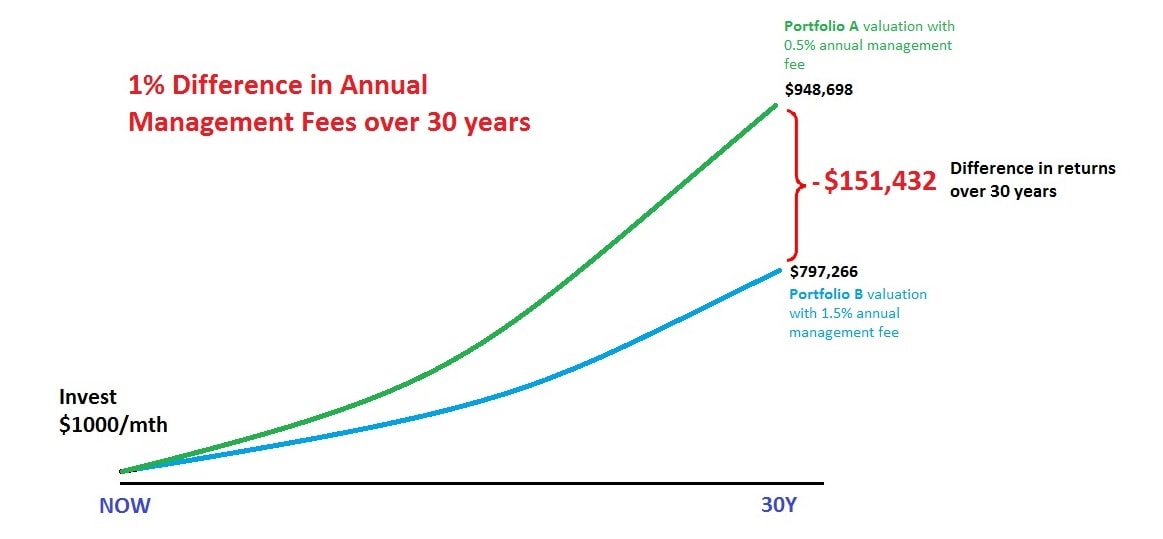

How a 1% fee could cost Millennials $151,432 in retirement savings

Every investor knows that fees can eat into your investment returns. Fees include annual management fees charged by the fund house that are already factored into the fund’s Net Asset Value (NAV). There are also other fees such as platform fees and sales charges that you may need to pay.

Let’s assume for an investor who has $1,000,000 in his investment account and has to pay a 1% fee, that could mean $10,000 every year, and a 1% fee may not be that much if your investment sum is small. But it may not be so for Millennials because of one important factor: Time.

Assuming a young investor who invest $1,000 every month and has 30 years to save for his retirement, that could mean $151,432 lost just on fees!1.

Above graph is for illustration purpose only. Both portfolio returns are projected based on 6.5% annual compounding return before annual management fee. Portfolio A has a 0.5% annual management fee and Portfolio B has a 1.5% annual management fee, hence Portfolio A has a net return of 6% and Portfolio B net return of 5% respectively. Note that typically the returns shown on actual fund factsheets have already factored in the respective annual management fees.

Once you, as a well-informed investor, has decided to embark on a low-cost investing journey, one of the next best move to get a higher investment return is to invest in a low-cost fund. By low-cost, we mean that the Annual Management Fee or Total Expense Ratio that the fund charges is kept to the lowest in their respective category. Furthermore, why pay sky-high fees when one can choose to invest on a platform that offers no sales charge and zero fees?

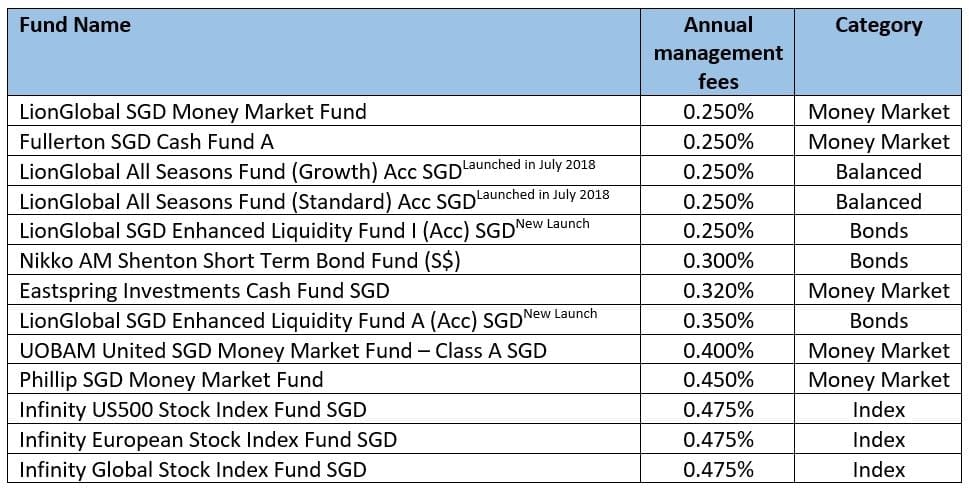

So what does this mean for you as an investor? Annual management fees, like all other fees, may cut into the gains of investors’ returns and a 1% fee over a long term could mean a lot. While the annual management fee of unit trusts are about 1.5% on average, there are still funds that charge less than 0.5% p.a. besides the usual Money Market Funds (mainly used as a Cash management facility), and Index Funds, which typically has an annual management fee of 0.475%.

Here are some funds on dollarDEX that are charging less than 0.5% p.a. annual fees.

Standing out from this list are the LionGlobal All Seasons Fund and LionGlobal SGD Enhanced Liquidity Fund A that were launched last year. With a management fee of 0.25% and 0.35% per annum, it has one of the lowest fees in the Balanced and Bonds fund category, on par with many Money Market funds and beating more than 900 other funds available on dollarDEX, including most Bond funds.

How did Lion Global Investors maintain the low fee?

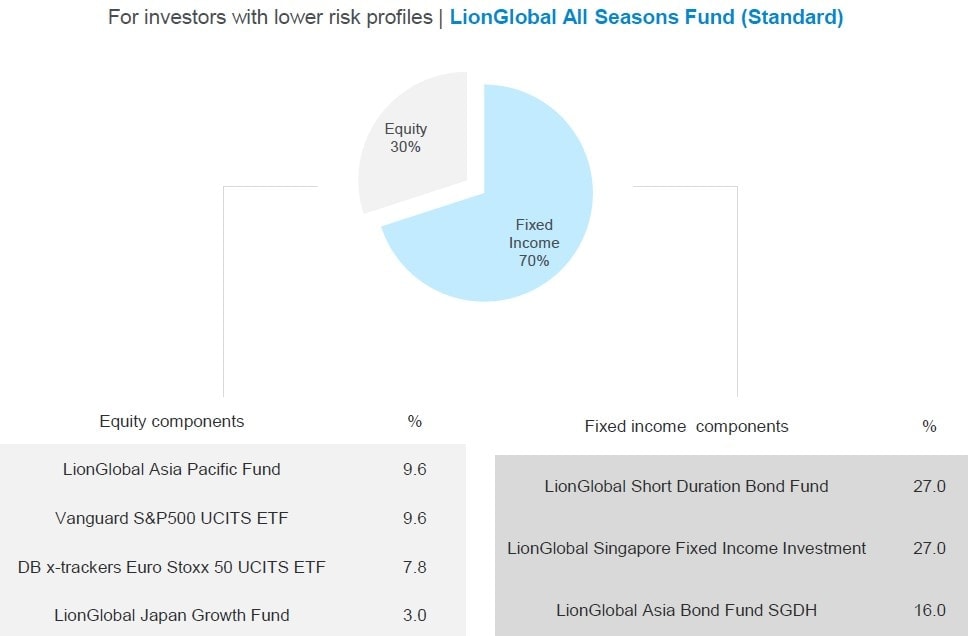

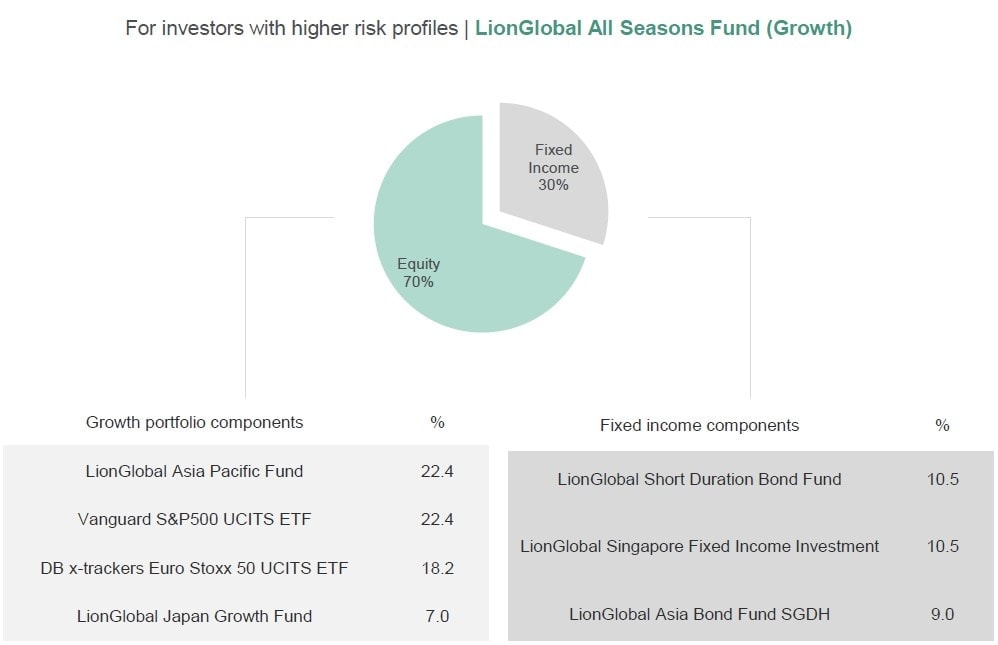

LionGIobal All Seasons Fund adopts a fund-of-funds strategy where it holds only seven funds split across Actives & Passives, Fixed Income & Equities as well as Geographical Regions. Unlike most fund-of-funds, which has double-layered fees, the feeder funds for LionGIobal All Seasons Fund, such as LionGlobal Asia Pacific Fund does not charge LionGIobal All Seasons Fund any management fees, thus they are able to offer such a low fee structure to investors.

Click below to find out more about the LGI All Seasons funds:

LionGlobal All Seasons Fund (Growth) Acc SGD

LionGlobal All Seasons Fund (Standard) Acc SGD

While the LGI SGD Enhanced Liquidity Fund I (Acc) SGD has a management fee of 0.25% but it is of institutional share class and has a minimum investment amount of S$1,000,000 that puts many retail investors out of reach. Regular investors like us have the retail share class LGI SGD Enhanced Liquidity Fund A (Acc) SGD that is also attractively priced at 0.35% per annum in management fee.

The LGI SGD Enhanced Liquidity fund is unique as it is a bond fund that works similar to a Cash Management Fund but has a better yield at 2.4% Yield-to-Maturity3. It uses an Amortized Cost accounting method, instead of the usual Mark-to-Market valuation, hence it is able to ensure that the NAV price per unit does not fluctuate with market volatility but instead, priced at its intrinsic value since each underlying security purchased by the fund is held to maturity.2

Besides the LionGlobal funds mentioned above, the Nikko AM Shenton Short Term Bond Fund is another low cost option in the list that is favourable in this current rising rate environment.

In summary, it is important to consider the annual management fees in your choice of funds and truly maximise your investment returns by not letting fees eat into them. While Bond funds typically have lower fees and corresponding lower returns compared to Balanced funds, LionGlobal’s new offerings aim to defy the norm and disrupt this space with their new offerings. Find out more about these funds by using our intuitive Fund Finder today!

Footnotes

Sources:

1MSN: https://www.msn.com/en-us/money/tools/timevalueofmoney

2Texas CLASS: https://www.texasclass.com/the-showdown-mark-to-market-vs-amortized-cost/

3LionGlobal SGD Enhanced Liquidity Fund: Click here

YOU MAY ALSO LIKE

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 15/01/2019.