Additional property cooling measures = End of financial freedom?

Despite having one of the highest per capita income and lowest personal income tax rates in the world, Singapore is also consistently ranked among the top in terms of home and car prices. It is no surprise then that Financial Freedom has become such an elusive term for most young Singaporeans.

Many have witnessed their parents' or grandparents' generation turn into millionaires or multi-millionaires (at least on paper) from the Singapore growth story through exponential returns on their residential or investment property, further ingraining the strong Asian obsession for real estate investing. However, given the Singapore government's determination to manage excessive exuberance in the real estate sector, the dream of owning multiple properties and having tremendous gains may now be just a distant reality.

Where then, should investors turn to if they want to build a steady stream of passive income?

The answer may lie in dividend-paying unit trusts.

In the vast universe of unit trust offerings, dividend-paying income funds are still the preferred choice for yield-seeking Asian investors. Ask any seasoned investor with a diversified dividend portfolio why they prefer to invest in dividend-paying funds, and more often than not, the most common answer you will get is:

"I'm not too concerned about market volatility as long as I continue to receive a decent dividend. In the long run, the dividends that I receive will likely compensate for short term market fluctuation"

The average holding period of income investors are much longer than growth investors, typically ranging from 5-7 years compared to the 1-3 years holding period of growth investors. Over a longer time horizon, overall portfolio returns of income-seeking investors tend to outperform their growth-seeking peers purely due to the longer duration in the market.

At dollarDEX, we have over 250 dividend-paying funds and the dividend yields of these funds range from a nominal 0.08% per annum to as high as 10.3% per annum. Investors can also choose funds with various distribution periods, be it monthly, quarterly, semi-annually or annually. Additionally, there are also many asset classes and sectors to choose from depending on their preference.

With so many choices available, what should you as an income investor look out for to narrow the search criteria?

In addition to the usual criteria for selecting unit trusts (understanding your risk profile, long term track record, fund manager strategy, currency denomination etc), do also pay attention to the following:

1. Distribution frequency

Similar to dividend stocks and REITs, many income funds also pay out dividends on an annual or semi-annual basis. Increasingly, due to the huge popularity of income funds amongst Asian investors, many more fund managers are starting to distribute dividends on a monthly or quarterly basis. This is a huge advantage especially if you are trying to build your passive income stream to supplement or eventually replace your active earned income.

2. Yield

The higher the dividend yield the better, right?

Not necessarily. If the dividend yield is exceptionally high such that the fund manager is unable to generate yields higher than the fund's dividend policy, then the fund manager may have to resort to selling its underlying securities to raise cash for distribution. This inadvertently affects the Net Asset Value (NAV) and if this persists for a prolonged period of time, the NAV of the fund will be drastically affected. At times, this may also cause the fund manager to take drastic measures such as reducing the dividend payout ratio.

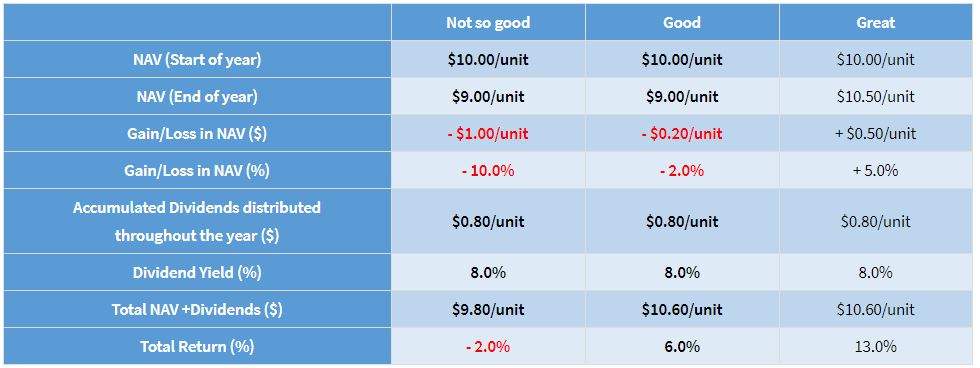

3. Total return

For the uninitiated, total return for fund performance as the name suggests, is the total gain in the portfolio value of the fund including dividends distributed. A good dividend fund is one that consistently achieves total return for the investor regardless of economic environment while a great fund is one that is able to generate growth in NAV even with a high level of income distribution.

Here is an illustration for reference:

4. Portfolio allocation

While it may be tempting to allocate a substantial portion of your investments into a high-income fund, another important thing to note when building your dividend portfolio is to consider the asset allocation or portfolio composition to ensure that you are well diversified across various asset classes and across various markets.

A good number of funds to hold is between 5-7 with exposure in both bonds and equities, as well as in various geographical regions such as Global, Asia, Emerging Markets, Singapore, US, Europe etc.

Another alternative to a DIY portfolio allocation is to simply select 2-3 Global Multi-Asset Income funds (GMAI) and let the fund managers do the asset allocation.

In your pursuit for financial freedom, it is important to diversify your income sources by having multiple income streams from various sources such as property, blue chips stocks, REITs, unit trust, CPF & insurance retirement plans.

Check out our Fund Finder to start searching for funds to allocate for your portfolio.

Happy investing!

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 04/09/2018.