Highlights of H2 market outlook (Part 2)

In part two of our H2 Market Outlook series, we have summarized key highlights from BlackRock and Wellington Management on behalf of UOB Asset Management. This follows our H2 Market Outlook seminar in July where we invited fund partners to share their views on the market as well as opportunities for the second half of 2018.

Investment opportunities in a world of synchronized expansion by BlackRock

At the seminar, BlackRock shared that they favour US equity due to strong expected earnings compared to other regions. With the rising political risk in the European bloc, BlackRock believed that this risk has not been fully priced-in yet, thus preferring a wait-and-see approach. On the equity valuation front, Emerging Market equities particularly Asia, looks attractive relative to history and compared to other regions.

Given the rising interest rates, cost of borrowing for corporates will weigh in on profitability, hence credit quality and selection is key. With that, BlackRock favours Investment Grade bonds versus the High Yield segment.

BlackRock also gave an in-depth coverage on the Financials sector, through the BGF World Financials Fund, where they believe that Financials are structurally attractive due to the access to long-term trends in Digital Finance & growing wealth in Emerging Economies. Valuations on a forward P/E ratio is amongst the lowest, and the macro environment is supportive driven by strong economic growth (which leads to stronger loan growth), higher interest rates (leading to higher net interest margins) and US policy reforms (lowering regulatory costs and possibly lower corporate taxes).

Here is what BlackRock have to say about their views on the market in the Q&A below.

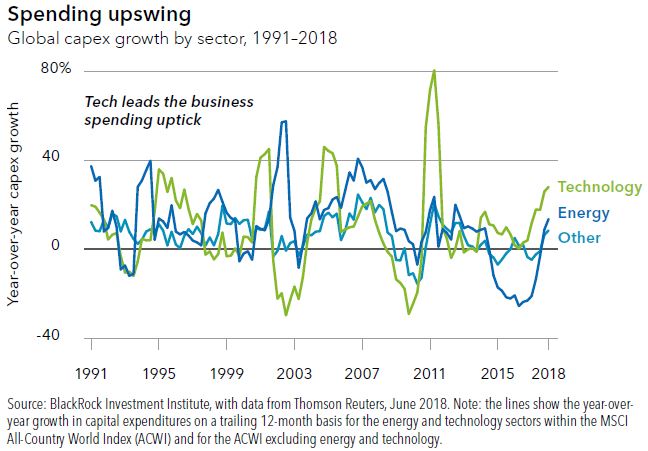

Besides the financial sector, what are some of the other equity sectors that investors can consider and why?

Financials and technology are our favoured sectors. Capex is picking up globally - with technology leading the charge (Refer to the Spending upswing chart). Years of policy uncertainty and low confidence kept company purse strings tight. Their re-opening in an age of technology and evolving consumer behaviours has much of the spending directed at intellectual property and innovation - a boon for technology firms. The spending uptick could spill into 2019 as companies adjust to new US tax laws – provided that trade tensions do not pinch confidence. We see some notes of caution rearing.

The story is not US-only. High capacity utilisation rates and ageing assets in Europe point to room for spending. In China, investment in strategic initiatives is set to accelerate even as it declines in heavy industries. History shows big spending can eat into stock returns. Yet spending discipline among many companies gives us confidence that profit margins and earnings could be well insulated.

What should investors take note of when investing in the respective equity regions?

From a US dollar perspective, we have an overweight tactical view on US equities. Unmatched earnings momentum, corporate tax cuts and fiscal stimulus underpin our positive view. We like momentum. We prefer quality over value amid steady global growth but rising uncertainty around the outlook. Financials and technology are our favoured sectors.

We have overweight tactical views on EM and Asia ex-Japan equities as well. In EM, economic reforms, improving corporate fundamentals and reasonable valuations support EM stocks. Above-trend expansion in the developed world is another positive. Risks such as a rising US dollar, trade tensions and elections argue for selectivity. We see the greatest opportunities in EM Asia.

In Asia ex-Japan, the economic backdrop is encouraging, with near-term resilience in China and solid corporate earnings. We like selected Southeast Asian markets but recognise a worse-than-expected Chinese slowdown or disruptions in global trade would pose risks to the entire region.

We are neutral on Japanese equities. The market's value orientation is a challenge without a clear growth catalyst. Yen appreciation is another risk. Positives include shareholder-friendly corporate behaviour, solid company earnings and support from Bank of Japan stock buying.

However, we do have a tactical underweight view on European equities. Relatively muted earnings growth, weak economic momentum and heightened political risks are challenges. A market dominated by value sectors also makes the region less attractive in the absence of a growth upswing.

What are some of the things investors can do to build portfolio resilience?

As uncertainty picks up, so does the importance of portfolio resilience. Investors can consider shortening duration in fixed income, going up-in-quality across equities and credit, and increasing diversification.

We prefer to take risk in equities and still favour momentum. We prefer quality over value amid steady global growth but rising uncertainty around the outlook. Momentum has been the market leader, but quality companies demonstrating high profitability and low leverage have also outperformed global equities broadly.

This was evident as trade fears ratcheted up. We see higher-quality stocks outperforming in times of rising macro uncertainty and risk aversion. We find many such companies in the US, where earnings growth fuelled by the tax overhaul offers an edge. We favour US short duration in fixed income but longer-term US Treasuries and German bunds should play their traditional role cushioning any growth shocks. We prefer an up-in-quality stance in credit.

Thematic investing such as focusing on companies that excel on environmental, social and governance (ESG) metrics can also lend long-term resilience to portfolios, we believe.

What kind of outcome does BlackRock expect from the recent US-China trade spat?

Trade risks weigh on our outlook. US-China economic tensions have been heating up, with trade the hot button. The tensions go far beyond the bilateral trade gap; the real rivalry centres on China's technology development programme - and its competitive and national security implications for the US. Negotiating on tariffs and imports will likely prove easier than getting China to compromise on tech and other strategic initiatives. We see a prolonged period of tensions as a result, including around restrictions on Chinese investments in the US and transfer of technology to China. Importantly, there is bipartisan support in the US Congress to be tough on China when it comes to trade.

A further sharp escalation in trade actions globally could derail the economic expansion. First, falling business confidence may lead companies to delay or cancel investment plans. Second, tariffs can push up costs and depress demand. Integrated global supply chains risk amplifying this impact.

Neither the US nor China wants a full-blown trade war, in our view. Yet structural rivalry means tensions are likely to heat up and persist.

To find out more about BlackRock World Financials, click here.

Global market outlook: Quality growth approach by UOBAM

Finally, Wellington Management on behalf of UOB Asset Management echoes BlackRock's views and expects strong fundamentals to support risk assets in 2018, favouring equities over bonds and credit over government bonds. Wellington highlighted that tight spreads limit upside opportunities in investment grade bonds and cautioned against High Yields, favouring high quality credit in US and Europe.

For investors who are concerned about the longevity of the current Bull Run, Wellington Management also shared that this current bull market of about 10 years is not the longest recorded in history. The longest bull market for the S&P500 lasted for 14.6 years post World War Two followed by 13.9 years post-Great Depression.

Here is what UOBAM have to say about their views on the market in the Q&A below.

What is UOB Asset Management's view on the technology sector?

Broadly speaking, we remain sanguine on the outlook for global technology equities. Despite the strong run of this sector over the past year, we still believe valuations are largely supported by strong fundamentals. We continue to see a long runway for solid performance and remain focused on quality, long-term secular growth companies that have the ability to deliver double-digit growth over time. Many of the trends in the technology space that were once cyclical in nature have become more secular with the rise of powerful forces such as machine learning, Internet-of-Things, artificial intelligence, electrification of automobiles, rapid data growth, and cloud computing among others.

We are however, exercising a bit of caution in some areas within the technology sector where, despite structural drivers intact, a few macroeconomic factors could present headwinds. This would include continuing trade tensions between the US & China, rising rates and inflation that could hinder further margin expansion, and the progression into the more mature stages of the global economic cycle.

What EM exposure does UOB Asset Management like? Is the recent EM volatility an opportunity to buy or should investors wait and see?

We are constructive on the prospects for EMs, which are, in general, either in early- or mid-cycle stages of their economic recovery. EM inflation remains largely benign with some countries even in the process of monetary easing due to sharp declines in inflation. Moreover, many EM real rates are positive (and higher than among developing markets), providing a cushion for capital flows and lessening the need for significant tightening. Overall, valuations are not too rich with the MSCI Emerging Market Index still trading below its historical price to book and below global and US valuations.

Some of the regional opportunities include:

Positive inflection points in Latin America - Brazil's central bank cut its benchmark rate by more than 5% in 2017. Inflation has been trending lower since the start of 2016, commodity prices have stabilized, and private consumption is growing. While the recovery remains tepid, we expect potential acceleration over the coming quarters. Argentina also remains an underappreciated growth story. There, inflation and interest rates have been coming down, and investment and personal consumption are showing signs of strength, notably via robust construction activity and a pickup in auto sales.

Innovation and SOE reform in China - China, boasting a staggering pace and scale of innovation, is now home to one of the world's leading global e-commerce and cloud service providers, the world's largest gaming company, a global leader of lenses for automotive safety and autonomous systems, and several of the world's largest security and surveillance system producers. Over the last decade and a half, China's patent applications have surged and now account for more than 40% of the world's total applications. China's stock market composition is also increasingly transitioning away from state-owned enterprises (SOEs) with the majority of China's market capitalization now in private enterprises.

India: Attractive in the medium term - Despite structural reforms in India that are disrupting established ways of doing business that may reduce economic growth in the near term, we believe it contributes to a stronger outlook over the medium term. Over time, we believe that reforms like the GST and a new bankruptcy law, among others, will ultimately facilitate creative destruction of capital. Businesses are taking advantage of current reforms, which are breaking down regulatory barriers to scale and making India an exciting place to hunt for potential investment opportunities. We see economic development as a powerful force for structural change in EM. Many thematic investment opportunities enjoy secular tailwinds, yet they tend to be underrepresented in traditional indexes; areas that include automation, logistics, health care provision, environmental consciousness, and discretionary lifestyles.

With the recent pick-up in global economic growth, will it spill over to the Commodities sector? Is it timely to look into the Commodities sector?

The second quarter started off with strong performance across commodities, as the market initially shook off the trade tariff discussions and instead seemed to respond to the strong fundamental story. Since mid-May, however, a lot more attention has been paid to the prospect of trade wars and the negative impact that they could have on global demand for a range of commodities. A drop off in demand would certainly dampen our bullish outlook, but we remain focused on what is still a strong fundamental story across many of the commodities.

Without being blind to the risks that have driven this pullback, we are still supportive of the current cyclical environment in commodities. Supplies across many commodities remain constrained, putting balances into deficit for 2018 and 2019.This environment should allow for a lower rate of demand that still draws down inventories. Furthermore, the low price environment that we have been in has delayed investment in new capacity, and the uncertainty that we have today will continue to delay any additional spending. Every day that commodity producers delay investment in new supply will ultimately lead to deeper deficits in the future.

We continue to believe that we are at a point in the economic cycle where commodities should do quite well. Global PMI numbers have been strong, unemployment remains low, and consumer confidence has stayed elevated. This should lend support to overall commodity demand, in spite of negative headlines about trade. We continue to watch trade developments as a risk, but as it has taken several years for commodities to reach such positive fundamentals, we question whether it could be undone overnight.

To find out more about the UOBAM Global Quality Growth fund, click here.

With these insights and strategies from PIMCO, Lion Global Investors, UOB Asset Management & BlackRock, consider taking the next step to find out which funds can work for your portfolio. Simply search for the funds you want on dollarDEX using our Fund Finder to get started!

YOU MAY ALSO LIKE

BlackRock Investment Institute, as at July 2018

In Singapore, this material is issued by BlackRock (Singapore) Limited (company registration number: 200010143N). Investment involves risks. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

International investing involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Company name is only for explanatory purposes and does not constitute as investment advice and is subject to change.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 17/09/2018.