Master the art of managing your cash with Money Market Funds

One important yet often ignored building block of wealth is the management of your idle cash, or simply, Cash Management. Many investors sit on cash for various reasons. They could be waiting for the right opportunity to enter the market, perhaps they have just exited an investment position and waiting to redeploy, or simply worried that they'll need the money for an emergency.

Whatever your reason for holding cash, you must know that inflation is eating your money away. Holding all that excess cash in banks earning the meagre 0.15% interest simply does not make great financial sense at all. For longer-term cash management, there are solutions such as the Singapore Savings Bond capped at $100,000 per individual as well as fixed term deposit for higher interest.

Money market funds or sometimes known as cash management funds is another great way to manage your idle cash, especially monies that you are planning to set aside for investments or when you are saving for a big ticket item like a wedding or a car.

Here, we attempt to breakdown what Money Market Funds (MMF) are, some of the benefits attached to it, and how you can get started to make your money work harder..

What are Money Market Funds?

MMFs are open-ended mutual funds that invests in short-term and low-risk debt securities such as Government Treasury Bills and Commercial Paper. One example of such securities is the "Public Utilities Board 3.9% 31/08/2018" where it uses the proceeds to finance infrastructure works undertaken by the Singapore Government. MMFs are usually benchmarked against bank deposits as they seek to preserve capital while providing a higher yield.

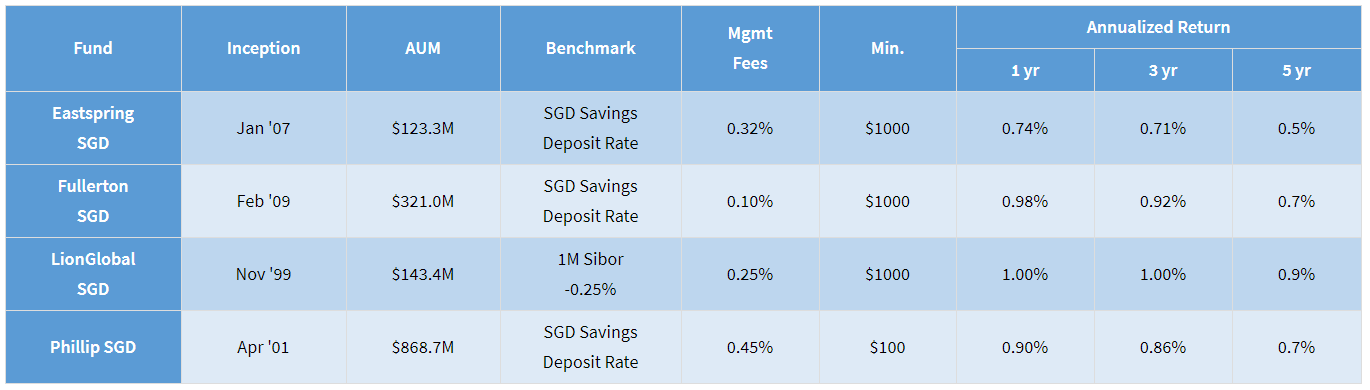

Like most unit trusts, MMFs publish their factsheets monthly and investors can read to understand what the fund manager invests in as well as how the fund has performed across different periods.

Currently on dollarDEX, there are nine Cash Management Funds/MMFs split into three broad categories:

- SGD denominated debt securities investable in SGD (most popular)

- USD denominated debt securities investable in USD

- Foreign Currency (USD or EUR) denominated debt securities investable in SGD

It comes as no surprise that SGD denominated debt securities investable in SGD (category 1) is the preferred choice for most Singaporean investors as there is literally no exposure to currency fluctuation since the base currency that they are holding is SGD to begin with. Adding to that, the stability and performance has generally been better as compared to the other two categories with exposure to USD or EUR. However, if you have a view on USD or EUR against the SGD, or that your preferred holding currency is in USD, categories two and three are definitely worth a consideration as well.

Given that the Singapore MMF is the most popular option, let's dig a little deeper into it.

From the table above, the most commonly used benchmark for Singapore Money Market Funds is the SGD Savings Deposit Rate. The annualized return for the MMFs also ranges from 0.7% to 1% per annum depending on the fund you select, which is far better than putting it into a normal bank deposit account. A look at the chart performance on the factsheets will show a steady upward sloping line with minimal volatility. That said, MMFs are not capital guaranteed. Of course, some may argue, too, that deposits above $50,000 with each bank are also at risk as they are not being covered by the SDIC (Singapore Deposit Insurance Scheme).

So, who should consider Money Market Funds?

1. Investors who are new to unit trust / dollarDEX

If you are new to unit trust investing or new to the dollarDEX platform, this is one good way to get started without taking too much risk. You can familiarize yourself with the entire process flow from fund selection, investing, payments, portfolio tracking, switching and even redemption. Given that you pay close to nothing on dollarDEX (zero commissions & zero switching fee), there is no better way to kick-start your investing journey than through a Money Market Fund.

2. Investors with idle SRS accounts

If you are a smart taxpayer that have been squirrelling money away in an SRS (Supplementary Retirement Scheme) account over the years, good on you! However, do you know that the interest earned is at a nominal 0.05% per annum? (Yes, shocking but true) Thankfully, another great benefit of the Singapore MMF is that you can use both Cash and SRS to buy into the fund! So why short-change your retirement fund when you can potentially make much more with MMFs?

3. Seasoned investors who are waiting for the right time to enter the market

For seasoned investors who are price sensitive and prefer to "time" the market, MMFs offer an excellent way to "park" your funds while you wait for that opportune moment. Instead of selling your existing holdings and have it credited into your local bank account as cash, consider a switch into a MMF for a potentially better yield.

Investors holding on to cash and waiting on the side can also consider holding MMFs first and subsequently switching into the fund of your choice as the turnaround time for switching is much faster and administratively easier.

To find the full list of MMFs on dollarDEX, simply go to Fund Finder -> Select Cash Mgmt under Asset Class.

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 06/09/2018.