Low rates are back, so where do you turn in fixed income?

13 Jun 2019

Summary

Investors who need income and return potential should consider an active, balanced, global approach. Consider pairing high–quality investment–grade corporates, Treasuries and select securitised assets with infrastructure debt and higher–quality US, European and Asian high–yield bonds.

Key takeaways

- Faced with low or even negative bond yields, many investors are looking to preserve income and return potential – and an active, holistic approach could help

- We see opportunities in the securitised fixed–income market and higher–quality corporate bonds, though investors should be cautious and selective with BBB exposure

- For additional income potential, look to higher–quality US high–yield bonds, select global high–yield bonds (particularly from Europe and Asia) and infrastructure debt

- Using these securities in a “barbell” approach can help investors take selective risks while providing the potential for favourable yields and returns

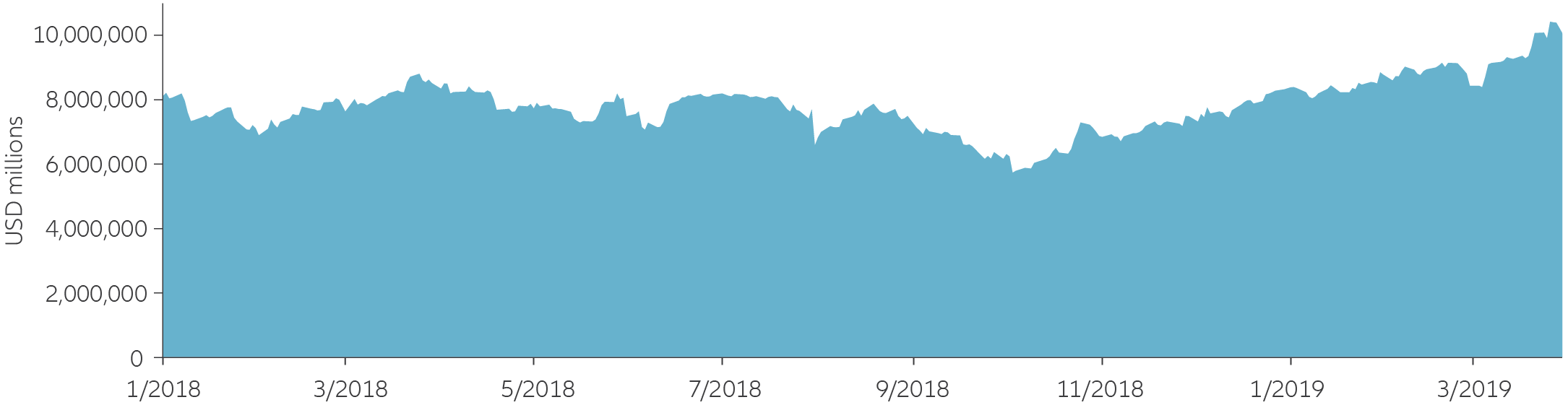

With global growth slowing and inflation still low, most major central banks have paused their plans for raising rates – and in some cases have even begun cutting them. This has pushed bond yields lower around the world. In fact, the amount of negative–yielding US dollar–denominated debt has risen to more than USD 10 trillion globally, as the chart below shows.

A record amount of debt now has negative yields

Bloomberg Barclays Global Aggregate Bond Index negative–yielding debt

Source: Bloomberg. Data as at 31 March 2019.

As a result, many investors once again are looking to preserve income and meet return expectations. We suggest taking a holistic, active approach to building fixed–income portfolios using a “barbell” approach – taking selective risks for higher income potential while using more defensive positions to balance overall risk. On one end of the barbell could be high–quality investment–grade corporates, Treasuries and select securitised assets. On the other could be BB rated US high–yield bonds, European and Asian high–yield bonds, and infrastructure debt.

In the investment–grade universe, look to higher–quality bonds

Among investment–grade securities, we see opportunities in higher-quality corporate bonds and the securitised fixed–income market.

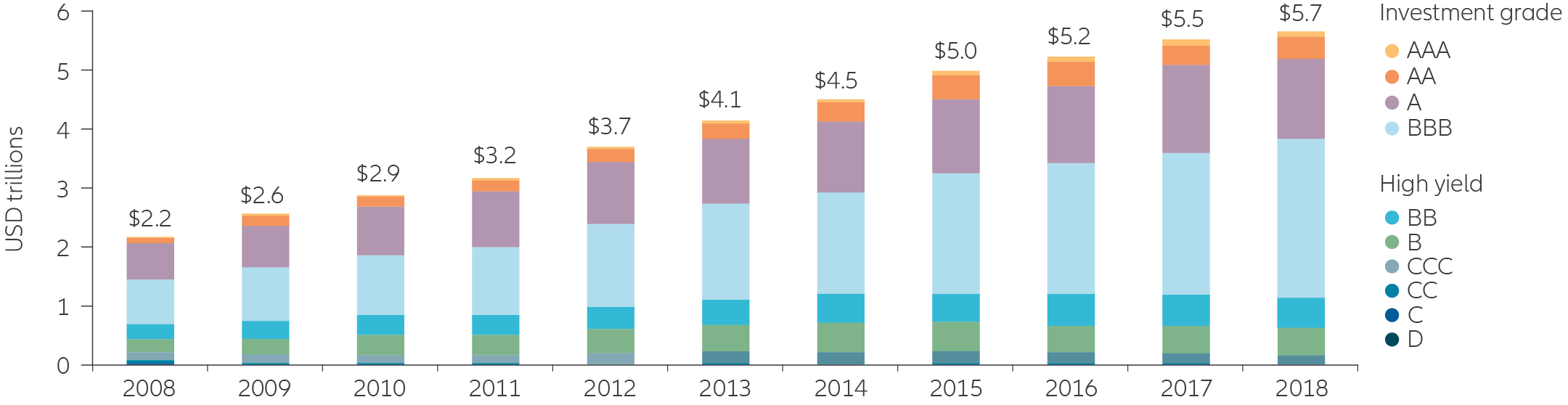

1. Look to higher–quality corporate bonds The US investment–grade bond market has doubled in size since the 2008 financial crisis, but overall credit quality has deteriorated. The landscape is increasingly dominated by assets with BBB ratings, as shown below; these are on the low end of the range that qualifies as investment–grade. As US economic growth slows and corporate earnings moderate, we suggest repositioning towards higher–rated securities, such as bonds rated A.

More investment–grade bonds have lower BBB ratings

Ratings of the US non–financial corporate–debt market

Source: Bloomberg. Data as at 31 December 2018. Calculated using ICE (Intercontinental Exchange) investment–grade and high–yield bond indexes, excluding the issues of financial firms, as at 31 December for each year shown.

Although there are specific areas of the BBB marketplace that look attractive, we believe investors should become increasingly selective and active in this space. The US economic cycle is now in a more mature phase, and low rates are once again tempting corporations to take on more debt. Consider focusing on issuers with:

- Credible plans to reduce their debt burdens (known as “de–leveraging”).

- Consistent free cash–flow levels, which can often be found in monopoly–like businesses with the ability to take on debt.

- Attractive subordinated–debt issues, which are riskier but can offer more attractive terms; look for issues from high–quality banks and utilities.

2. Consider securitised fixed–income assets One area of the investment–grade bond universe that offers attractive diversification opportunities is the securitised fixed–income market. These are pools of assets with cash flows that are divided and sold to investors, and they tend to be tied to what we view as more resilient economic sectors: consumers, residential housing and commercial real–estate. Among the more attractive opportunities are:

- High–quality asset–backed securities (ABS), such as AAA rated credit cards and prime auto, which tend to be liquid and can complement Treasury or cash holdings.

- More specialised areas of the ABS market such as franchise ABS, single–asset commercial mortgage–backed securities and non–agency mortgage bonds. These can help investors diversify their investment–grade bond holdings, and can be good alternatives to BBB rated corporate bonds.

For enhanced income potential, look for higher yields with higher quality

For investors in search of additional income and yield, we see opportunities in higher–quality US high–yield bonds, select global high–yield bonds and infrastructure debt.

-

1. Go higher quality in US high yield

Within what Moody's estimates to be a USD 1.2 trillion US high–yield marketplace, the highest–quality BB rated segment remains relatively attractive. These issuers have better credit profiles, tend to offer shorter–duration bonds and have higher yields than investment–grade securities. Our focus remains on companies with visible earnings streams and no imminent refinancing risks. As the economic cycle matures, US high–yield investors may have an opportunity to invest in “fallen angels” – BBB rated assets that have been downgraded to high–yield status. These corporations could improve their debt profiles and once again become investment–grade assets.

-

2. Explore high–yield issues in Europe and Asia

To diversify holdings and enhance yield potential, consider investing in global high–yield issues – particularly from Europe and Asia. Europe's substantial economic slowdown has made these bonds less expensive, and they are generally more conservatively positioned: nearly 73% of the market is BB rated versus 46% in the US, according to ICE. This has helped lower the default rates for European versus US high–yield issues, particularly during downturns. Asian high–yield bonds – especially US dollar–denominated ones – may also provide higher yields than their US counterparts. The Asian high–yield market is primarily dominated by Chinese companies, and we believe China's economic outlook is good thanks to its stabilising economy and the potential for a resolution to the US–China trade dispute.

-

3. Diversify with infrastructure debt

Infrastructure–debt investments – which are privately financed projects such as airports and water pipelines – are often highly regulated and can have predictable cash flows, longer maturities and lower loss rates than corporate bonds. While there may be liquidity constraints, their additional yield potential and lower correlations with equity and traditional fixed income can provide a valuable source of diversification. In addition, ESG (environmental, social and governance) investors can find synergies in infrastructure debt, since many of these projects focus on renewable energy, social infrastructure (such as universities, hospitals and schools), and conventional energy and utilities (such as waste– and water–treatment facilities).

Build your bond portfolio with a “barbell” approach

Although investors are facing low yields from government bonds globally, we see opportunities to invest actively across the fixed–income spectrum – particularly with a “barbell” approach that balances safer with riskier investments. On one end of the barbell could be high–quality investment–grade corporates, Treasuries and select securitised assets. On the other could be BB rated US high–yield bonds, European and Asian high–yield bonds, and infrastructure debt. Combined, this approach may be able to help investors take selective risks while providing the potential for favourable yields and returns.

YOU MAY ALSO LIKE

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Diversification does not ensure a profit or protect against a loss. Equities have tended to be volatile, and do not offer a fixed rate of return. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Foreign markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations.

This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Panama, Peru, and Uruguay.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG, licensed by FINMA (www.finma.ch) for distribution and by OAKBV (Oberaufsichtskommission berufliche Vorsorge) for asset management related to occupational pensions in Switzerland; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

841220

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 04/06/2019.