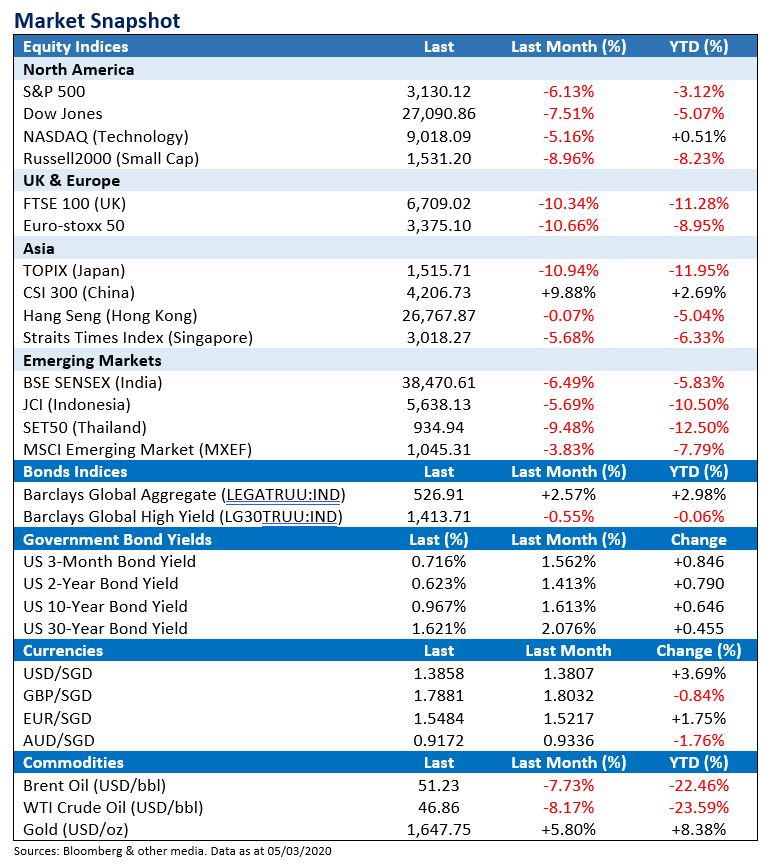

March 2020 Market Update

Fears of the spread of the coronavirus and its impact on the world economy continues to grip financial markets around the world with global indices testing correction territories. What has initially been thought of as an Asian epidemic has now evolved into almost a global pandemic.

The VIX index, also known as the volatility or fear index, spiked to a high of 40.11 on 28th February – a level not seen in almost a decade. (the last time the VIX crossed the 40.0 level was in August 2011 on Black Monday due to the European Debt Crisis)

With governments and central banks worldwide acting to contain the virus and to provide stimulus to tame the markets, is this a bottom–fishing opportunity or has the worst yet to come?

Central Banks & policy tools

Given the potential impacts of COVID–19 on global growth, G7 finance ministers and central bank governors acknowledged the need for swift policy actions and reaffirm their commitment to use all appropriate policy tools to achieve strong, sustainable growth and safeguard against downside risks, and to stand ready to provide a more forceful, coordinated response if conditions require it.1

IMF & World Bank – The International Monetary Fund (IMF) is making available about US$50 billion for low-income and emerging market countries while the World Bank will provide an initial package of up to US$12 billion to assist countries coping with the health and economic impacts of the COVID–19 outbreak.1

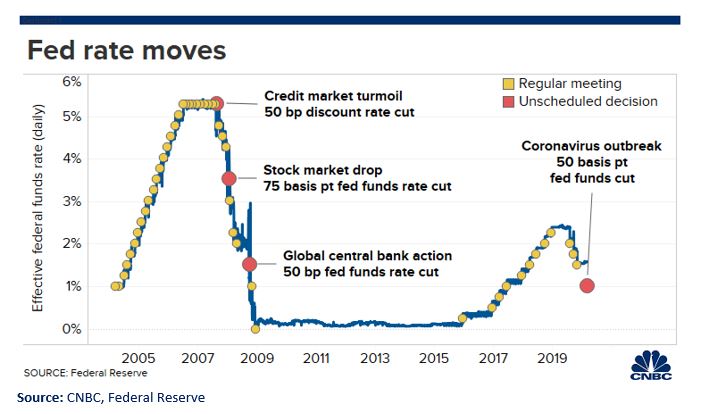

U.S Federal Reserve – On 3rd March, the Federal Reserve made an emergency cut in interest rates by half a percentage point to a target range between 1%–1.25% after officials saw the coronavirus as having a material impact on the economic outlook. Fed Chairman Jerome Powell also indicated that the Fed will continue to watch the coronavirus spread and would adjust policy accordingly, though responses would come in the form of rate cuts rather than additional asset purchases, or quantitative easing.2

Reserve Bank of Australia – The RBA has cut official interest rate to a new record low of 0.5% due to the “significant effect” of coronavirus outbreak on the Australian economy and signalled it is prepared to cut further if needed. The outbreak has already hammered industries including tourism, education and mining that are heavily dependent on exports to China.3

Major central banks have also scheduled meeting in the coming weeks including the European Central Bank (ECB), Bank of Japan (BoJ) and Bank of England and the possible moves might include further rate cuts, with the BoJ and ECB deeper into negative territory.4

However, investors and economists are concerned that there is not much monetary policy can do to save the global economy, especially when some major central banks – such as the ECB and BoJ – have already cut interest rates into negative territory. Even China has much less ammunition than the last time they had to launch a stimulus package, and central banks around the world may find themselves required to act forcefully in the weeks ahead should conditions deteriorate further.4

United States

Biden "relief rally"? – After losing nearly 800 points on 3rd March despite an emergency interest rate cut from the Fed, the Dow Jones Industrial Average rose nearly 1,200 points the next day fuelled by former Vice President Joe Biden's lead in the Democratic primary and ahead of Bernie Sanders, soothing some of Wall Street's fears about Sander's anti–capitalist policy proposals, which includes higher taxes on the wealthy, breaking up big banks and a $15 an hour minimum wage.5

Mohamed El–Erian, chief economic advisor at Allianz, cautioned that the Fed will not be able to stop the financial markets from freezing amid economic fallout from the coronavirus outbreak as it's not going to encourage people to travel or to encourage people in China to go back to work. Instead, let economics and natural dynamics play out before the market is attractive enough for the sort of risk that is ahead.10

Echoing Erian's views, Boris Schlossberg, co–founder of BKForex.com expects the decline in earnings estimates is going to continue and be much worst than people think. In a best-case scenario, it's a two–quarter decline in earnings as markets stabilize, then to get the supply chain back up, and then getting demand back up. He thinks that people are clearly underestimating the long–term impact of all these problems.6

China

The Chinese manufacturing economy was impacted by the epidemic last month with the Caixin/Markit Manufacturing Purchasing Manager's Index (PMI) showing the lowest on record of 40.3 for the month of February, way below economists' expectation of 45.7 and a sharp dip from January's reading at 51.1.7

PMI readings above 50 indicate expansion, while those below that level signal contraction.

While some economists expects a strong rebound from the second quarter of 2020 going into the second half of the year, others are concerned that with the jump in virus cases overseas, there is a growing risk of a protracted downturn in foreign demand, dampening the likelihood of a quick V–shaped recovery in the coming months.7

Europe

A sudden spike in the number of coronavirus cases in Italy has prompted officials to close schools in Milan, cancelled the Venice Carnival and most other public events and museums. The problem for Europe is that because Italy is a member of the Schengen Agreement, which allows free movement of people between most European countries, Italy and its neighbours have no permanent border controls. Thus, there is concern that COVID–19 could spread rapidly across Europe if it is not contained in Italy, and the imposition of border controls would be hugely disruptive to the European economy.8

Further, the intensification of the civil war in Syria has boosted the likelihood of a flood of refugees from the Middle East to Europe. There is concern that given the surge in cases in Iran and given the unsanitary conditions that refugees face, the risk of the virus spreading has increased.8

Unlike China, democratic nations in Europe or United States might have more difficulty imposing draconian restrictions on movement. While there is certainty that economies will bounce back quickly after the virus, there is no certainty that the worst is over.8

Asia

The ASEAN+3 Macroeconomic Research Office (AMRO) estimates that the COVID–19 epidemic could deduct as much as half a percentage point from the economic growth of some regional economies in 2020. Given the size of China's economy, a slowdown there will spill over to the rest of the ASEAN+3 economic bloc, which comprises the 10–member state of ASEAN as well as China, Japan and South Korea.9

The most immediate impact on the region has been the disruption to travel, tourism and related industries which has significantly increased since the SARS outbreak in 2002–2003 as the region became much more dependent on Chinese tourism.9

The manufacturing sector has also been disrupted, with domestic demand in surrounding countries taking a hit. Many regional economies such as Singapore and Vietnam are deeply integrated within regional and global supply chains and China is an important link in these networks.9

However, trade and tourism are expected to rebound in line with China's demand once the epidemic recedes and the ASEAN+3 economies still have policy space to mitigate the impact and shore up growth.9

As you watch intently on how the impact of the coronavirus would unfold in the following weeks and months along with how your portfolio value would fluctuate with each positive and negative development, don't forget to stay calm and invested with dollarDEX. Over the long haul, the coronavirus situation will be a thing of the past.

If you are not confident of timing the market, one good way is to invest in smaller tranches or set up a Regular Savings Plan (RSP) on dollarDEX to smooth out the volatility and take the emotions out of investing. It is also important to have a diversified portfolio to avoid concentration risk in a particular sector or region.

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 11/03/2020.