Dot-com bubble 2.0 or Industry 4.0?

Dot-com bubble 2.0 or Industry 4.0?

In the past decade since 2008, no other sector has gained more prominence among consumers and individual investors than the technology sector. Incidentally, 29th June 2007 was the day that Apple launched the first generation of iPhone with much fanfare, drawing thousands of Apple fanatics to wait outside Apple and AT&T retail stores even before the device's launch.1 Today, Steve Jobs' legacy lives on as the man who revolutionized the way people interact with their mobile phones by putting the internet in everyone's pocket.2.

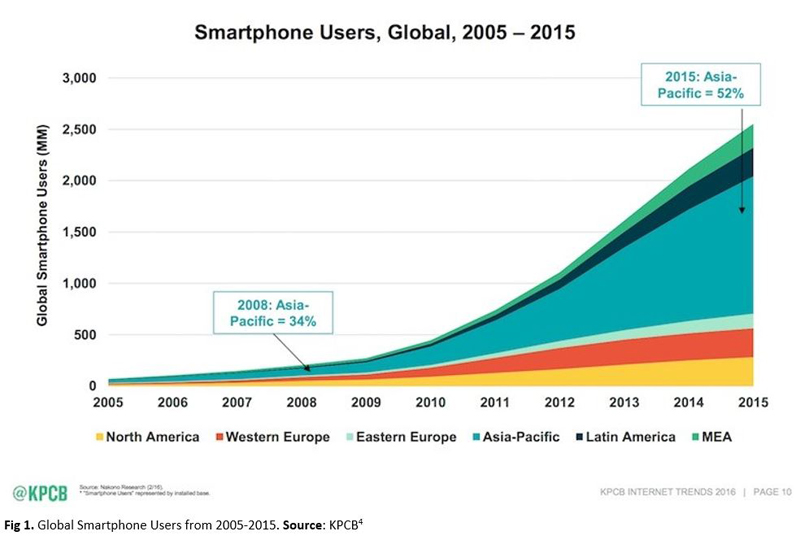

Back in 2008, there were barely 250 million smartphone users globally, by 2015 the number have swelled to over 2.5 billion users, an impressive 10X increase in just 7 years! Today, the estimated number of smartphone users is estimated at about 2.71 billion3, considering a world population of roughly 7.7 billion people, one in three would be owning a smartphone.

While the growth of the smartphone market has benefited Apple Inc. tremendously, catapulting it to become the first publicly-listed US company to be worth over a trillion dollars5 (that's US$1,000,000,000,000.00) back in August 2018, this decade has also seen the emergence and rise of many technology–focused and disruptive business models including unicorns such as Uber, Lyft, Grab, Gojek & Didi Chuxing which have disrupted the transportation industry, AirBnB for the hotel industry, Tesla for the automotive industry and many others, some of which have recently IPO–ed and many are planning to publicly–list after years of venture–led funding.

In the recent years, we have also seen the coining of the US FAANG (Facebook, Amazon, Apple, Netflix & Google) and Chinese BAT (Baidu, Alibaba & Tencent) stocks which have done exceptionally well for their long–term shareholders.

Could this be dot-com bubble 2.0?

The dot–com bust in the early 2000s was a painful memory for those who have been through it. At that time, the Nasdaq Composite index, which included many Internet–based companies, peaked in value on March of 2000 before it all came crashing down. The aftermath of the dot–com bust lasted till October 2004 after a series of follow–on setbacks including the 9/11 terrorist attack in 2001 as well as other major scandals like the infamous Enron accounting scandal and the Worldcom & Adelphia Communications scandal in 2002.6

One could draw a few similarities between the dot-com boom in the 1990s to the current bull market in technology stocks:

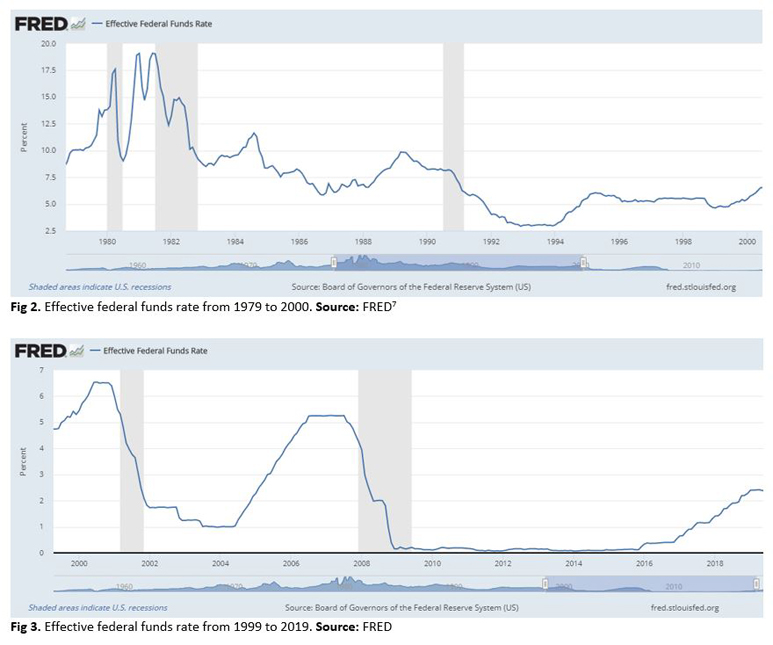

- Relatively benign interest rates — US interest rates during 1990s were relatively low, hovering around 5–6% compared to those in the 1980s. Similarly, interest rates post–2008 crisis was also near rock bottom post–2008 global financial crisis. This led to the increased availability of capital to be deployed as investors and venture capitalists are willing to seek higher returns from more speculative investments.

- Spending tendencies of internet companies — Most internet companies incurred net operating losses as they spent heavily on advertising and promotions to harness network effects and to gain market share as quickly as possible. Many of them offered their products and services for free, or at a discount with the expectation that they could build enough brand awareness to charge profitable rates for their services in the future. The ease of raising money from venture capitalists also led some companies to spend lavishly on elaborate business facilities and perks for employees. It was the way dot–com companies operate in the 1990s and it is also the way that many fast-growing technology start–ups operate now.

- Big names going IPO — Household names in the 1990s such as Netscape, Yahoo!, Lycos and Excite all went public and were extremely successful in their IPOs before slowly fading away after the dot–com bubble burst, save for Yahoo!. Similarly, prominent unicorns in recent times that floated their shares include Uber, Lyft, Pinterest & Slack in 20198 as well as Spotify & Dropbox in 2018.9 To–date, many of them have yet to turn profitable while many more are rushing to list before the economic conditions worsen amidst the trade uncertainty.10

While there are many similarities, there are also differences:

- Cusp of the Fourth Industrial Revolution

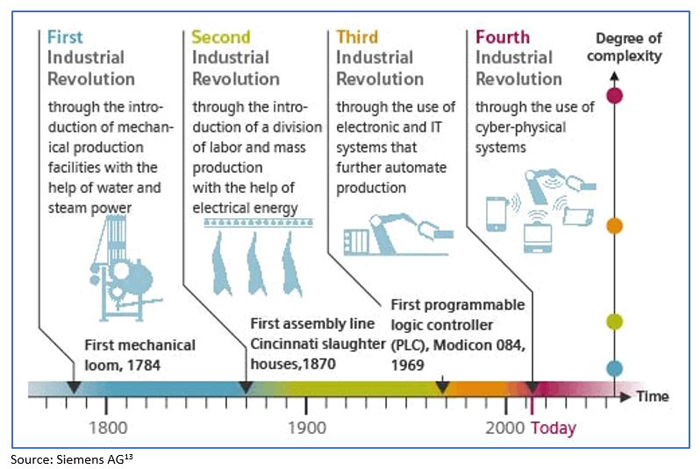

The phrase Fourth Industrial Revolution (or Industry 4.0) was brought to prominence in 2015 by Professor Klaus Schwab, founder and executive chairman of the World Economic Forum first in an article in Foreign Affairs, and again in his 2016 book.11 He describes the enormous potential for the technologies of the Fourth Industrial Revolution as well as the possible risks.

One of the greatest promises is the potential to improve the quality of life and raise the income levels for the world' s population as organizations and workplaces become more efficient and “smarter” when humans and machines work hand in hand. However, the risks are that Industry 4.0 could lead to a job market that is segregated into “low-skill/low–pay” and “high-skill/high–pay” segments, leading to the widening of economic and social gap and causing some jobs to become obsolete.12

While industrialization is not new and has been around throughout recent history, the figure below summarizes how each of the earlier three industrial revolutions are characterized as well as how the fourth one is shaping to be.

As industrialization progressed from harnessing water and steam power to mechanize production in the 1700s–1800s, to mass production of goods and services through electrical energy in the 1800s–1900s, to production automation using electronics and information technology capabilities from 1969 to early 2000s, one common theme among each phase is the advancement of technologies.

In that aspect, the fourth industrial revolution is no different from its predecessors. However, with billions of people connected by mobile devices with unprecedented processing power, storage capacity and access to knowledge, multiplied by emerging breakthrough in fields such as artificial intelligence, Internet of Things (IoT), autonomous vehicles, quantum computing and enabled by 5G and beyond, the largest beneficiaries of innovation tend to be the providers of intellectual & physical capital — the innovators, shareholders and investors.14 - Technology continues to outperform

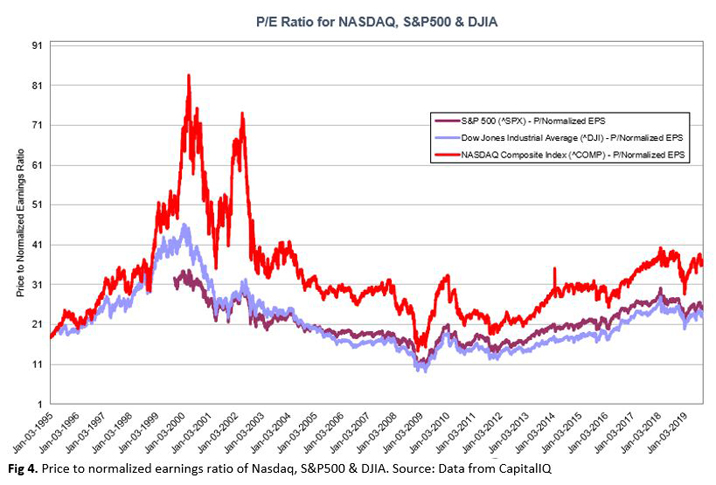

Given the above observation that the largest beneficiaries of innovation tend to be innovators, shareholders and investors, this could also be the reason why the technology–heavy NASDAQ Composite has outperformed the S&P 500 & Dow Jones Industrial Average across multiple time periods despite every boom and bust.

- Tech valuations have yet to hit levels seen during the dot-com era

Perhaps a sign of more rational exuberance rather than irrationality, price–to–earnings, a measure of whether valuations are cheap or expensive, of the technology–heavy NASDAQ Composite are currently hovering around the 30–40x range compared to the 50–80x range back in 1999 and 2000 before the dot–com bubble burst.

- Sound and profitable businesses will prevail and emerge stronger

Just like running any other businesses, technology companies that are well–run with strong fundamentals and value propositions will prevail even in challenging times. Amazon, Google, eBay ' Microsoft took the opportunity to consolidate their position when the going gets tough and came to dominate their respective fields.6 Hence it is important not to jump on the bandwagon and invest in every fad but pick potential winning stocks carefully.

If you believe that technology will continue to lead the future in the Fourth Industrial Revolution and want to be a part of it, yet don't know how to separate potential winners from losers, click here to find out more about our range of unit trusts within the tech sector or explore our full range of funds using our intuitive fund finder.

Finally, I leave you with a parting quote:

“Nothing important has ever been built without irrational exuberance” – You will need some of this mania to cause investors to open–up their pocketbooks and finance the building of railroads or the automobile or aerospace industry or whatever. And in this case, much of the capital invested was lost, but also much of it was invested in a very high throughput backbone for the Internet, and lots of software that works, and databases and server structure. All that stuff has allowed what we have today, which has changed all our lives... that's what all this speculative mania built.6

— Friend of Fred Wilson, Venture Capitalist, on the dot-com bubble

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 20/09/2019.

-

1 https://en.wikipedia.org/wiki/IPhone_(1st_generation)

3 https://techjury.net/stats-about/smartphone-usage/

4 https://www.kleinerperkins.com/perspectives/2016-internet-trends-report/

6 https://en.wikipedia.org/wiki/Dot-com_bubble

7 https://fred.stlouisfed.org/

8 https://www.computerworld.com/article/3412337/biggest-technology-ipos-2019-so-far.html

9 http://techgenix.com/biggest-tech-ipos/