|

Investing into China: The Growing Giant 11 May 2021

Pandemic: First in, first out China staged a phenomenal economic rebound when COVID-19 crippled the global economy in 2020, being the only major economy to expand in 2020.1 After suffering a negative shock in the first quarter of 2020 due to the protracted shutdown of industrial production and severe restrictions on consumer expenditure due to lockdowns, the Chinese economy staged a strong recovery in economic momentum for the rest of 2020, buoyed by export demand and gradual recovery in domestic economic activity.2

After a phenomenal 2020 and a strong start to 2021, the CSI 300 gave up its gains and underwent a correction in February, prior to which Chinese officials had repeatedly warned of asset bubbles and touting the curbing of risks in the financial system as a key policy goal in 2021.3 Still, even though A-share market valuations continue to be elevated against historical valuations after a 2-year run up, it remains relatively low compared to other countries in the world.

In light of a stronger global rebound from the pandemic, the International Monetary Fund (IMF) raised its 2021 growth forecast for China to 8.4% in April. The upgraded projection sits 0.3% above the IMF's previous prediction in January and would mark the country's strongest growth rate since 2011.1

Government’s focus and Central bank (PBOC) With a GDP growth target of around 6% set for 2021, some believe that the Chinese government expects growth to moderate as it takes steps to curb debt-related risks.3 China aims to become a high-income country by the end of 2025, and to double the size of its economy and GDP per capita by 2035. The year 2021 is thus crucial to China as it marks the start of the two set time frames.4

While the Chinese government’s cautious attitude toward expansionary macroeconomic policy reflects its unease over inflation and financial risks, the People’s Bank of China (PBOC) has so far kept the nation’s Loan Prime Rate - the benchmark lending rate for corporate and household loans - steady for the 11th straight month in March.5

Opportunities within the 14th 5-year Plan Underpinned by a powerful domestic demand engine, the Chinese government is focused on increasing domestic spending and unlocking the significant savings of the country’s populace.6 Underscoring the strength of the Chinese consumers and their growing role in China’s economic growth, Singles’ Day in 2020 generated gross revenue almost US$29.5bn more than the combined revenue of similar events in western countries such as Black Friday, Prime Day and Cyber Monday.7

China’s 14th Five Year Plan’s emphasis on boosting domestic demand, supply chain upgrading, technology self-sufficiency, and further opening the country’s domestic markets implies opportunities for investors in multiple sectors, such as tech, clean energy, education, and healthcare.4 The nation’s push towards net zero carbon emission by 2060 and drastically reduce the use of coal and fossil fuels by replacing them with renewables should also bode well for leading companies in the related tech and renewable energy sectors, such as Electric Vehicles and solar energy supply chain.7

Case in point 1: Technology China is allocating significantly more resource to increase patent counts and overall research and development of advanced technologies, which the government is expecting to grow 7% every year.7

While recent developments on the Chinese government’s scrutiny over internet companies have raised concerns, Bloomberg Economics view the move as a boon for online commerce and consumption over the longer term. The team opines that while curbing monopolies may be painful for incumbents in the near-term, more competition should be good for consumers and the continued growth of the industry over the longer term.8

Case in point 2: Biopharmaceutical Seeking to cultivate a homegrown biotech industry, regulators have accelerated approval times for cutting-edge therapies, extended patent protections, clamped down on corruption and expanded government spending, garnering interest from foreign researchers and venture capital firms.

The government is also allowing foreign drug makers to tap into China’s vast market, loosening rules for foreign manufacturers to circumvent lengthy clinical trials already conducted in their home markets.6

The Bond Market As China’s interest-rate differential with the United States shrunk in recent times, international investors slowed their purchases of Chinese government debt, marking the first drop in foreign investors’ positions since February 2019.9

However, index provider, Financial Times Stock Exchange (FTSE) Russell, had also recently announced the inclusion of Chinese government bonds into its widely followed World Government Bond Index (WGBI) in October, which should usher in an estimated US$150 billion to US$180 billion of new inflows into the Chinese bond market this year.10

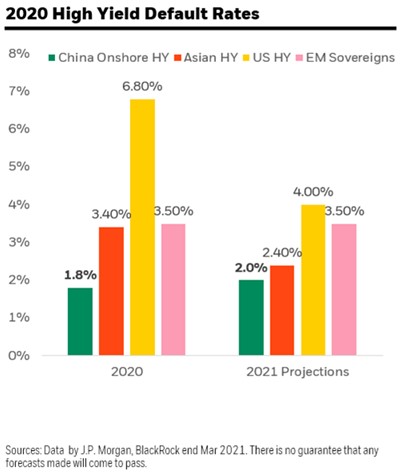

Outside of government bonds, China’s significantly healthier default rates within the high yield space relative to global peers also highlights the economy’s resilience and explains the quicker rebound from 2020’s epidemic.

Sources: Data by J.P. Morgan, BlackRock end Mar 2021. There is no guarantee that any forecasts made will come to pass.

Conclusion With the government focusing on quality growth and to smooth the path for economic policy and recovery, China’s current macroeconomic backdrop presents an opportunity. China continues to lead the world for structural changes, with the nation’s highly developed internet ecosystem and growing middle class charging a powerful transition towards a balanced economy spearheaded by domestic consumer spending.6

There seems to be no foreseeable substantial change in the US’s trade policy on China despite the new administration, and it seems unlikely there will be a scaling back of restrictions or a rollback of tariffs imposed on Chinese companies.11

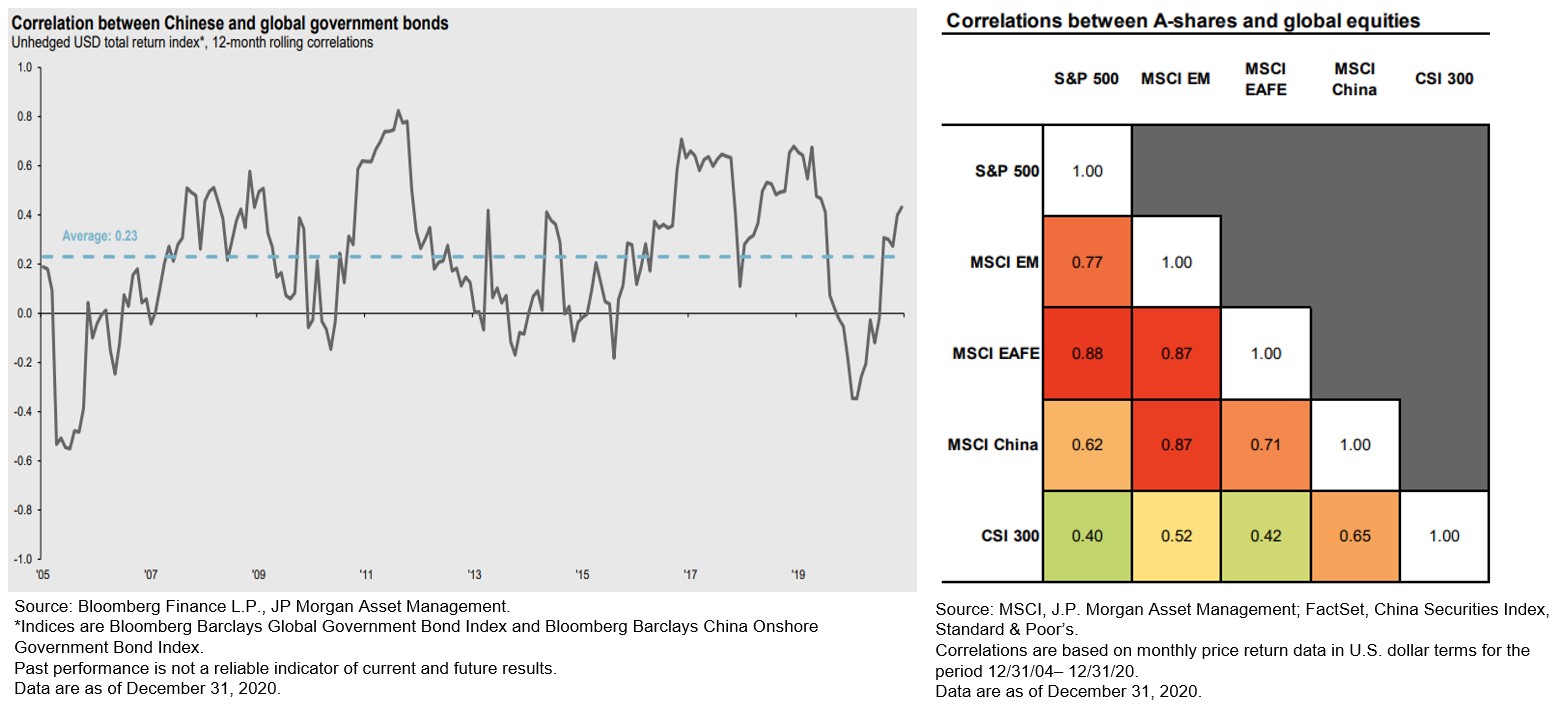

Active management can be a differentiator to long-term investment performance, as agility in repositioning portfolios in adherence to dynamic market conditions cannot be achieved through passive strategies. With correlations treading away from its global peers, China’s bond and equity space presents a great opportunity set for investors seeking diversification within the respective asset classes or within their portfolios.

YOU MAY ALSO LIKE THIS

|