Amid low returns from “safe” bonds, look to Asian risk assets

13 Jun 2019

Summary

Thanks to positive macroeconomic news, China's resilient growth and room to cut rates in India and Indonesia, the outlook for Asia–Pacific risk assets is good. Corporate bonds, emerging-market debt and dividend–paying stocks can play a critical role for investors in search of income potential.

Key takeaways

- “Riskier” assets in the Asia-Pacific region offer attractive income potential for investors dissatisfied with the returns of traditionally “safe” bonds

- After a tough 2018, Asian risk assets have been supported by Federal Reserve policy, easing US–China trade tensions and stabilising growth in China

- China's growth outlook is positive for Asia overall and should help the region's equity markets, including dividend–paying stocks

- India and Indonesia have room to cut their policy rates, which should help their bonds

With traditionally “safe” bonds offering limited returns globally, we suggest investors actively hunt for income among “riskier” income generators such as corporate bonds, emerging-market debt and dividend–paying stocks. Asia–Pacific risk assets can play a critical role for investors, given the region's positive macroeconomic news, China's resilient growth and the potential for lower rates in India and Indonesia.

A favourable macro backdrop for Asia-Pacific

In 2018, the Asian market was dragged down by concerns over rate hikes by the Federal Reserve, rising tension in the US–China trade relationship and slowing growth in China. But since the beginning of 2019, these three key factors have become tailwinds that support Asian risk assets.

- The Fed is more patient. Additional Fed rate hikes and further strength in the US dollar seem unlikely this year. This should help stem the outflow of capital to the developed markets from Asia and the emerging–market world.

- A full–blown US–China trade war seems less likely. Despite the recent escalation in tensions, we think the threat of weaker global trade and financial shocks will push the US and China to put aside their differences and eventually settle for a trade deal. Both sides remain engaged in negotiations despite the sabre–rattling rhetoric; market sentiment can shift drastically on sign of any positive development.

- China's growth looks more stable. Proactive fiscal and monetary stimulus measures from the Chinese government seem likely to stabilise the country's growth this year. China's government has set 6%–6.5% as the official growth target for 2019, and we believe the authorities have the willingness and means to achieve it.

Resilient growth dynamic in China

Given the release of China's stronger–than–expected credit, growth and GDP data in the first quarter, we think the market will agree with our view that a sharp deceleration in Chinese growth is unlikely this year. This would be supportive for the Asia–Pacific region given how dependent regional economies are on trade with China. As the following table shows, China has become the most important export destination among many Asian economies – surpassing even the United States and the European Union. This gives us additional confidence in Asia's growth potential despite the risk of slowing demand in the developed world.

Asia's export economy depends on China

Export exposure in value-added terms by destination of final demand (& of GDP)

Source: OECD–WTO TiVA database, Allianz Global Investors Economics & Strategy. ASEAN: Association of Southeast Asian Nations. Data as at 2015.

Another factor supporting our optimism on Asia is the expected bottoming–out of the tech cycle in mid–2019. We expect the global semiconductor sales cycle to benefit from a pickup in demand from major tech firms that plan to expand data centres, and from a pre–build in inventory by a key smartphone and 5G equipment manufacturer. This should help North Asian economies, which have a heavy tech focus in their export mix.

Room for policy rate cuts

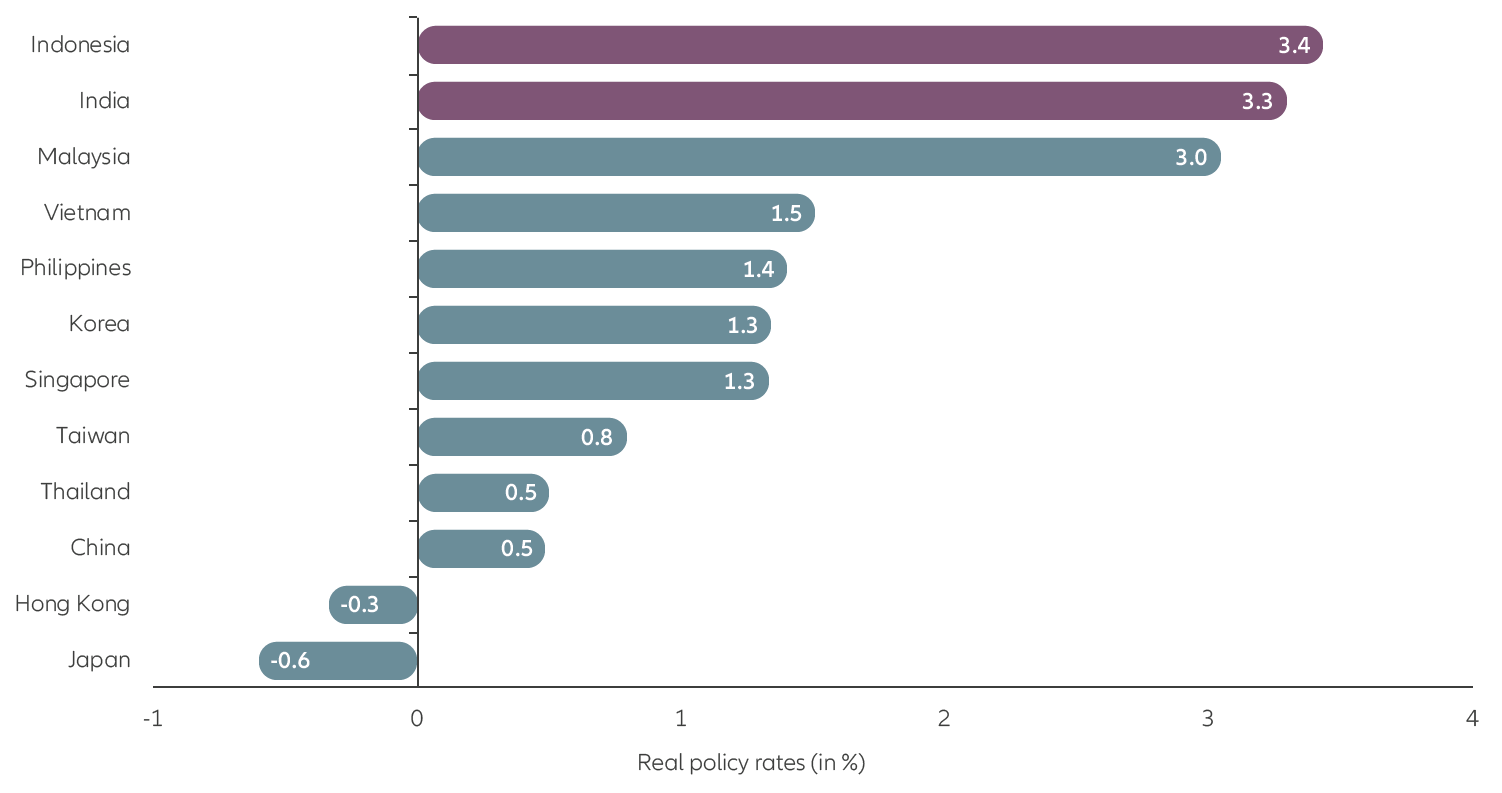

Central banks in domestic–demand–driven economies like India and Indonesia should also help support growth momentum in Asia. The accompanying chart shows the real policy–rate levels of key Asian countries; India, Indonesia and Malaysia are relatively high at 3% and above.

India and Indonesia have room to cut rates

Real policy rates (in %) of key Asia-Pacific central banks

Source: CEIC, Allianz Global Investors Economics & Strategy. Data as at March 2019.

Given globally low inflation and a stable external environment thanks to an accommodative Fed, we think the central banks of India and Indonesia will cut policy rates to guide down their domestic interest–rate levels and support their economies. We expect the Reserve Bank of India to make a 25 basis–point cut in June, with the potential for more in late 2019, and we expect Bank Indonesia to start cutting rates in the second half of the year.

Infrastructure investments are also important for India and Indonesia's growth. We think it is important for these two economies to improve their basic infrastructure – such as power stations, roads, railroads, ports and airports – to solicit private investments and push forward the industrialisation process. India's Narendra Modi and Indonesia's Joko “Jokowi” Widodo agree, which is one of the reasons why they pledged to keep investing in infrastructure in their re–election campaigns. Of course, structural reforms are also needed to upgrade the legal and fiscal foundations and help the economies of these countries become more efficient and productive.

Investment implications

- Stable growth in China is positive for Asia, and it should help the region's equity markets and dividend-paying stocks.

- A turnaround in the tech cycle would be positive for North Asia's economies, benefiting the tech sector and supporting export growth.

- India and Indonesia, along with other economies such as Malaysia and the Philippines, have room to cut their policy rates, which should help their fixed–income securities.

YOU MAY ALSO LIKE

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Diversification does not ensure a profit or protect against a loss. Equities have tended to be volatile, and do not offer a fixed rate of return. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Foreign markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of this document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Panama, Peru, and Uruguay.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG, licensed by FINMA (www.finma.ch) for distribution and by OAKBV (Oberaufsichtskommission berufliche Vorsorge) for asset management related to occupational pensions in Switzerland; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

843725

All information here is for GENERAL INFORMATION only and does not take into account the specific investment objectives, financial situation or needs of any specific person or groups of persons. Prospective investors are advised to read a fund prospectus carefully before applying for any shares/units in unit trusts. The value of the units and the income from them may fall as well as rise. Unit trusts are subject to investment risks, including the possible loss of the principal amount invested. Investors investing in funds denominated in non-local currencies should be aware of the risk of exchange rate fluctuations that may cause a loss of principal. Past performance is not indicative of future performance. dollarDEX is affiliated with Aviva but dollarDEX does not receive any preferential rates for Aviva products as a result of this relationship. Unit trusts are not bank deposits nor are they guaranteed or insured by dollarDEX. Some unit trusts may not be offered to citizens of certain countries such as United States. Information obtained from third party sources have not been verified and we do not represent or warrant its accuracy, correctness or completeness. We bear no responsibility or liability for any error, omission or inaccuracy or for any loss or damage suffered by you or a third party (including indirect, consequential or incidental damages) arising in any way from relying on this information.

This information does not constitute an offer or solicitation of an offer to buy or sell any shares/units.

This article has not been reviewed by the Monetary Authority of Singapore.

Information is correct as of 04/06/2019.