Three reasons to get active

This story was published on 23 April 2018 by Allianz Global Investors

Summary

Active managers outperformed their passive peers during the two most recent major market downturns – a key consideration as today's abnormally long cycle winds down. Moreover, passive investments can be less liquid in volatile markets, and reduced central-bank stimulus could mean lower correlations.

Key takeaways

- During the tech-market bust and great financial crisis, US large-cap active managers outperformed their passive peers – food for thought as today’s abnormally long market cycle may be drawing to a close

- Passive investors expect to be able to shift positions quickly, but volatile markets don’t always offer enough liquidity to trade efficiently – and volatility has recently risen sharply

- Easy money from central banks resulted in market distortions that inordinately benefited passive strategies – but this environment won’t last forever

It is well-known that the active management industry has recently encountered its share of challenges. In the US in 2016, USD 500 billion moved into passively managed index funds, while USD 340 billion exited actively managed funds. While there is no guarantee that actively managed strategies will outperform the broader market, we believe this shift from active to passive is misguided for three key reasons.

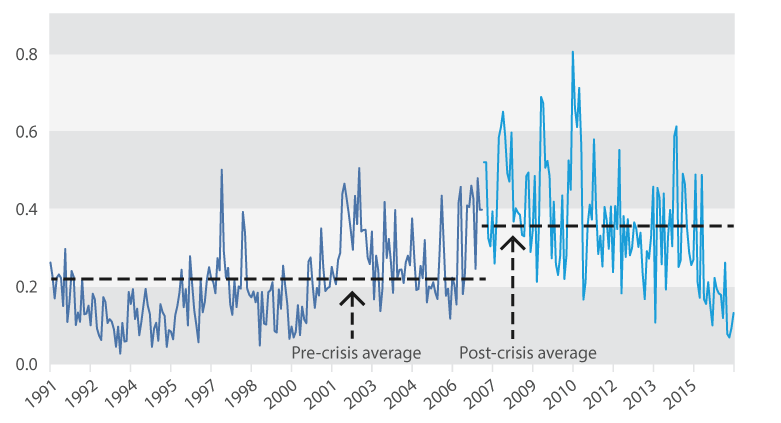

Stock correlations nearly doubled after the financial crisis

S&P 500 Index; January 1991 through December 2017

Source: FactSet, AllianzGI Economics & Strategy. Data as at 31 December 2017.

There is no guarantee that actively managed investments will outperform the broader market.

Sources for study of US large-cap active managers: Morningstar, S&P 500 Index, Allianz Global Investors. Data as at 31 December 2017. Allianz Global Investors created the "Active Large Cap Blend" category by including only those Morningstar "Large Blend" category constituents that are not defined by Morningstar as index funds. Institutional share classes only. Excess return relative to S&P 500 Index, calculated monthly. Net of fees.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted. This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan];and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

Information is correct as of 11/07/2018.

Over a full cycle, active managers have done well

First, the fair evaluation of any investment strategy should cover a full market cycle. A 2012 study from Robert Baird shows that while 59 per cent of active managers added value over one year, 73 per cent did so over five-year periods. This carries particular resonance today because of how abnormally long the current market cycle has become: Despite the recent sell-off, the S&P 500 Index hasn’t seen a bear market since the financial crisis ended more than nine years ago.

This means that since the market troughed in March 2009, one key area where active managers have proven expertise – providing downside protection – has been in less demand because of the rising tide that lifted most risky assets simultaneously.

Yet when the markets have not performed as well – such as during the 2000-2002 tech-market bust and the 2008-2009 financial crisis – our research shows that US large-cap active managers outperformed their passive peers by 471 basis points and 100 basis points, respectively.

One of the tools that helps active managers navigate storms before they strike is their ability to analyse corporate fundamentals of the securities they own. When volatility rises, active managers can underweight underperforming assets, or they can simply move money into cash. Passive vehicles, on the other hand, are at a disadvantage when markets get rocky: they not only fall in lockstep with the index being tracked, but there is a risk they will underperform after accounting for fees.

Poor understanding of passive strategies can be problematic

Second, the shift toward passive is troubling because of how passive instruments are deployed. Frequently, passive investors buy index funds for tactical rather than strategic reasons, meaning they expect to move in and out of positions quickly. But when markets get volatile, there isn’t always enough liquidity to trade efficiently.

A prime example of this problem can be seen in the “flash crash” of 24 August 2015, when the Dow Jones Industrial Average briefly plunged nearly 1,000 points. Circuit breakers (trading halts) were triggered almost 1,300 times, and the prices of some popular exchange traded funds (ETFs) disconnected from their underlying assets. One US consumer staples ETF lost 32 per cent of its value even though the companies it owned were down only 9 per cent.

These types of trading risks may extend well-beyond “plain-vanilla” equity ETFs. According to a March 2018 Wall Street Journal article, some popular bond ETFs have grown more attractive to short-sellers due to questions about the funds’ ability to process redemptions when markets turn.

When investing in passive instruments, it is vital to look beyond the focus on low-cost fees and tactical trading to understand the intrinsic characteristics of these products. Take volatility ETFs, for example. Long-volatility ETFs are designed to lose money if held over the long-run because they must constantly buy expensive longer-dated options contracts while selling less-expensive shorter-dated contracts.

And while short-volatility ETFs can benefit from the same dynamic, their investors can get wiped out when volatility spikes. In fact, many “new-era” passive investment products – for instance, active ETFs and smart-beta ETFs – have neither an extensive track record nor a broad asset base. This means they may not behave as expected when market conditions shift.

If recent experience tells us anything about passive investing, it is that understanding your investment is critical. Poorly timed tactical trades in supposedly highly liquid vehicles may result in outsize losses.

Passive investing benefited from central-bank stimulus, which is now unwinding

Third, passive managers have benefited from years of unprecedented monetary stimulus from central banks. After the last financial crisis, the world’s major central banks lowered interest rates to record-low, sometimes even negative territory. They also launched asset-purchase programs such as “quantitative easing” that stimulated markets even more. These efforts pushed up asset classes’ correlations – the tendency to move in lockstep with one another.

The reason this is important is that when correlations are low, stocks tend to rise or fall based on their company-specific characteristics. Corporate fundamentals and the valuable work that active managers do – sifting through balance sheets, income statements, pay-out ratios and more – have the potential to make a real difference. But when correlations are high, stocks tend to go up and down at the same time.

From this standpoint, it is encouraging to see correlations returning to normal as major central banks normalize monetary policy – a natural part of the economic cycle. The Federal Reserve is raising interest rates and unwinding its balance sheet, European Central Bank officials are tapering QE and the Bank of Japan is buying fewer assets through its “yield curve control” programme.

We think their combined efforts mean global central-bank liquidity could reach its peak in 2018 and correlations are likely to continue falling – one more reason for investors to get, and stay, active.