|

Are Asian Investment Grade bonds set for a bull run in the Year of the Ox? By PineBridge Investments 2 March 2021

Asian investment grade (IG) bonds performed well in 2020, with the JACI Investment Grade Total Return Index rising nearly 7%1, thanks largely to strong credit fundamentals that allowed the asset class to remain resilient through the pandemic. As the Covid-19 recovery in Asia picks up momentum, will Asian IG bonds rise even higher this year?

After a surprisingly strong 2020 for the asset class, are Asian IG bonds still attractive? Arthur Lau (AL): The year started on a risk-on tone as investors reacted to the “blue sweep” in the US as the Democratic Party effectively gained control over both the US House of Representatives and Senate, which is seen as crucial for President Biden’s policy agenda. Yields on 10-year US Treasuries rose in January. Credit spreads tightened as investors continued to demand yield assets, driving interest in Asian fixed income.

Asian IG still offers higher yield with lower duration than peers

Source: Bloomberg, PineBridge Investments. Asian IG is represented by JACI Investment Grade, US IG by the Bloomberg Barclays US Credit Index and Global Agg Credit IG: Bloomberg Barclays Global Aggregate Index. For illustrative purposes only. We are not soliciting or recommending any action based on this material. Past performance is not indicative of future results. We are not soliciting or recommending any action based on this material. Yield refers to the return an investor would expect from a bond. Duration represents the interest rate sensitivity of a bond.

Omar Slim (OS): Broadly speaking, economic fundamentals in Asia are stronger compared to other markets due to better Covid-19 containment efforts, and this should offer a strong anchor for the region’s recovery. China was the only major economy to grow last year.3 We expect a broad economic recovery to take shape this year, not only in China but also in Singapore, South Korea, and Thailand for instance. In terms of credit metrics, corporate net leverage has remained relatively low compared to US, Latin American, and other emerging markets issuers, while interest coverage ranked highest relative to these three regions.4

Asia credit spreads still have room

Source: JP Morgan, Bloomberg, PineBridge Investments, as of 19 January 2021. Asia IG Credit Spread represented by JACI Investment Grade Index. For illustrative purposes only. Any opinions, projections, forecasts, or forward-looking statements presented are valid only as of the date indicated and are subject to change. We are not soliciting or recommending any action based on this material.

How are you currently positioned in the Asian IG market? OS: Our positioning reflects our view of more returns dispersion this year. This will be driven by the diverging economic prospects within Asian countries as well as different outlooks for segments and idiosyncratic issuer risks. As 2021 began, we’re overweight issuers from Singapore, Japan, and Australia relative to the benchmark. In Singapore for instance, with unemployment rate declining consistently and the smooth rollout of vaccines, we expect a strong, albeit uneven, recovery for the year. With regards to our sector allocation, we have a smaller allocation to sovereign issuers, preferring instead corporates as demand recovers. More specifically, we like the financial and government-related sectors and avoid Covid-19 impacted sectors. Within financials, we are overweight non-bank financial institutions which present more interesting valuations and steady fundamentals.

It is important to note that our positioning distills our investment process, which simultaneously analyzes fundamentals, valuations, and technical factors.

What potential risks are you watching out for? OS: The dominant theme for this year will remain the pandemic impact on economic growth and credit metrics. More tangibly, the risks are centered around the success of the Covid-19 containment efforts, including medical breakthroughs and vaccines deployment.

We also continue to monitor closely US-China relations under the Biden administration, which we expect to remain competitive, as mentioned earlier by Arthur. We are particularly cautious on duration risk as the recovery strengthens and US Treasury issuance increases. As always, we remained focused on monitoring individual issuers’ credit risks as well as environmental, social and governance (ESG) factors that could be material to an issuer’s credit worthiness.

Last year, the Asian bond market saw a wave of sovereign downgrades and corporate defaults. What is the outlook for downgrades and defaults this year? AL: We believe sovereign credit outlook will remain stable this year. As the Covid-19 recovery broadens across the region, it should be constructive for both sovereigns and corporates.

What are your expectations for US-China trade relations under President Biden? AL: In our base case, we don’t think US trade policy on China under the Biden administration will substantially change. In the near term, it is likely to be status quo. We do not expect any rollback of the tariffs already imposed. We also don't think there will be a substantial scaling back of restrictions on China’s information technology and technology, media and telecom (TMT) activities. The future of the ‘Phase One’ deal signed last year remains to be seen. China has fallen behind on its agreed purchases of US exports last year largely due to the pandemic.

We think President Biden will be more multilateral in his approach, working with allies to form a China strategy, which, arguably, may be more effective. Nevertheless, we continue to keep a close eye on US-China trade policy and its potential impact on the fixed income market.

As a seasoned Asia fixed income investor, what do you think are the key pillars to successful investing in Asian IG?

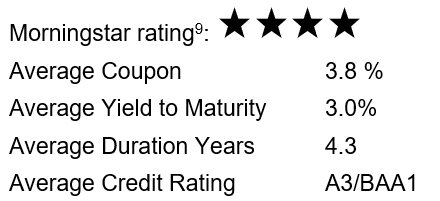

The PineBridge Asia Pacific Investment Grade Bond Fund, co-managed by Arthur Lau, CFA; Omar Slim, CFA; and Andy Suen, CFA, offers pure exposure to investment grade debt securities. The Fund has historically delivered better return/risk profile than peer average, with higher returns for lower risk over the three-year period ending 31 January 2021.8

Fund Snapshot

Source: PineBridge Investments, 31 December 2020. Fund performance is reflective of Share Class Y. For illustrative purposes only. We are not soliciting or recommending any action based on this material. For explanation of technical terms, please visit the individual fund page at pinebridge.com.sg.

Learn more about the Fund and how it can help your portfolio, visit pinebridge.com.sg.

YOU MAY ALSO LIKE THIS

Sources 1 JP Morgan, as of 31 December 2020. 2 As of 31 December 2020. 3 IMF, PineBridge calculations as of January 2021. 4 BAML, PineBridge Investments, as of 30 June 2020. Any opinions are valid only as of the date indicated and are subject to change. For illustrative purposes only. We are not soliciting or recommending any action based on this material. 5 Ministry of Manpower, as of 28 January 2021. 6 Moody’s, PineBridge Investments. As of 30 June 2020. Any opinions, forecasts and forward-looking statements presented above are valid only as of the date indicated and are subject to change. 7 JP Morgan, PineBridge Investments. Reported as of January 2021. Any opinions, forecasts and forward-looking statements presented above are valid only as of the date indicated and are subject to change. 8 Morningstar, as of 31 January 2021. Fund performance is reflective of Share Class Y. Peers refers to the average of all funds under the Morningstar category Asia Bond. The index is JPM Asia Credit TR USD. Risk is measured as standard deviation, which is a basic measure of the fund risk, i.e. the volatility of the fund’s returns in relation to its average. The higher the standard deviation, the more volatile the fund’s returns. The Fund’s total return is 6.09% vs 4.57% for peers. The Fund’s standard deviation is 5.17% vs. 6.68% for peers. Past performance is not indicative of future results. 9 Morningstar Rating™ Source: Morningstar Essentials™ as of 31 December 2020. Copyright © 2020 Morningstar, Inc. All Rights Reserved. Morningstar Rating in the ASIA BOND Morningstar Category. Morningstar Performance ratings shown reflect the share class performance shown unless noted otherwise on this material. Third-party rankings from rating publications are no guarantee of future investment success. Working with a highly rated advisor does not ensure that a client or prospective client will experience a higher level of performance or results.

PineBridge Asia Pacific Investment Grade Bond Fund Endnotes PineBridge Investments (‘PineBridge’) is a group of international companies acquired by Pacific Century Group from American international Group, Inc. in March 2010. PineBridge companies provide investment advice and market asset management products and services to clients around the world.

PineBridge Investments is a registered trademark proprietary to PineBridge Investments IP Holding Company Limited. Services and products are provided by one or more affiliates of PineBridge however certain incidental middle and back office services may be outsourced to 3rd parties.

PineBridge Asia Pacific Investment Grade Bond Fund is a sub-fund of PineBridge Global Funds, an Irish domiciled UCITS umbrella fund, authorised and regulated by the Central Bank of Ireland. The Fund Managers are PineBridge Investments Asia Limited and PineBridge Investments Singapore Limited.

The inception date of Class Y of the Fund was 8th of February 2017.

Where performance is presented herein it is representative of Class ‘Y’ in U.S. dollars.

The performance of the Sub-Fund’s portfolio of investments will be measured against JP Morgan Asia Credit Index (JACI) Investment Grade Total Return (the “Index”). The Index is a traditional, market capitalization weighted index; which includes bonds issued by Asia based sovereigns, quasi-sovereigns, and corporates.

Any performance presented is historical, assumes reinvestment of all interest, dividends and capital gains, and is not indicative of future results. Investment return and principal value of an account will fluctuate, and there can be no assurances that losses will not be incurred.

Rates of return and asset valuations, if shown, are in U.S. dollars, unless otherwise stated and are computed using a time-weighted rate of return. Any performance results for periods of less than one year are not annualized. Income is included net of irrecoverable withholding tax deducted at source in accordance with the domicile of the underlying portfolios. Portfolios are valued on a trade date basis.

Where gross performance returns are quoted, they are presented net of transaction costs and before the deduction of management fees and all operating costs (which include custodian and administration fees).

Where net performance returns are quoted, they are presented net of transaction costs and net of the deduction of management fees and all operating costs (which include custodian and administration fees). These fees reduce a client's return.

Fund fees and expenses are described in PineBridge Global Fund’s offering documentation, which is available upon request.

Past performance may not be a reliable guide to future performance. The value of units and the income from them may fluctuate.

Copies of PineBridge Global Fund’s Prospectus, the Key Investor Information Documents (KIID), and the most recent financial statements, which include risk factors and terms and conditions and which should be read before investing, may be obtained free of charge in Ireland from PineBridge Investments Ireland Limited, and in Germany from BHF-BANK AG, Bockenheimer Landstraße 10, 60323 Frankfurt. The KIID is also available from http://www.pinebridge.com.sg.

In Switzerland, the Prospectus, the Key Investor Information Document (KIID), the Trust Deed as well as the annual and semi-annual reports of the Fund may be obtained free of charge on the homepage of the management company or from the Swiss Representative. The Representative and Paying Agent of the Fund for Switzerland is State Street Bank International GmbH Munich, Zurich Branch, Beethovenstrasse 19, 8027 Zurich.

The information presented relates to an account that is subject to laws and regulations that may be different from those applicable to an account for an investor in a different jurisdiction. Therefore, results may differ materially due to different investment limitations, regulatory environments and portfolio compositions.

The Fund is authorised for public distribution in Austria, Denmark, Finland, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Singapore, Sweden, Switzerland and the United Kingdom.

The units of the Fund may not be offered, sold or delivered in the United States or to or for the account of U.S. Persons.

This material is issued by: PineBridge Investments Ireland Limited, 4th Floor, The Observatory Building, 7-11 Sir John Rogerson’s Quay, Dublin 2, Ireland.

Last updated as of 23rd October 2020.

PineBridge Investment Singapore Limited's Disclaimer

Past performance may not be a reliable guide to future performance. Investment involves risks including the possible loss of principal amount invested. The value of the units in the Fund and the income accruing to the units, if any, may fall or rise. The Fund may use or invest in financial derivatives for efficient portfolio management and hedging purposes. PineBridge Asia Pacific Investment Grade Bond Fund (the “Fund”) is a sub-fund of PineBridge Global Funds, an Irish domiciled UCITS umbrella fund, authorized and regulated by the Central Bank of Ireland and registered as a recognised scheme under the Securities and Futures Act (Cap 289) in Singapore. The manager of the Fund, PineBridge Investments Ireland Limited (the “Manager”), has appointed PineBridge Investments Singapore Limited (“PBIS”) as its representative in Singapore. We are not soliciting or recommending any action based on this material. Investors should seek professional advice, and read the prospectus and the product highlights sheet, available from PBIS or any of its appointed distributors, for further details including the risk factors, before investing. This is not intended to be a recommendation to buy or sell a security or an indication of the holdings of any portfolio or an indication of performance for the subject company/issuer.

The information presented herein is for illustrative purposes only and should not be considered reflective of any particular security, strategy, or investment product. It represents a general assessment of the markets at a specific time and is not a guarantee of future performance results or market movement. Any views express represent the opinion of the manager and are subject to change. Views may be based on third-party data that has not been independently verified. PineBridge Investments does not approve of or endorse any re-publication or sharing of this material. In Singapore, this document is issued by PineBridge Investments Singapore Limited (Company Reg. No. 199602054E), licensed and regulated by the Monetary Authority of Singapore (MAS). This advertisement or publication has not been reviewed by the MAS. Investors should note that the website www.pinebridge.com.sg and any other website (including any contents therein) referred to in this document have not been reviewed or endorsed by the MAS. |