|

Manulife Investment Management’s Asia-Pacific REITs Fund: A unique income solution for investors By Manulife Investment Management 6 July 2021

Asia-Pacific real estate investment trusts (AP-REITs) have become increasingly popular with investors, and deservedly so.

First, they offer a unique, diversified opportunity set across real estate segments: from established Grade A office space located across the region’s bustling cities to cutting-edge logistical facilities and the growing number of data centres that power cloud applications.

In addition, AP-REITs provide a unique hybrid product structure that appeals to different investors, particularly those seeking steady, long-term income. By “hybrid product structure”, we mean that REITs possess equity and bond characteristics: investors can participate in the potential upside of price appreciation (similar to equities), while also receiving income from regular dividend payouts (similar to the coupon payments from bonds).

This article examines the investment case for AP-REITs, including the opportunities on offer and how they are affected by different market environments. Finally, we will look at how Manulife Investment Management’s unique active-management approach to the asset class allows investors to capture the most it has to offer.

AP-REITS: A diversity of opportunity for investors

Although the first AP-REIT (ex-Japan) was listed in Australia in 1971, the concept is still relatively new to the region. Singapore has since emerged as the leading REITs hub, while lesser-developed markets in Southeast Asia have gained notable momentum over the past five years.

The relative novelty of the asset class, coupled with a diverse range of opportunities, is proving particularly attractive to investors. Indeed, the asset class’s rapidly expanding universe gives investors exposure not only to real estate in more developed economies (Australia and Singapore) but also emerging economies (India and Philippines, with the latter launching its first REIT in 20201). Indonesia is also currently working on changes to REIT laws that should allow for REIT listings. The diversity extends to different segments that include established and newer industries. Office and retail REITs represent traditional real estate plays in most markets. Meanwhile, industrial REITs (incorporating data centres and logistics) reflect exciting innovations in the asset class.

AP-REITs performance in different market environments: The impact of interest rates and inflation

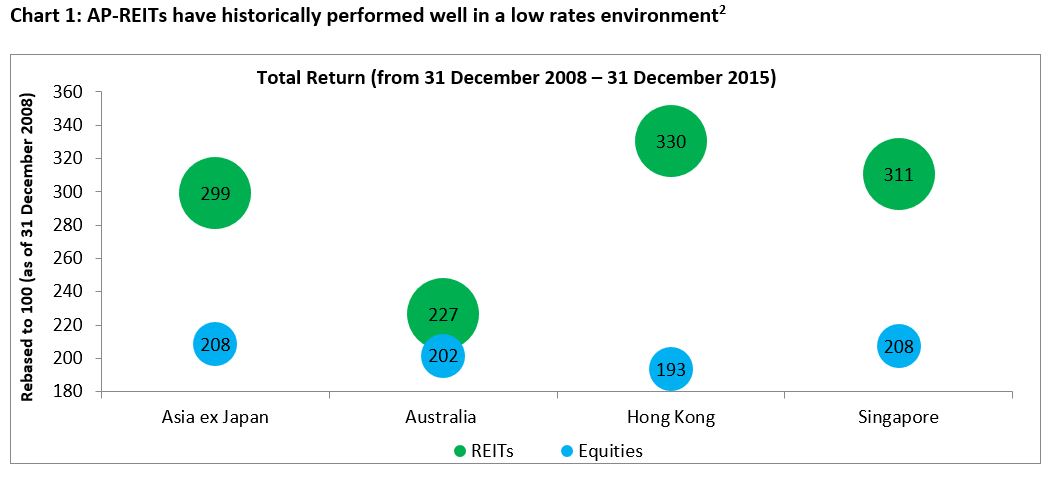

Of relevant market factors, interest rates have historically played a significant role in how investors position themselves in the asset class. Indeed, as Chart 1 shows, AP-REITs outperformed equities on a regional and individual-market basis during the US Federal Reserve’s previous cycle of low interest rates, which lasted from December 2008 to December 2015. Why is this?

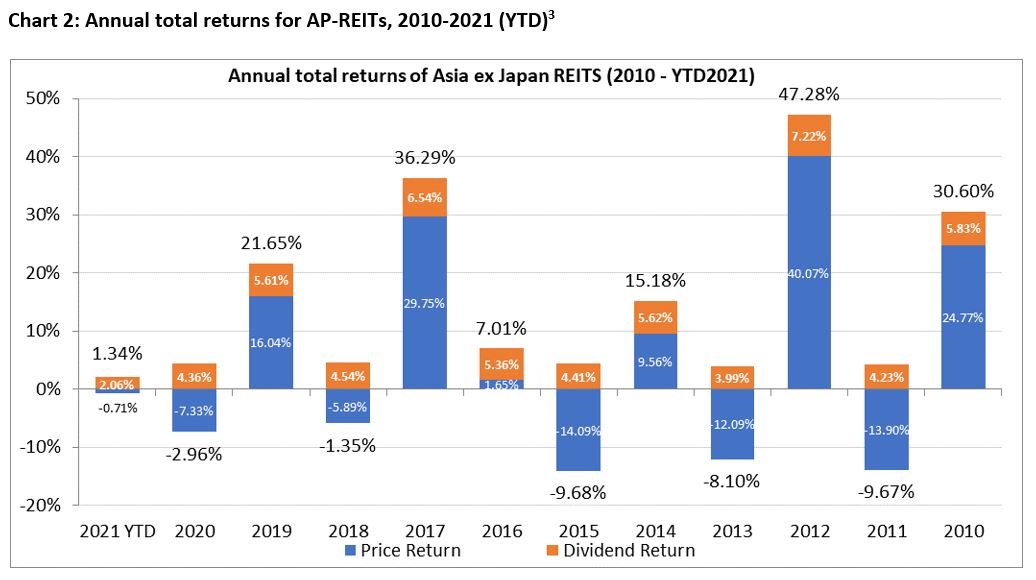

This relative outperformance is based on the ability of AP-REITs to deliver positive dividend returns across a range of the market environments (see Chart 2). Indeed, REITs are required to pay a significant portion of operating income as dividends that serves as a cushion to steady returns during times of market volatility.

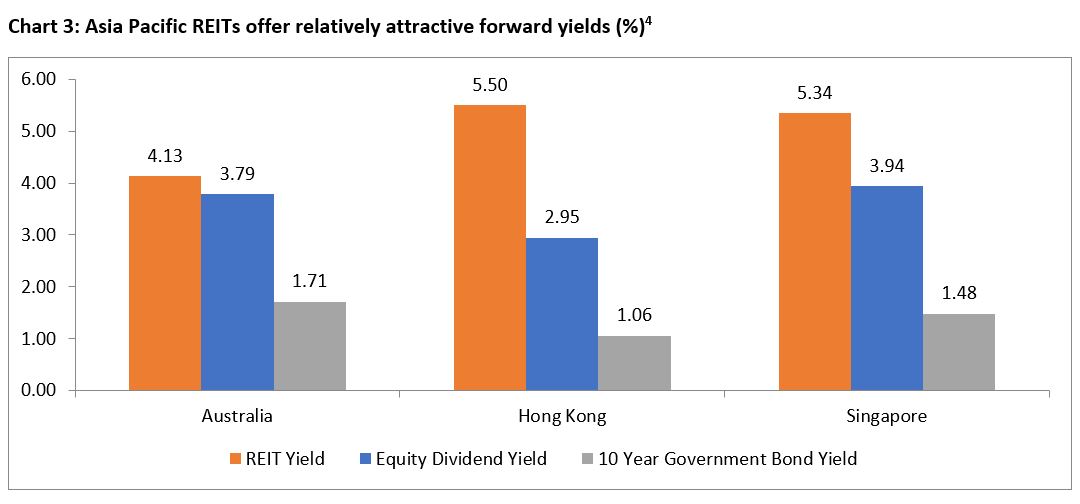

Thus, in a lower for longer interest rate environment, the more attractive and steady yields that REITs offer are one of the key value propositions for the asset class (see Chart 3). REITs may outperform in a lower interest rate environment with a lower risk-free rate and the opportunity for investors to earn more yield for holding risk securities.

At first thought, the logic is the opposite in a rising or higher interest rate environment: investors may be given less attractive compensation for risk due to a higher risk-free rate, particularly compared to lower-risk alternatives. In addition, many REITs hold varying levels of debt to finance their assets and as such, higher rates could result in higher interest burden. Overall, our current house view is that we are in a “lower for longer” interest rate environment with expectations that key developed market central banks likely will not raise interest rates until 2023, based on current guidance, which should mean interest rates serve as a tailwind for the asset class over the near-term.

However, as we emerge from the COVID-19 pandemic, inflation is also on the mind of many investors. Generally, real estate offers investors a hedge against inflation, as rising prices for goods and services is usually also reflected in increasing prices for real estate and rents. In the case of REITs, some lease structures have built-in annual step-ups or CPI-linked rental increases, which should help mitigate some of the impact of higher inflation for landlords and net operating income. Specific REIT segments may also be affected more than others. For example, office REITs are more sensitive to changes in employment and economic growth than other segments.

But there is a notable addition to the above analysis: not all inflation is necessarily the same. Historically, REITs tend to outperform during periods of inflation driven by economic growth as the pricing of leases is more competitive based on expectations of improving business conditions due to greater demand for real estate space. However, inflationary periods experienced during lower economic growth may reduce the benefit of the hedge. While it is too early to tell the length and ultimate extent of current inflationary pressures, REITs are arguably better positioned than other traditional asset classes to hedge the potential impact for investors.

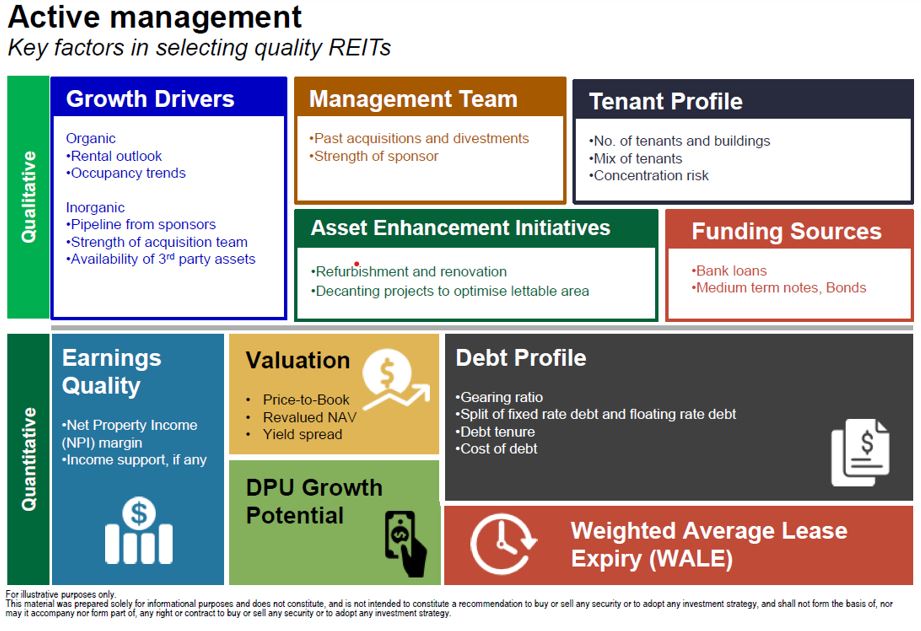

Manulife Investment Management’s unique active approach to AP-REITs: The Manulife Asia Pacific REITs Fund5 (the Fund) Manulife Investment Management has significant experience investing in REITs, both globally and in the region. We have adopted a unique, active approach to AP-REIT selection that provides benefits for investors. Indeed, as part of our robust selection process, we closely scrutinise an array of qualitative and quantitative factors (see Chart 4) before any REIT is included in our portfolio. This allows us to identify those names with attractive risk-adjusted return profiles for the Fund’s two main categories of holdings: income-producing REITs and growth-based real estate equities.

Indeed, the Fund is designed and managed based on these unique active management capabilities and commits to at least 70% of holdings dedicated to income generation. However, the asset allocation to regional REITs can be as high as 100%.

Overall, AP-REITs have the potential to offer investors a stable income and comparatively attractive yields through the following factors:

The remaining portion of the portfolio (up to 30%) is dedicated to property-related equities that provide significant capital-growth potential. These include real-estate developers and property-management companies. In general, the non-REIT elements of the portfolio display these characteristics:

Conclusion: AP-REITs possess a distinct hybrid structure that provides investors with steady, dependable income while also providing a potential upside for capital appreciation. They have also historically performed well in low interest-rate environments, which we anticipate will persist globally over the near term. Manulife Investment Management’s unique active approach accentuates the benefits of REITs, applying rigorous selection criteria to ensure investors get the most out of this emerging, exciting asset class.

YOU MAY ALSO LIKE THIS

Sources 1 Ayala Land Subsidiary- AREIT was listed in 2020. 2 Bloomberg, as of 31 December 2015. Australia REITs measured by S&P/ASX 200 A-REIT Index, Hong Kong REITs measured by Hang Seng REIT Index, Singapore REITs measured by FTSE ST Real Estate Investment Trusts index; Asia ex Japan REITs measured by FTSE EPRA/NAREIT Asia ex Japan REITs Index, Singapore Equities measured by Straits Times Index STI Total Return Index, Hong Kong Equities measured by Hang Seng Index, Australia Equities measured by S&P/ASX 200 index, Asia ex Japan equities measured by MSCI AC Asia Ex Japan index (total return). Past performance is not an indication of future results. 3 Bloomberg as of 31 May 2021. Asia ex Japan REITs are represented by FTSE EPRA/NAREIT Asia ex Japan REITs Index. Performance in USD. 4 Bloomberg as of 31 May 2021. REIT Yield and Equity Dividend Yield are the projected 12-month yield from Bloomberg consensus. REIT Yield: Australia REIT – S&P/ASX 200 A-REIT Index, Hong Kong REIT – Hang Seng REIT Index, Singapore REIT – FTSE ST Real Estate Investment Trusts index. Equity Dividend Yield: Straits Times Total Return Index, Hang Seng Index, S&P/ASX 200 index. 10 Year Government Bond Yield = Local Generic 10- year Government Bond Yield. Projections or other forward-looking statements regarding future events, targets, management discipline or other explanations are only current as of the data indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different than that shown here. 5 The full name of the Fund is Manulife Global Fund-Asia Pacific REITs Fund.

Important Information Manulife Global Fund (the “Company”) is an open-ended investment company registered in the Grand Duchy of Luxembourg. The Manulife Global Fund – Asia Pacific REITs Fund (“the Fund”) is recognised under the Securities and Futures Act of Singapore for retail distribution. The Company has appointed Manulife Investment Management (Singapore) Pte. Ltd. as its Singapore Representative and agent for service of process in Singapore.

The information provided herein does not constitute financial advice, an offer or recommendation with respect to the Fund. The information and views expressed herein are those of Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) and its affiliates (“Manulife”) as of date of this document and are subject to change based on market and other conditions. Manulife expressly disclaims any responsibility for the accuracy and completeness of, and the requirement to update, such information.

Investments in the Fund are not deposits in, guaranteed or insured by Manulife and involve risks. The value of units in the Fund and any income accruing to it may fall or rise. Past performance of the Fund is not necessarily indicative of future performance. Opinions, forecasts and estimates on the economy, financial markets or economic trends of the markets mentioned herein are not necessarily indicative of the future or likely performance of the Fund. The Fund may use financial derivative instruments for the purposes of investment, hedging or efficient portfolio management. Investors should read the Singapore prospectus and the product highlights sheet and seek financial advice before deciding whether to purchase units in the Fund. A copy of the Singapore prospectus and the product highlights sheet can be obtained from Manulife or its distributors. In the event an investor chooses not to seek advice from a financial adviser, he should consider whether the Fund is suitable for him.

Distributions are not guaranteed. Investors should refer to the Singapore prospectus for the distribution policy of the Fund. The Directors of the Company shall have the absolute discretion to determine whether a distribution is to be made in respect of the Fund as well as the rate and frequency of distributions to be made. Distributions may be made out of (a) income, or (b) net capital gains, or (c) capital of the Fund, or (d) gross income while charging all or part of the fees and expenses to capital, or (e) any combination of (a), (b) , (c) and/or (d). Past distribution yields and payments are not necessarily indicative of future distribution yields and payments. Any payment of distributions by the Fund is expected to result in an immediate decrease in the net asset value per share of the Fund.

This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. |