|

Finding the Sweet Spots in Asia High Yield Amid Market Noise By PineBridge Investments 7 Sep 2021

Asia high yield bonds offer plenty of value, especially for those able to position across credit ratings, sectors, and markets. Balancing yield and risk will be key to long- term growth and income generation, says PineBridge Investments’ Head of Asia ex Japan Fixed Income Arthur Lau.

Asia high yield has become an important component of the global emerging markets high yield market, driven by prolific capital raising by Chinese enterprises in recent years. New issuances rose in first half of the year compared to the same period a year ago, despite a slowdown in issuances by Chinese property issuers amid deleveraging efforts.

While concerns have risen over defaults in the Chinese property sector, Arthur Lau, CFA, Head of Asia ex Japan Fixed Income at PineBridge Investments, says Asia high yield bonds, as a whole, remain a compelling investment on the back of strong fundamentals, but investors should exercise selectivity.

“Asia high yield offers a compelling combination of the highest yield and the shortest duration among global peers. The region’s growth trajectory is much stronger than developed markets, and we expect the growth rate to outpace developed markets in the next two years, which bodes well for the corporate sector,” he explains.

“The key to investing in this market is doing your homework in researching and understanding the risk/return profile of issuers to find the ‘sweet spots’ in the market and build a resilient portfolio that can ride out short-term volatility.”

Four reasons to invest Lau offers four reasons why investors should consider Asia high yield for their portfolios today.

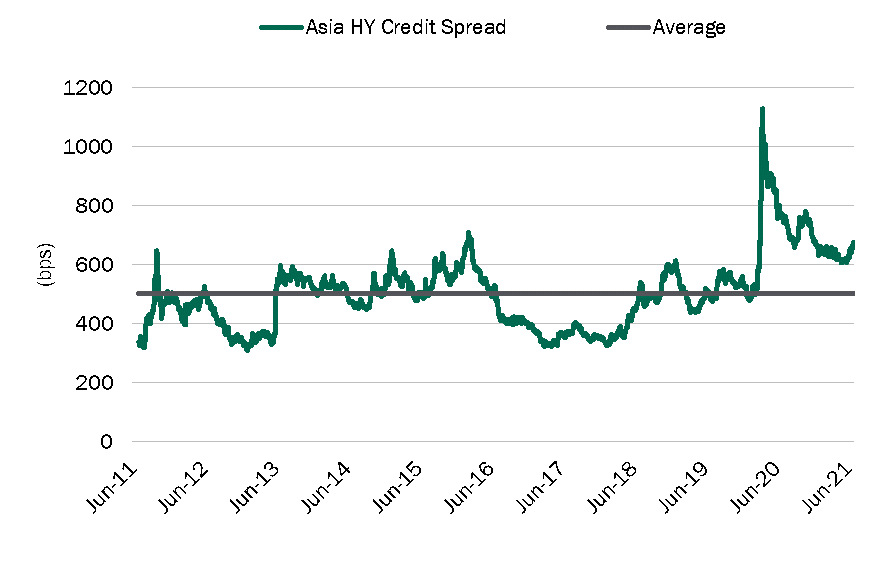

Source: J.P. Morgan, Bloomberg, PineBridge Investments as of 30 June 2021. Asia HY Credit Spread is represented by the JACI Non-Investment Grade Index. For illustrative purposes only. Any opinions, projections, forecasts, or forward-looking statements presented are valid only as of the date indicated and are subject to change. We are not soliciting or recommending any action based on this material.

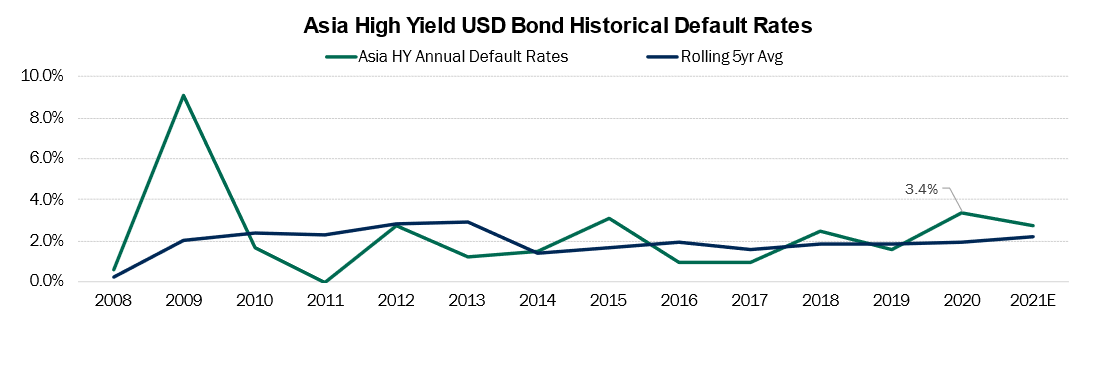

Source: J.P. Morgan, PineBridge Investments as of 14 April 2021. For illustrative purposes only. We are not soliciting or recommending any action based on this material. Any opinions, projections, forecasts, or forward-looking statements presented are valid only as of the date indicated and are subject to change.

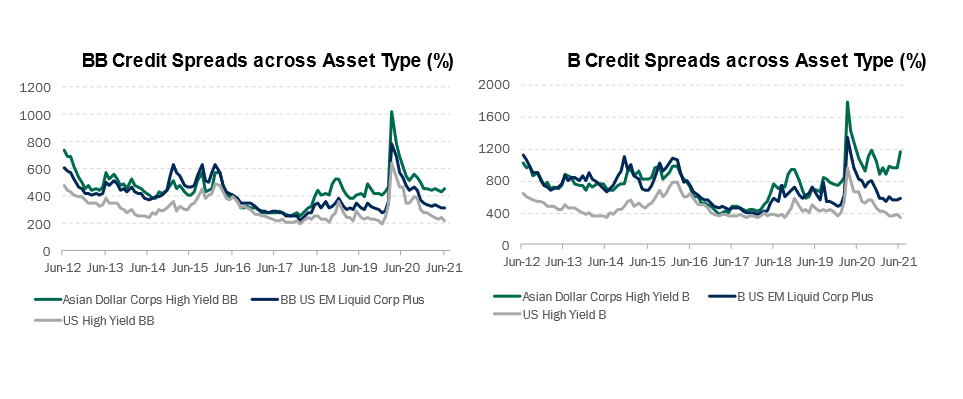

Selective Opportunities in Asia HY

Source: BofA Merrill Lynch, PineBridge as of 30 June 2021. For illustrative purposes only. Any opinions, projections, forecasts, or forward-looking statements presented are valid only as of the date indicated and are subject to change. We are not soliciting or recommending any action based on this material. Past performance, or any prediction, projection or forecast, is not indicative of future performance. *Credit spread is the difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality.

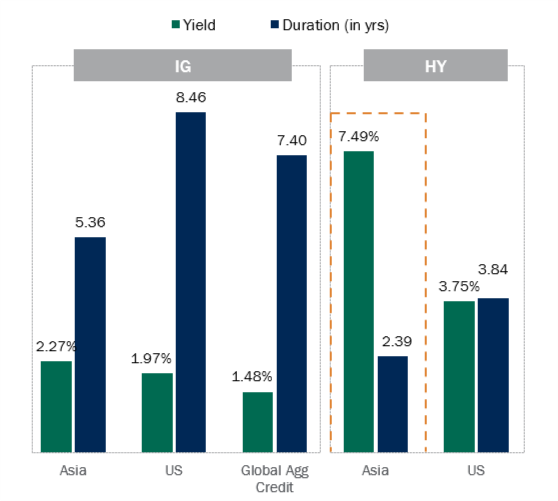

Source: Bloomberg, PineBridge Investments as of 30 June 2021. Any opinions, projections, forecasts, or forward-looking statements presented are valid only as of the date indicated and are subject to change. We are not soliciting or recommending any action based on this material. Duration is a measure of the bond’s sensitivity to changes in interest rates. Yield refers to the rate of return if bonds are held to maturity. The rate of return includes the coupon payments received during the term of a bond and its principal repayment upon maturity.

Active credit selection to stay ahead of the curve Managing risk is key to high yield investing, as lower-rated bonds tend to suffer in slow-growth and recessionary environments and during periods of heightened volatility. Active credit selection allows managers to position across sectors, markets, and credit ratings, and thoroughly focus on issuer fundamentals as well as sector and macro cycles. Lau says the nonfinancial aspects of the issuer such as environmental, social, and governance (ESG) performance are just as important as financial metrics.

“A substantial portion of Asia high yield bonds are issued by unlisted companies. Accessing information on these issuers may be challenging if the issuer’s disclosure or investor communication is weak,” says Lau. “It’s important to understand the financial and nonfinancial dynamics, particularly ESG. Active investing allows you to be ahead of the curve.”

With property making up approximately 40% of the Asia high yield market,1 Lau emphasizes selectivity by focusing on established players that have secure market share or are increasing market share. Recent borrowing restrictions on Chinese property developers may strain weaker players, but in the longer term, will be positive for the sector, he adds.

“The key to understanding risks in China is understanding the policy agenda, what the central government wants to achieve, and the economic and social policy direction,” he explains.

In his over 30 years of experience in the industry, Lau notes that periods of market stress may also present opportunities to uncover undervalued issuers. For example, the pandemic has opened up opportunities to invest in “fallen angels” – investment grade-rated bonds that have been downgraded to junk bond status largely dragged by sovereign downgrades but whose fundamentals remain intact.

Over the long term, the emerging market for sustainability-linked bonds is poised to provide potential new opportunities that have not been widely available to date in Asia high yield. This segment has seen a mini-boom over the past year, as corporates sought to tap ESG-dedicated institutional capital to finance green projects as governments also race to reduce carbon emissions.

“We believe an actively managed standalone allocation to Asia high yield can maximize the rising income and growth opportunities in this highly dynamic market,” says Lau.

Learn more about Asia high yield opportunities at https://www.pinebridge.com/en-sg/intermediary-and-individual/featured-funds/asian-high-yield.

For more investment insights, please visit http://www.pinebridge.com.sg.

Sources 1 Source: J.P. Morgan, as of 31 March 2021.

PineBridge Investments' Disclaimer All investments involve risk, including the loss of principal amount invested. Past performance is not indicative of future results. The information presented herein is for illustrative purposes only and should not be considered reflective of any particular security, strategy, or investment product. It represents a general assessment of the markets at a specific time and is not a guarantee of future performance results or market movement. This material does not constitute investment, financial, legal, tax, or other advice; investment research or a product of any research department; an offer to sell, or the solicitation of an offer to purchase any security or interest in a fund; or a recommendation for any investment product or strategy. You are solely responsible for deciding whether any investment product or strategy is appropriate for you based upon your investment goals, financial situation and tolerance for risk. You should also read the prospectus of the investment product for further details, including the risk factors before investing. Any views express represent the opinion of the manager and are subject to change. Views may be based on third-party data that has not been independently verified. PineBridge Investments does not approve of or endorse any re-publication or sharing of this material. We are not soliciting or recommending any action based on this material. In Singapore, this document is issued by PineBridge Investments Singapore Limited (Company Reg. No. 199602054E), licensed and regulated by the Monetary Authority of Singapore (MAS). This advertisement or publication has not been reviewed by the MAS. Investors should note that the website www.pinebridge.com.sg and any other website (including any contents therein) referred to in this document have not been reviewed or endorsed by the MAS. |

To continue to serve you better, our system will be undergoing maintenance between 10 PM to 11:59 PM on 25 Apr 2024. During this period, you will not be able to access your dollarDEX account. We apologise for any inconvenience caused.