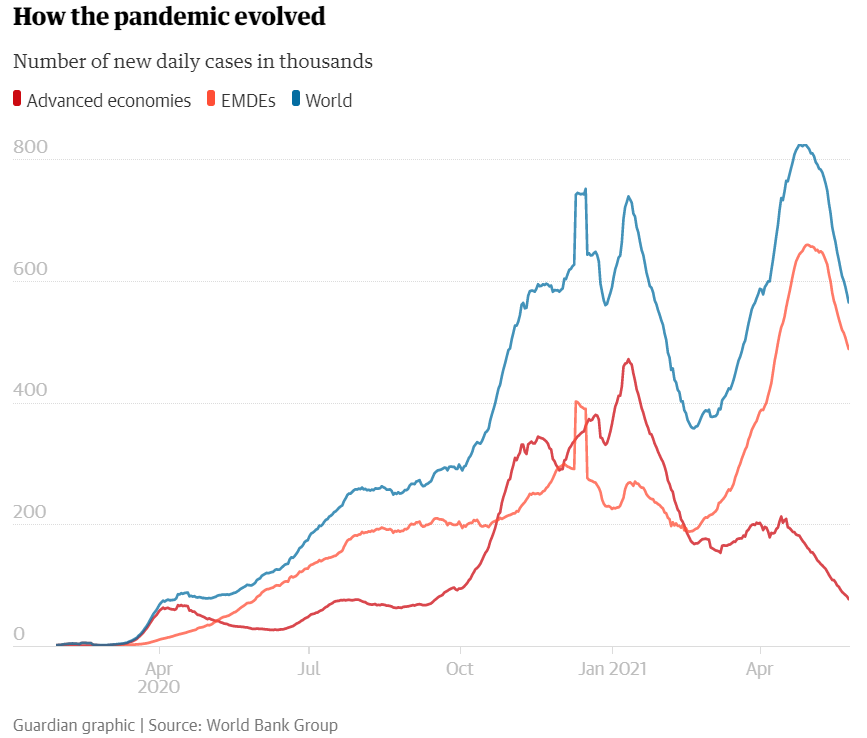

An uneven recovery With many countries now having started widespread vaccine rollouts, the number of daily cases is stable or falling in most regions.5

Countries that have been quick to vaccinate their population against COVID-19 and that are managing to control infections through effective public health strategies are seeing their economies recover more quickly. The uneven recovery is also driven by varying levels of government support to vulnerable workers and businesses, a country’s dependency on particular sectors, as well as public health and vaccination policies.6

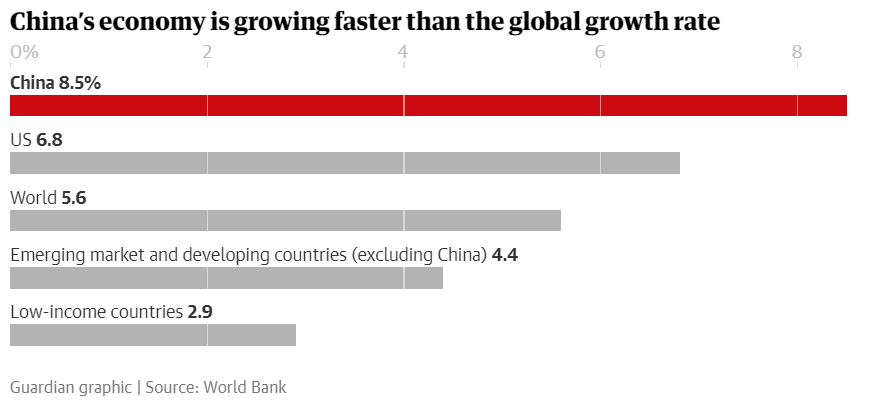

China China is expected to grow by 8.5%, higher than the 6% expected in emerging and developing markets. Excluding China, developing markets are expected to grow by a more modest 4.4%, held back by slower progress with the Covid-19 vaccine and a resurgence in infection rates.7

Consumer inflation has remained tame in China despite recent surge in factory prices. The country’s higher-yielding bond markets also remain attractive to global investors, which may help keep the yuan stronger against its peers. Chinese 10-year sovereign bonds still yield around 1.6% more than Treasuries of the same tenor. The inclusion of some government debt into FTSE Russell’s flagship global debt index will also help support inflows.8

The People’s Bank of China (PBOC) has already started curbing credit growth to tackle debt risks, although in a gradual manner to avoid stalling its economic recovery. In June, the PBOC also increased its injection of short-term cash for the first time since March, a marked shift in its approach in managing liquidity after months of providing the minimum to meet market demand.8

Read more: Investing into China: The Growing Giant

United States The US economy is expected to grow by 6.8% this year, reflecting massive government support and the relaxation of pandemic restrictions amidst an effective inoculation program.6 Investors are also following Biden’s infrastructure bill, that could deliver a fresh jolt to business activity in the US, while improving roads, bridges and tunnels.9

US investors will in the coming weeks find themselves in the backdrop of what is setting up to be another strong round of quarterly corporate earnings results. According to FactSet data, 66 of 103 S&P 500 companies that have issued earnings per share guidance for the second quarter so far, are projecting a positive outlook that exceeds consensus estimates.2

Also: Is the US worth investing into right now?

Europe Analysts at Morgan Stanley believe Europe is well-placed to outperform all major regions this year, due to attractive valuations, stronger earnings-per-share growth and the launch of the EU’s massive post-COVID recovery fund. Goldman Sachs and JPMorgan’s analysts have also separately identified “inexpensive” and “cheap” stocks within Europe.10

After initial setbacks, the pace of Europe's vaccination campaign has picked up and infection rates in many member countries have been falling.11 However, one dissenting investor thinks that European markets lack the disruptors and exciting industries seen in Asia and America.10

The big question is when the Fed will start tapering its stimulus.

Inflation remains a big risk and on investors’ radar, so do expect to hear more and more about inflation in coming months as investors hawk on every fresh data point. So far, Federal Reserve Chair Jerome Powell have said repeatedly he believes inflationary pressures this year will be "transitory", largely reflecting base effects as this year's data lap last year's pandemic-depressed levels.12

Investors have been fixated on whether the Fed will start tapering its asset purchases earlier than planned in response to runaway inflation, and comments from several Fed officials are increasingly pointing the commencement of tapering to the start of 2022 and for Fed rate hikes to begin at the end of 2022.9 If inflation does gets out of hand, however, central banks may have to reverse stance, and that would certainly ripple through the valuations of risky assets.

The Bank of England (BoE) has similarly kept its monetary policy unchanged but will be monitoring its inflation data as the UK economy recovers. The stance would buy the bank some time to see the full impact of ending furlough programs and structural unemployment that may emerge, as well as to observe if inflation proves to be transitory or persistent.13

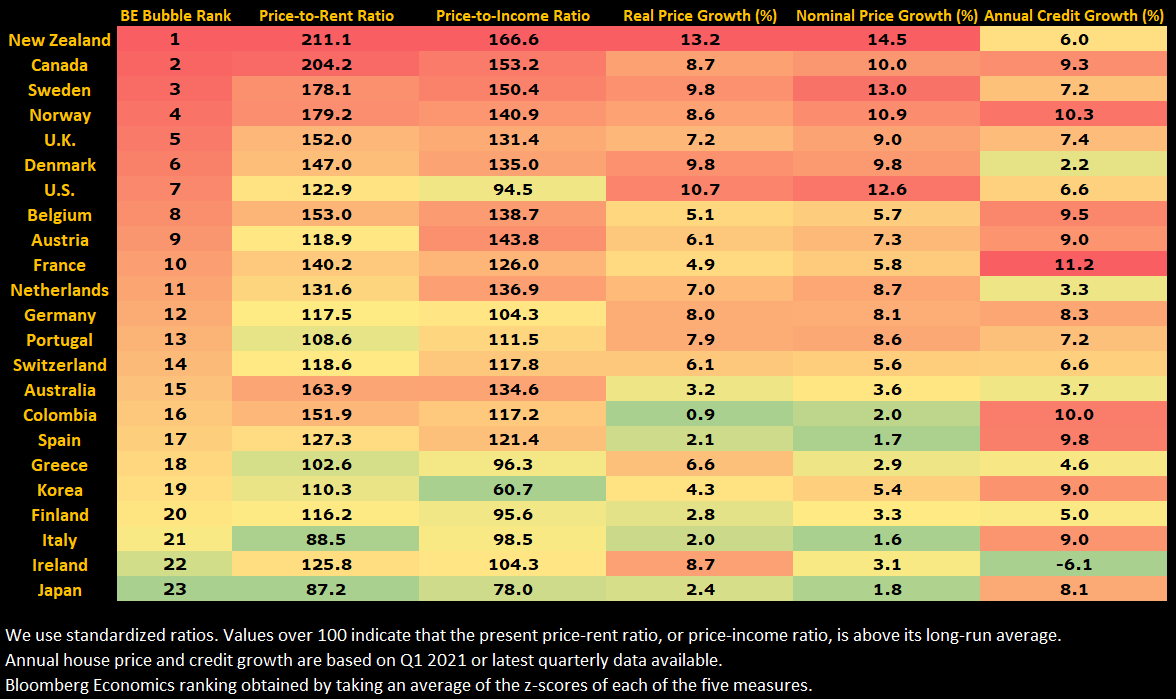

Heeding the simmering property sector Real estate price ratios for many countries are higher than they were ahead of the 2008 financial crisis, according to the Bloomberg Economics analysis.14

Source: Bloomberg Economics

Economist Niraj Shah of Bloomberg Economics opines that record low interest rates, unparalleled fiscal stimulus, lockdown savings ready to be used as deposits, limited housing stock, and expectations of a robust global economic recovery are all supercharging home prices.14

Keeping up With the US still 7.6 million jobs shy of pre-pandemic levels15, a withdrawal of economic support in the immediate horizon does not seem too likely. Inflation data and labour market reports will therefore likely be key for the rest of 2021, as investors look for indications to the health of the US economy and how far central banks can keep supporting the economy with accommodative policies.

Investors may also wish to keep tab on increased wages and bond yields to stay ahead of inflation data and central bank decisions. The former leaves more cash on consumers’ hands that could possibly push prices higher, while the latter could rise if and/or when investors sell bonds in anticipation of higher interest rates.

Concerned about inflation? We outline 3 easy ways to inflation-proof your investment portfolio to help you stay ahead.

2021 has been a roller coaster ride for economies and markets around the world, battling a pandemic that proves difficult to control even with highly effective vaccines and successful inoculation campaigns. With half the year gone and half more to go, use the chance to review your investment portfolio and make the necessary adjustments to achieve your investment goals. Login to your dollarDEX account to assess your investment portfolio now, or create a free account if you do not have one!

Want free investment insights to your inbox? Sign up now!

YOU MAY ALSO LIKE THIS

Sources 1 https://www.investors.com/news/stock-market-forecast-next-six-months-poses-new-risks-for-investors/ |