Equity market setbacks are normal

Summary

The recent US equity market setback seems to be little more than a wobble. The global economy is not in recession, although it is slowing down, and monetary policy is still accommodative across the board. Nevertheless, this is cold comfort to investors who have become sensitive to even smallish corrections.

Key takeaways

- Neither the US nor the global economy are close to recession: the Fed and other central banks are still accommodative, and financial conditions are still loose

- Longer-term Treasury yields are not at levels that should force asset allocation changes out of equities and into bonds

- Trade wars are painful, but they should not have a huge negative economic cost

- Quantitative tightening and rising US rates are supporting the US dollar, but it has risen only 7% this year

- Equity valuations are high, but shorter-term earnings growth is still strong

- A bullish stance would be supported by US Treasury yields stabilising at current levels (around 3.15%)

- A bearish view would see high-yield credit spreads start to widen from current levels

Global equities in general - and US equities specifically - have been tearing upwards for the past decade with few serious setbacks. Cushioned by the super-palliative combination of ultra-low interest rates and quantitative easing (QE), investors moved away en masse from sovereign and investment-grade bonds towards high-yield bonds and equities.

Yet recently, the global equity markets have experienced a series of stumbles that have unnerved investors a bit too much. Setbacks like these are arguably part of the normal process of markets - a way of clearing market excesses - but since the financial crisis, central banks have been loath to tolerate any loss of confidence in policy or in markets. Their supportive monetary policy has fostered a low-volatility, high-leverage, buy-the-dip mindset among investors, and a sense that central bankers have their backs. The upshot is a widespread sensitivity to even smallish corrections of 5% - such as the kind we’ve recently seen.

Admittedly, this jumpiness is mostly a US response; years ago, Europe endured its own euro-zone crisis while emerging markets were roiled with political and local issues. Nevertheless, the old adage still holds true: when the New York market sneezes, the world catches a cold.

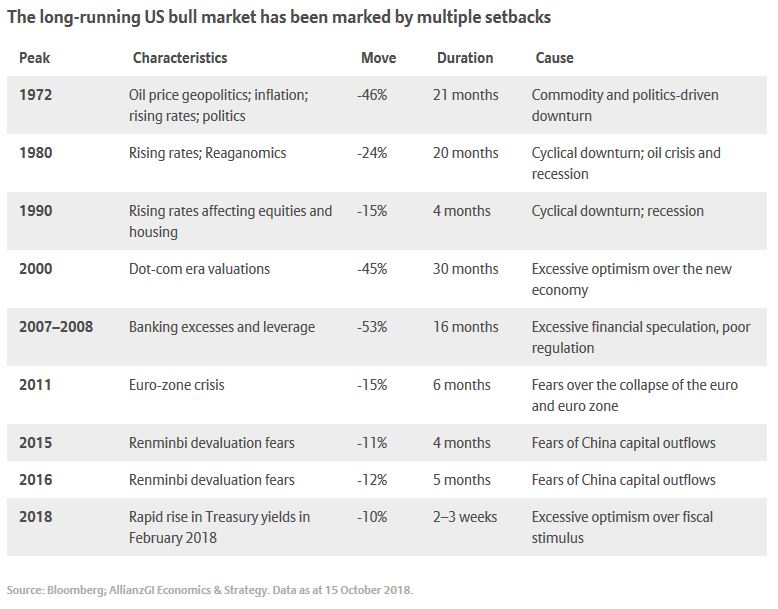

Significant market corrections in US history

The brief list of equity market setbacks outlined in the accompanying table reveals a range of events, durations and magnitudes. It is also worth noting that the US fixed-income market hasn’t had a proper setback since the savings-and-loan crisis of the early 1990s, and the debt and loan carnage of 2008-2009.

As the same time, it is notable that nearly all of the triggers seen in the more substantial setbacks are in place today: fears abound over China, excessive fiscal stimulus, high oil prices, political uncertainty and overvaluations.

As the same time, it is notable that nearly all of the triggers seen in the more substantial setbacks are in place today: fears abound over China, excessive fiscal stimulus, high oil prices, political uncertainty and overvaluations.

So where are we now?

This year has been a challenging one for investors globally, with just one asset class - US equities - consistently doing well. In reality, however, growth in US equities has been almost entirely driven by the tech, consumer discretionary and health-care sectors; most other US sectors were down by between 5% and 25% as at mid-October.

The volatility shock of February unsettled investors around the world, yet a number of factors point to this recent bout of nerves as one that is “made in America”:

- A hawkish Fed. The US Federal Reserve remains increasingly hawkish on its interest-rate projections, with the economy at full employment, significant fiscal stimulus at work and consumer inflation emerging.

- Less liquidity. Accelerating quantitative tightening, combined with the new cash repatriation policy in the US, is beginning to impinge on global liquidity conditions for the US dollar. This, in turn, is placing pressure on weaker banking systems, overleveraged emerging-market borrowers and economies that are sensitive to high oil prices - including India and Indonesia.

- Peak earnings. Today’s high earnings are matched by 2019 expectations for the US equity market, supported by President Donald Trump’s tax cuts. Yet this may in fact herald “peak earnings” for this cycle.

- Peak buy-backs. Uncertainty is being fuelled by the quarterly cessation of US corporate share buy-backs. These will reach a record level in 2018, totalling nearly USD 1 trillion this year - 5% of US GDP - and nearly USD 5 trillion over the past five years. Buybacks on this scale have not been a factor in any other market.

- Trade troubles. An increasingly aggressive US trade policy is also redrawing the globalisation consensus of old. The US is looking to corral China and its economic policy as it begins to acknowledge China as a strategic competitor in tech and intellectual property.

- A late-cycle economy. We are late in what is already close to the longest economic cycle on record. The US economy may be burning bright thanks to President Trump’s fiscal stimulus, but it could come down to earth with a bump at some point in the next year or so.

All of these factors have been building for some time, affecting global investor sentiment while US investors have focused on the booming domestic situation. As such, it is possible that the latest market drop is simply the US catching up with global assets that already fell in 2018.

So where are we now?

It is worth remembering that the world is not in a recession, yet a host of factors point to a global economy that is going through some notable changes.

- China is slowing as it rebalances, and it is hoping to avoid a trade war - hence its conciliatory responses to President Trump so far. If China doesn’t stay strong, Germany, Japan and others could see a slowdown in capital expenditures and investment, which is already coming under pressure from higher oil prices.

- Inflation is beginning to brew globally as output gaps close and consumer prices rise. This will be exacerbated by tariffs and the challenging global weather conditions of this past summer, which affected harvests and are likely to drive food-price inflation.

- During 2019, the European Central Bank will follow the path out of QE set by the Fed and the Bank of England, although this will be tempered by rates remaining super-stimulative.

Despite all these factors, politics and policy will have the biggest impact on international investor confidence; Brexit, Italy, India and the Middle East are all capable of providing shocks. And depending upon what happens in November’s US mid-term elections, investors will feel assuaged or need more clarity.

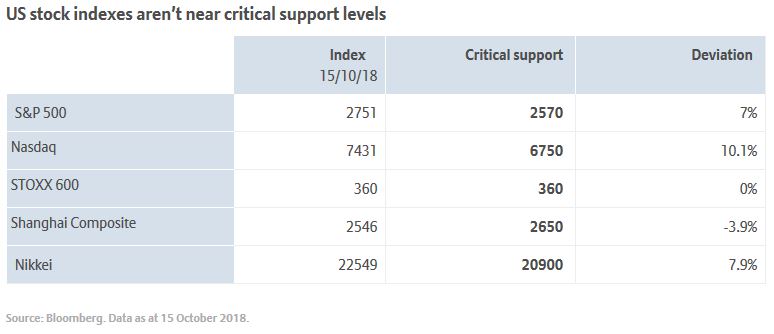

For now, however, this US equity market setback seems to be little more than a wobble. Europe and China are at or near critical support levels, as the accompanying table shows, but we have not yet reached levels that should cause major technical concern for US investors.

Overall, valuations will remain crucial to identifying attractive long-term returns. US equities do seem to be expensive, while Asian and European equities (politics notwithstanding) appear to offer better value, higher dividends and similar long-term growth prospects.

As we get later in the economic cycle, particularly in the US, we expect equity volatility to remain elevated; in this environment, we prefer an active approach, which can help identify winners and losers and provide an extra layer of risk mitigation for portfolios.

YOU MAY ALSO LIKE

Investing involves risk. Equities have tended to be volatile, and do not offer a fixed rate of return. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted. This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor, is affiliated with Allianz Global Investors US LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association];and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 13/11/2018.