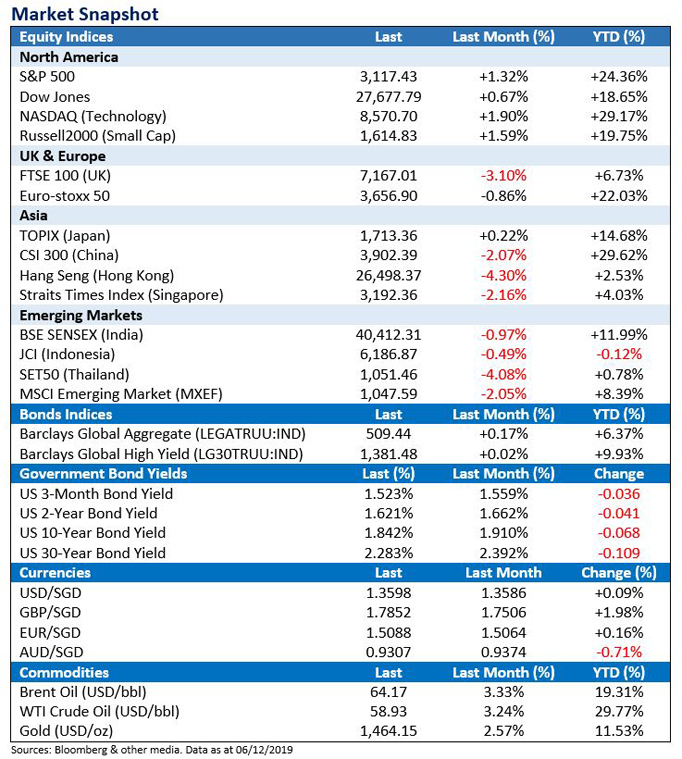

2020 investment outlook

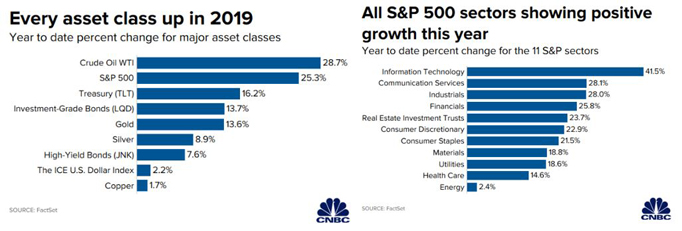

2019 is shaping up to be one of the best years for US investors with nearly every single asset class on track to finish the year in positive territory. Whether is it stocks, government debt, corporate bonds or commodities, investors would have reaped a profit no matter what they invest in. That is a stark contrast from 2018 where just about every single asset class posted flat or negative performance.1

All 11 S&P 500 sectors are also ending the year with positive returns, with technology leading a whopping 41.5% gain. Communication services, industrials, financials, real estate, consumer sectors are all up more than 20% this year.1

With 2020 just around the corner, the biggest question at the back of investors' minds is always “Is now a good time to invest?”

How are investors feeling about 2020?

According to UBS Investor Watch, which surveyed global investors on their outlook for 2020 and beyond, investors are feeling anxious with geopolitical tensions being the primary source of unease. It also revealed that 72% of investors described the investment environment as more challenging than it was five years ago and 52% of them are unsure if now is a good time to invest.2

With the overhang of trade tensions, US presidential election and growth slowdown, the findings come as no surprise.

So how should investors position their portfolio amid this uncertainty?

Here we look at each region and the expectations of them going into 2020.

Overall, the global economy is expected to enter a low–growth period of vulnerability over the next several quarters leading to a moderate recovery in the U.S and global growth in the course of 2020. However, elevated political uncertainty and events of extreme risks could weigh in on this expectation, hence it could be prudent to focus on capital preservation and be cautious on corporate credit and equities while waiting for more clarity.3

United States

PIMCO expects real US GDP growth to continue slowdown to a 1.25% - 1.75% range in 2020, from a peak of 3.2% in the second quarter of 2018. Slower global growth and elevated trade tensions are expected to continue to depress investment and export growth. Business output and profit growth is expected to slow and affect labour markets and weigh in on consumption.

Against this backdrop, we expect the Fed to support growth by cutting rates further over the next few quarters, resulting in some growth reacceleration in the second half of 2020.3

Eurozone

Core inflation and growth in the Eurozone is expected to remain low, close to the current level of around 1%. Ongoing trade tensions will exert a significant drag on eurozone growth, somewhat offset by supportive domestic conditions including easy financial conditions, some modest fiscal stimulus and some remaining pent–up demand. Growth is expected to improve modestly over the forecast horizon as trade conditions improve gradually through the year, but this remains uncertain.

While the European Central Bank (ECB) will potentially cut policy rate a little further, PIMCO expects the focus to remain on forward guidance and continued asset purchases.3

United Kingdom: Deal or no deal?

Brexit is expected to take place orderly, either through an amended withdrawal agreement or a relatively orderly no–deal exit with side deals, or a stand–still arrangement in place that mitigates any short–run economic disruption. However, neither a chaotic no–deal nor a revocation of Brexit can be entirely ruled out.

U.K GDP growth is expected to grow modestly below trend in 2020 at 0.75% - 1.25%, as headwinds from weak global trade, Brexit–related uncertainty, and possible disturbances in the event of an orderly no–deal exit weigh on growth. A fiscal boost and resilient consumer will likely provide some support. Against this backdrop, the Bank of England is expected to keep its policy rate unchanged at 0.75% but to cut in the event of a no–deal exit.3

Japan: Fiscal is the new monetary

GDP growth is expected to slow to a 0.25% - 0.75% range in 2020 from an estimated 1.1% in 2019 while domestic demand to remain resilient owing to a tight labour market and anticipated fiscal accommodation, which would likely more than offset a negative impact of the consumption tax hike.

Monetary policy and Quantitative Easing (QE) is at or close to exhaustion but there is clear appetite for fiscal stimulus from both the Bank of Japan (BOJ) and the government. Given rising external risks, the likelihood of BOJ action is also increasing though deeper negative rates could be controversial from a cost–benefit perspective.3

China: Flexible yuan to cushion impact of trade war

For the first time in almost 20 years, GDP growth is expected to fall below the psychological 6.0% and hover between the 5.0% - 6.0% range in 2020. Trade conflict continues to linger, consumption is weakening, property investment has peaked, and business investment remains sluggish. Fiscal stimulus of around 1.0% GDP for infrastructure and household consumption is expected to provide a boost in the first quarter of 2020.

Chinese policymakers have been using a flexible exchange rate as an automatic stabilizer and the Chinese yuan is expected to moderately depreciate against the US dollar as tariffs increase further. This should somewhat cushion the trade war's impact on manufacturers.

The People's Bank of China is also expected to cut rates by 50 basis points in addition to reduce the banks' reserve requirement ratios. However, credit conditions are likely to remain relatively tight and policy transmission to be slow due to rising defaults and the deleveraging of the shadow banking industry.3

With all these useful market updates on your fingertips now, review your investment portfolio to ensure that it continues to work towards your investment objectives. For those who are still sitting on the fence, take your first step by exploring funds on dollarDEX by using our intuitive fund finder and get started on your no-fees investing journey now!

YOU MAY ALSO LIKE

Disclaimer

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 10/12/2019.